The Australian markets ended the week in the red on the back of a strengthening dollar and China’s weak economic data coupled with its unrelenting COVID-zero policy.

The materials sector was particularly badly hit.

The ASX200, ASX300, and Ordinaries ended the week down 1.08%, 1.12%, and 1.15% respectively.

Table of Contents

Last Week In ASX Stocks

ASX Materials Index (ASX:XMJ)

The ASX Materials Index (ASX:XMJ) closed the week down an abysmal 6.06% after a strengthening dollar battered commodities, while renewed COVID restrictions in China clouded demand prospects. Poor economic data out of China exacerbated the pain.

Sector majors BHP (ASX:BHP), Mineral Resources (ASX:MIN), South32 (ASX:S32), Rio Tinto (ASX:RIO), and Fortescue Metals (ASX:FMG) tanked 6.48%, 7.78%, 8.42%, 3.47%, and 3.93%, respectively.

New energy miners IGO (ASX:IGO), Lynas Rare Earths (ASX: LYC), and Allkem (ASX:AKE) closed lower by 5.71%, 1.34%, and 1.16%; however, Pilbara Minerals (ASX:MIN) stood out gaining 1.05%.

Also of concern for the sector gold’s poor performance despite the current global macro and financial environment which should have played to its strengths.

This begs the question: Is the yellow metal still a hedge against inflation and turmoil?

Gold producers Newcrest Mining (ASX:NCM), Evolution Mining (ASX:EVN), and Northern Star Resources (ASX:NST) ended lower by 4.33%, 3.77% and 1.82%, respectively.

ASX Energy Index (ASX:XEJ)

The ASX Energy Index (ASX:XEJ) fared poorly, losing 1.8% for the same narratives: A relentless dollar and recessionary fears.

Heavyweights Woodside Energy (ASX:WDS), Beach Energy (ASX:BPT), and Santos (ASX:STO) closed lower by 2.14%, 3.22%, and 1.83%.

However, coal majors New Hope Corporation (ASX:NHC), Stanmore Resources (ASX: SMR), Coronado Global (ASX:CRN), Whitehaven Coal (ASX:WHC), and Yan Coal (ASX:YAL) ripped higher by 12.97%, 1.88%, 8.91%, 10%, and 8.76% on rumors of a reversal of China’s ban on Aussie coal.

ASX Industrials Index (ASX:XNJ)

The ASX Industrials Index (ASX:XNJ) outperformed giving up just 0.43% as the medium-term outlook for export-oriented industrial majors looked comparatively better on the back of the strengthening dollar as well as strong economic data in the form of jobs and retail sales in the US.

Nonetheless, industrial commodities makers Brickworks (ASX:BKW), ADBRI (ASX:ABC), and Boral (ASX:BLD) tanked 2.56%, 3.75%, and 2.65% as rising interest rates dented construction outlook; worse, rampant inflation continues to suppress margins.

Industrial majors Amcor CDI (ASX:AMC) and Brambles (ASX:BXB) ended up 0.99% and 1.99% while Reece (ASX:REH) and Reliance Worldwide (ASX:RWC) closed down 4.61% and 3.54%.

Infrastructure players Transurban Group (ASX:TCL) and Qube Holdings (ASX:QUB) closed up 0.14% and down 3.57%, respectively.

Airlines Qantas (ASX:QAN) and Air New Zealand (ASX:AIZ) ended down 0.9% and up 0.88%, respectively.

In other news, Rex Airlines (ASX:REX) announced plans to acquire Cobham Aviation’s mining air freight business for A$42 million.

ASX Financials Index (ASX:XFJ)

The ASX Financials Index (ASX:XFJ) also fared better, down just 0.8%, after being heavily oversold over the past few months.

Banking heavyweights Commonwealth Bank of Australia (ASX:CBA), Australia New Zealand Bank (ASX:ANZ), and Westpac (ASX:WBC) lost 0.13%, 5.18%, and 1% respectively while National Australia Bank (ASX:NAB) gained 0.57%.

