Supply Network (ASX SNL) – A Compounding Machine With Structural Tailwinds

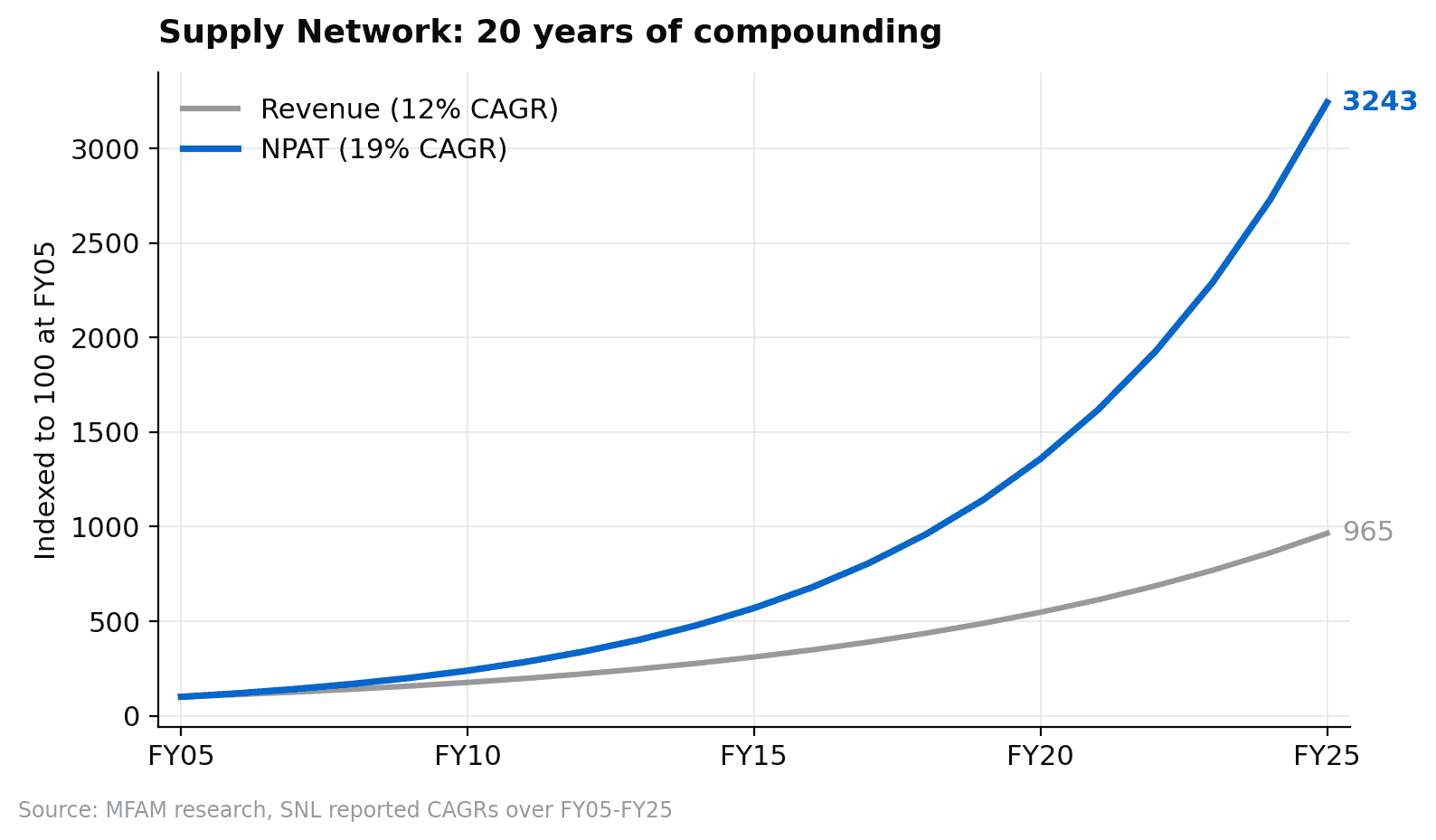

Supply Network (ASX: SNL) is one of the most consistent compounders on the ASX, delivering a 20-year revenue and NPAT CAGR of 12% and 19% respectively while consistently exceeding its own three-year targets. The company distributes aftermarket truck and bus parts across 26 branches in Australia and New Zealand, and Australian sales are accelerating at 18.5% in the first half of FY26. Structural tailwinds from increasing road freight volumes, a shift from OEM to aftermarket, and growing truck parc complexity support the long-term thesis. With a 33%+ ROE, a net cash balance sheet, and disciplined capital management, the 12-month price target of A$38.10 implies 10% upside.

Research published 25 February 2026. Price target and upside based on prices at time of publication.

About Supply Network

Supply Network Ltd (ASX: SNL) is Australia’s leading aftermarket distributor of truck and bus parts, operating 26 branches across Australia and New Zealand under the Multispares brand. The company distributes parts for all major truck and bus brands and has built a 20-year track record of compounding growth that few ASX-listed industrials can match. Headquartered in Brisbane and listed on the ASX, Supply Network has a market capitalisation of approximately A$1.5 billion and an enterprise value of A$1.5 billion, reflecting a net cash balance sheet.

