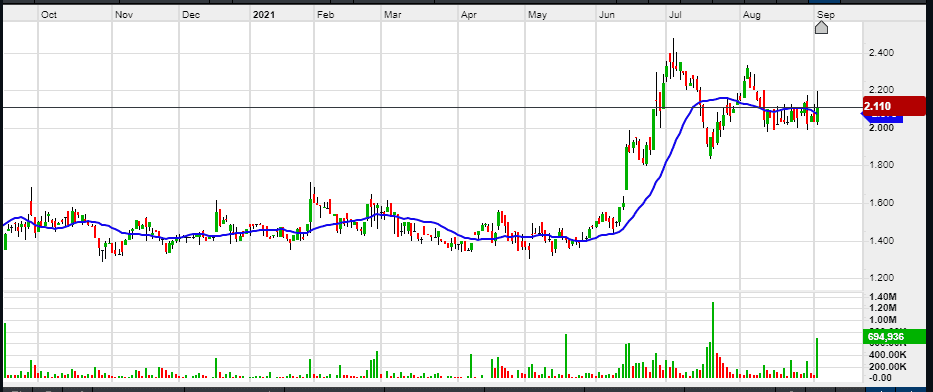

Entry : Maximum buy price $2.20

Position size : 4,500

Stop loss : $1.50

MME is fast moving disruptor in the personal lending sector targeting consumers that traditional lenders are shying away from. MME is a leader in the fintech space offer a list of products such as:

- Personal loans

- Freestyle virtual master card

- Moneyme+ a Buy Now Pay Later offering launched in August 2020

- ListReady covering expenses of preparing a property for sale

- AutoPay – Financing for settlement of vehicles in under 60 minutes launched in August 2020

As a provider of loans MME revenue is the interest charged on loans originated. Growth in the loan book over time will translate into revenue growth as the loans mature. As per the MoneyMe FY21 Results recently released the company has made significant progress:-

- Gross receivables $333m up 149%

- Revenue up 21% to $58m

- NPAT $12M up 16%

- Establishment of bank warehouse facility reducing funding costs by 55%

MME differentiates itself from traditional lenders by the speed at which loan can be approved. With 93% of loan approvals and payments automated. If we take a look at the recently launched AutoPay facility for vehicle financing, loans can be approved in under 60 minutes. Gone are the days of going to the dealership selecting the car then having to wait seven days while the finance broker or bank goes through the slow laborious process of approval and settlement. With Autopay you can be driving away with the car in 60 minutes. For car dealerships it is a volume game the more cars sold the greater the profit is the Autopay product is likely to see significant uptake over the foreseeable future.

Now MME is not the only fintech company in the lending space disrupting the incumbents, in the last few years you have seen the likes of Afterpay (APT), Zip Co (Z1P) and Wisr (WZR) all offer loan products of differing types. All three companies have seen rapid growth but have never generated profits, this has not stopped investors giving these business extremely high valuations. MME are generating positive NPAT while continuing to grow strongly all the while maintaining strong credit standards.

Key Risk

- Quality of credit originations (bad debt)

- Australian economic conditions