Allkem (AKE) is a resources company focused on the extraction and processing of Lithium chemical compounds.

The company is the result of an August 2021 merger between two lithium companies Orocobre (mine based in Argentina) and Galaxy (mine based in Australia).

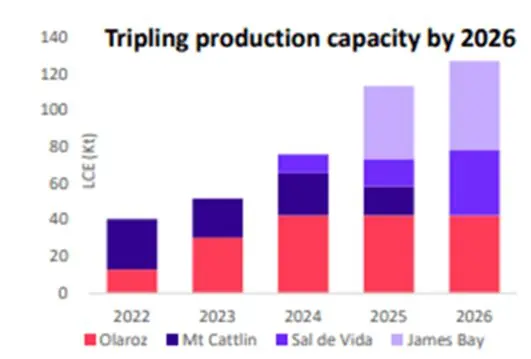

The company’s current Lithium production comes from 2 well-established mines, Olaroz and Mt Cattlin. Additionally, the company is currently building out a conversion facility in Naraha (Japan) as well as making progress on 3 other lithium mining sites – Sal de Vida (Argentina), Cauchari (Argentina), and James Bay (Canada).

I am interested in Allkem because of its

1) diversified geographical presence,

2) its assets that are currently in production that allows them to take advantage of the current high prices for lithium

3) its project pipeline that will triple production by 2026.

As per the table, the Mt Cattlin mine based on current ore reserves is due to reach the end of its life in 2025. The company is undertaking a drilling program which will expand the mines life.

In its recently reported FY2022 Results, Allkem reported revenues of US$770m and net profits of US$337m. These results gave the first glimpse of the company’s profit potential post its merger.

The profit result was based on

- Lithium carbonate FOB price of US$23,398/t in FY22, compared to US$4,983/t in FY21.

- Lithium spodumene had an average price of US$2,221/dmt in FY22, compared to US$415/dmt for the 30th June 2021

On Friday the company released its Sep 2022 Quarterly Report and the prices achieved by the company have only increased

- Revenue for the quarter was $298M

- Lithium carbonate average price US$42,237

- The sale price for lithium carbonate in the next quarter is expected to be approx. US$50,000

- Lithium spodumene’s average realised sale price was US$5,028

There was some slight negative news in the quarterly report. Olaroz Stage 2 expansion which is 93% built was expected to be in production by the end of 2022 has been delayed. The company was advised by suppliers of several key components that raw material supply and logistics constraints mean delivery will not occur on time. As a result, first production is not due until Q2 2023.

The delay in bringing online new mining projects is not a problem specific to Allkem as it’s industry-wide. Delays in bringing new lithium production online means the supply deficit will remain for longer than expected and prices will remain elevated leading to higher profitability for longer.

TRADE ACTION

Number of shares: 500

Entry: Buy up to: $14.90

Stop loss: $13.00

Target Price : $18.00