Regional banks Bank Of Queensland (ASX:BOQ) and Bendigo Adelaide (ASX:BEN) closed down 1.85% and up 1.17%, respectively.

Wealth managers Magellan (ASX:MFG), Platinum Asset Management (ASX:PTM), and AMP (ASX:AMP) closed lower by 2.2%, 9.17%, and 1.46% respectively.

Platinum reported net outflows worth AU$304 million in June, the highest since February last year.

Insurers Suncorp (ASX:SUN) and QBE Insurance (ASX:QBE) ended down 0.09% and 2.02% while Insurance Australia Group (ASX:IAG) closed up 0.69%.

Diversified financial services major Macquarie Group (ASX:MQG) declined 1.8%.

ASX Consumer Discretionary Index (ASX:XDJ)

The ASX Consumer Discretionary Index (ASX:XDJ) bucked the market trend, gaining 0.93% given its perceived resilience in the face of the current adverse macro environment.

Hospitality companies Star Entertainment (ASX:SGR) and Skycity Entertainment (ASX:SKC) closed lower by 1.02% and up 3.38%, respectively.

Travel companies Webjet (ASX:WEB), Flight Centre (ASX:FLT), and Corporate Travel Management (ASX:CTD) fell 6.03%, 7.04%, and 6.89%.

However, retailers Temple and Webster (ASX:TPW), Kogan (ASX:KGN), and Nick Scali (ASX:NCK) closed down 9.29%, 14.97%, and 6.49% while Harvey Norman (ASX:HVN) and JB Hi-Fi (ASX:JBH) inched into the green at 1.29% and 0.25%, respectively.

Investors appear to be nervous about Kogan’s profitability given supply chain pressures and a cutback in consumer spending amidst inflation.

The uncertain state of the Chinese economy hurt the short-term outlook of appliance maker Breville (ASX:BRG) as it fell 2.77%. Food brands Dominos (ASX:DMP) and Collins Foods (ASX:CKF) closed down 1.14% and 4.10%, respectively.

ASX Consumer Staples Index (ASX:XSJ)

The ASX Consumer Staples Index (ASX:XSJ) similarly trod a different path and returned to being an investor favorite gaining 1.91% for the week.

Sector majors Coles Group (ASX:COL), Wesfarmers (ASX:WES), and Woolworths (ASX:WOW) rose 3.44%, 2.82%, and 2.79%.

Food producer Tassal Group (ASX:TGR) ended up 0.21% while Bega Cheese (ASX:BGA), Costa Group Holdings (ASX:CGC), and GrainCorp (ASX:GNC) closed down 10.44%, 2.31%, and 3.17%, respectively.

Bega Cheese slumped after the company warned that its earnings would be impacted due to record milk prices.

Processed food makers a2M Milk (ASX:A2M) and Bubs Australia (ASX:BUB) also ended down 0.77% and 6.85%, respectively.

BUBS sold off regardless that it formal confirmation from the Biden administration to position itself for a permanent presence in the US market.

ASX All Technology Index (ASX:XTX)

The ASX All Technology Index (ASX:XTX) was, for a change, a relative outperformer as it rose 0.46%.

Platform companies REA Group (ASX:REA), Carsales (ASX:CAR), RedBubble (ASX:RBL), and Domain Holdings (ASX:DHG) declined 0.7%, 4.8%, 5.53%, and 5.97%, respectively.

Saas players Xero (ASX:XRO) and WiseTech Global (ASX:WTC) ended up 0.55% and 6.16% while Appen (ASX:APX) and Nuix (ASX:NXL) slumped 8.53% and 13.25%, respectively.

BNPL players took a heavy beating on rising rates, regulatory oversight, debt quality and recessionary fears.

Majors Block (ASX:SQ2), Sezzle (ASX:SZL), and MoneyMe (ASX:MME) fell 4.88%, 51.76%, and 8.46%.

