For those unfamiliar, Life360 (360) has a market leading app for families, called Life360.

One way to view 360’s core offering is a provider of family safety services. Users download the app which incorporates mobile phone GPS data. Numerous services are then available including location safety (families can track members), driving safety (crash detection and roadside assistance) and emergency assistance.

Besides the family-based app, 360 is also a leader in locating people, pets and things. Broadening their product suite, 360 also offers wearable devices (called tiles) which can be attached to items such as wallets, keys, handbags, luggage and pets.

360’s downloadable app has been a top-rater on mobile app stores whilst a wearable tile can be purchased at a typical retail store like JB HI FI.

There are a couple of reasons why we like 360. Firstly, we like the fact that 360 is a founder led business. In fact, Chris Hull founded the business is 2007 and continues to be a major shareholder today.

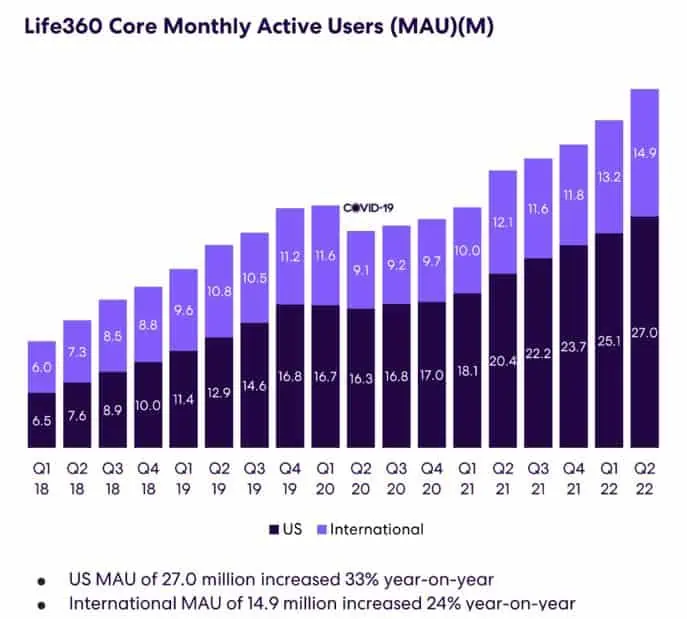

Secondly, 360’s growth has also been extremely strong and now boasts over 42 million monthly active global users. Importantly, as highlighted below, Monthly Active Users increased 29% year-on-year with U.S. delivering an impressive 33% uplift.

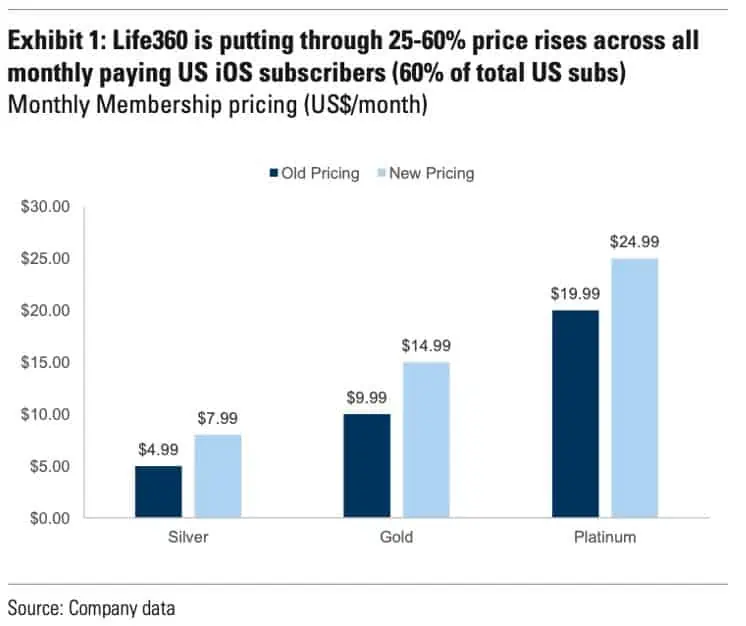

Recently, 360 announced increases for the price of its monthly US iOS subscriptions (annual subscriptions remain unchanged). The $4.99 silver monthly membership is now $7.99, the $9.99 gold membership is now $14.99, and the $19.99 platinum membership is now $24.99. This equates to a 25 – 60% price increase in monthly fees, as seen below:

More recently, (13th of Jan), 360 provided a 4Q trading update. A workforce restructure with a 14% reduction in employees was announced, driving an annualised cost saving of 15 million. This saving has brought forward expectations of cashflow break even target as the closing year of 2023 is now expected to be positive on an adjusted EBITDA/Operating cash flow basis. 360’s outlook for 2023 also looks solid with revenue growth expected to be 35% in addition to breakeven on an FY basis.

On the technical front, for a high PE speculative stock, 360 has succumbed to the pressure of the market, yet, once again we are looking for stocks that show strength when compared to the general market (the XJO) and 360 has shown decent strength in a very poor market, outperforming the XJO by 40% over the last 6 months. Through its short history, 360 has also shown evidence of being able to rally and make big moves. We recently got a taste of this when our index put in that 18% rally off the June lows whereas 360 put in a 123% rally during the same period.

In fact, 360 was the third best performing stock that showed the most strength off the June lows when compared to the entire ASX. During that rally (from 20th of June to 15th of August) we saw a rotation out of those low PE, strong performing energy and lithium producers into those beaten down growth and speculative areas of the market. Hence, what we saw in that rally (which was spurred on by optimism of a peak in inflation) could be a sneak peak of what’s to come when the market does switch back to a risk on environment. With a peak in interest rates and a decrease in inflation expectations, we are closer to a risk on environment than ever before.

Although, a common problem many growth stocks will face as they move higher is downward pressure from trapped buyers above who may look to exit once the share price reaches their entry price. The number of trapped buyers in 360 wanting to exit is unaccountable. This is just the reality of investing, it’s never perfect, as there’s always something to pick holes at which could be viewed as contentious. For instance, a stocks PE, or lacking quality institutional ownership, volume could be better, moving averages have not crossed over. Investing is an imperfect endeavour so it’s more about attempting to make decisions that stack the probabilities in your favour.

For example, the fresh positive news out by 360 should provide order flow (the buying continue) which increase the chances of the stock trending in the same direction without our stop getting hit. We can also add that 360 has just undergone a trendline break through the sloping descending resistance line, not to mention also bouncing off the 200 day moving average (a critical area of technical interest). A stock with confluence holds a better risk reward/opportunity than a plain vanilla trendline break with no fresh news. This is why we prefer stock patterns like 360 that have a built-in catalyst.

Despite these positives, there are still plenty of risks out there. For example, 1) consumer spending could pull back because of inflation, 2) we could see an increase in competition, and 3) we could also see a higher churn rate or lower subscription growth with these new changes.

TRADE ACTION

Number of shares: 600

Entry: Buy up to: $5.80

Stop loss: $4.90

Target Price : $7.45