Sezzle was hammered after it canceled its planned merger with ASX BNPL peer Zip Co (ASX:Z1P).

Zip, on the other hand, rose 11.76% due to the unwinding of the proposed transaction.

While the transaction will dent the company’s US expansion plans, investors were relieved that a potential cash burn on a US expansion is avoided.

Semiconductor and data center companies Altium (ASX:ALU) and NextDC (ASX:NXT) closed 0.52% and 0.087% in the green.

ASX Healthcare Index (ASX:XHJ)

The ASX Healthcare Index (ASX:XHJ) was however, the star sector of the week, clocking gains of 3.48%.

Though healthcare providers Ramsay Healthcare (ASX:RHC), Fisher and Paykel (ASX:FPH), and Healius (ASX:HLS) ended 0.043%, 1.51%, and 1.34% down, healthcare equipment makers Sonic Healthcare (ASX:SHL), Cochlear (ASX:COH), CSL Ltd. (ASX:CSL), and Resmed CDI (ASX:RMD), all of which are big exporters and beneficiaries of a strengthening US dollar, ticked higher by 1.68%, 5.97%, 3.71%, and 4.28%.

Meanwhile, biotech firms Imugene (ASX: IMU) and Mesoblast (ASX: MSB) ended up a mammoth 78.57% and 21.32% respectively after encouraging trial results.

ASX Real Estate Index (ASX: XPJ)

The ASX Real Estate Index (ASX: XPJ) fell just 0.24% during the week.

Sector majors Mirvac Group (ASX:MGR), Stockland Group (ASX:SGP), Vicinity Centres (ASX:VCX), and Scentre (ASX:SCG) all ended within 2% in the red.

ASX Telecom Index (ASX:TLS)

The ASX Telecom Index (ASX:TLS) also outperformed closing 1.81% in the green.

Sector players Telstra (ASX:TLS), Uniti Group (ASX:UWL), and Chorus (ASX:CNU) gained 1.81%, 1.11%, and 3.79% respectively, while TPG Telecom (ASX:TPG) ended down 1%.

Lastly, the ASX Utilities Index (ASX:XUJ) ended nearly flat but in the green by 0.059%. Sector majors APA Group (ASX:APA) closed up 3.62% while Origin Energy (ASX:ORG) and AGL Energy (ASX:AGL) ended lower by 3.33% and 2.89%, respectively.

Next Week In ASX Stocks

There are no major earnings announcements due for next week.

New Listings

No new listings next week.

Market and Economic Outlook

The major themes of the week were US retail sales for June, the all-important inflation print for June, and the start of the earnings season.

US retail sales reported a solid 1% growth (MoM) and 8.4% (YoY).

Unfortunately, this was counterbalanced by a worse-than-expected inflation print of 9.1% and poor earnings from banking majors Morgan Stanley and JP Morgan.

Markets were also unnerved by Canada’s huge 100 basis point rate hike.

In the APAC region, China reported an underwhelming 0.4% growth Q2 GDP (YoY) which was lower than expected.

However, Chinese Industrial Production grew 3.9% YoY. The country also enforced another round of lockdowns and testing.

Over in New Zealand, the Reserve bank delivered another 50 basis point hike which took the country’s cash rate to 2.5%, a six-year high.

Next week, on Monday, New Zealand declares its Q2 QoQ CPI .

The following day, the Eurozone publishes its YoY CPI for June while the US reports on Building Permits for the same period.

On Wednesday, we receive the British YoY CPI for June and a press address from BoE Governor Bailey.

On Thursday, US is due for Existing Home Sales for June, Initial Jobless Claims, Crude Oil Inventories, and the Philadelphia Fed Manufacturing Index for July.

More importantly, the ECB announces its Monetary Policy Statement, Interest Rate Decision, and Press Conference.

Lastly, on Friday, the UK will release MoM June Retail Sales along with its Services, Manufacturing, and Composite PMI.

Forex Outlook

AUD/USD

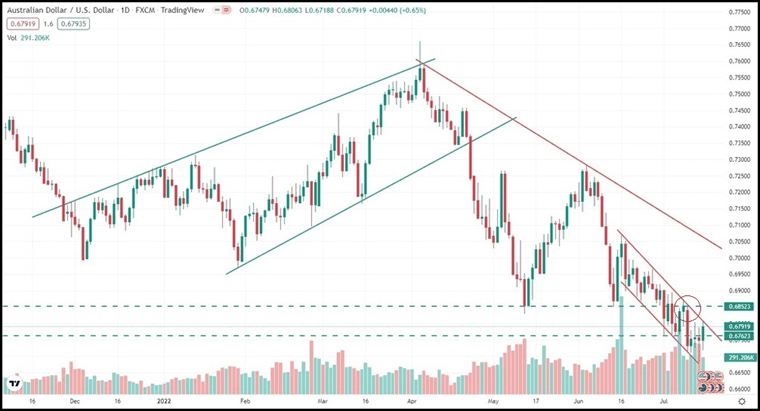

AUD/USD closed at 0.67919, below the previous weekly close of 0.68538, after slumping to a low in the vicinity of 0.66830, from where it rebounded.

The pair began the week with a solid drop as it met with the symmetry (red circle) of the 0.68500 zone of resistance as well as the upper (falling) line of the recent leg down channel on the daily chart above.

In the process, it created a massive evening star candlestick pattern, albeit inside a falling channel, but with negative implications nevertheless.

In the following two sessions, there was a tepid relief rally, but on Thursday, the bears came back into their own and slammed AUD/USD to a low of around 0.66830 that coincided with the lower line of the falling channel.

This, despite a beat on expectations from Australian employment data. Likely, the gut-punch US CPI number last week put paid to bulls’ intentions if any.

On Friday, AUD/USD rebounded as the Dollar Index softened, but the move again stalled at the upper channel line.

The down-sloping channel is, therefore, to be respected, given the breathtaking 1% rate hike by the RBC, and whispers that the US Fed, later this month, could also pull out a larger-than-expected rabbit from its hat.

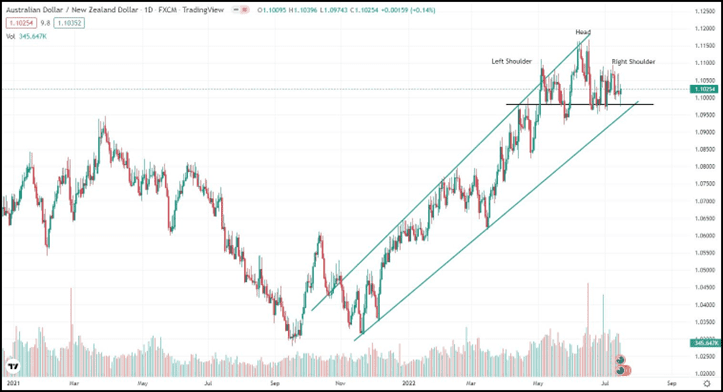

AUD/NZD

AUD/NZD ended the week at 1.10254, below the previous week’s close of 1.10650.

Technically, on the daily chart above, AUD/NZD appears to be hammering out a bearish head-and-shoulders pattern which will be confirmed if the 1.09810 and 1.09519 lines are violated to the downside.

The bearish probability is enhanced by the clearly enunciated desire of the RBNZ to control inflation, with even more rate action if necessary, despite the 50 bps hike during the week.

Tempering this assessment is the bullish jobs number issued by Australia, which came in far better than expected.

But that bounce was quickly sold into as the chart shows for Thursday, evidenced by a shooting star pattern.

The trajectory for AUD/NZD appears to be soft, therefore, and would become clearer with the kind of support that emerges at lower levels.