Why We Like SNL at Current Levels

Supply Network is one of those rare ASX businesses where the numbers speak for themselves. A 20-year revenue CAGR of 12% and NPAT CAGR of 19% is an extraordinary track record, and the company has consistently exceeded its own three-year targets along the way. At A$34.53, we see 10.3% upside to our A$38.10 price target, and we think the setup over the next two to three years remains highly attractive given the structural tailwinds supporting aftermarket truck parts demand.

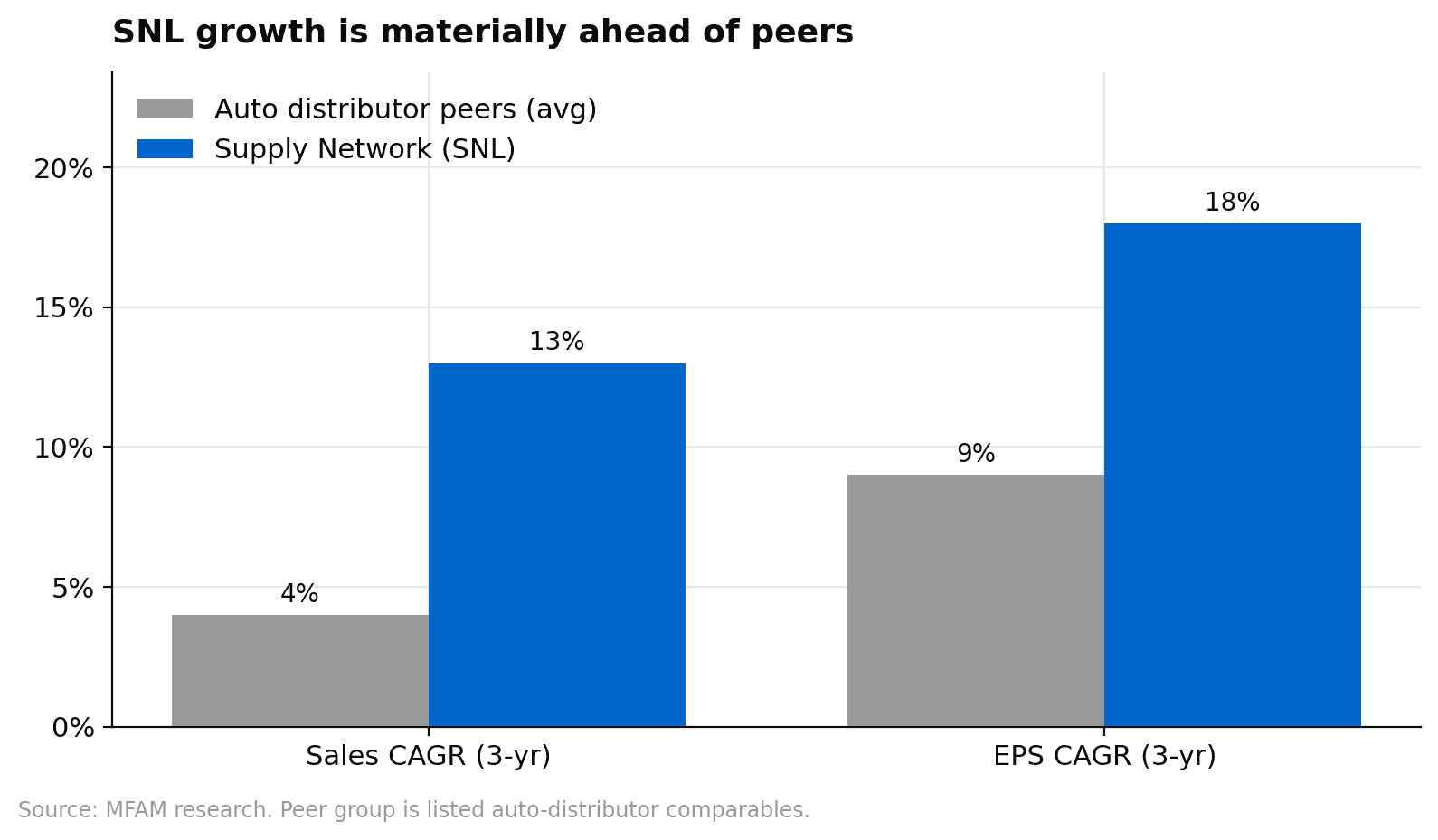

Our price target is derived from a 50/50 blend of a DCF valuation at A$40.09 per share (using a WACC of 9.2%, terminal growth rate of 3.0% and risk-free rate of 3.5%) and a PE multiple approach at A$36.09 (applying 30x to weighted FY26/27 earnings). The 30x PE represents a premium to listed auto distributor peers, which trade on an average of around 17x, but we think that premium is well justified by Supply Network’s materially stronger growth outlook. On a three-year basis, SNL’s sales CAGR of 13% and EPS CAGR of 18% sit well above the peer group averages of 4% and 9% respectively. On a PE-versus-EPS-growth scatter plot among auto distribution peers, SNL stands out clearly as a superior compounder.

Australian Sales Momentum is Accelerating

The most encouraging signal from the first half of FY26 is the acceleration in Australian sales growth. Domestic revenue grew 18.5% in 1H26, up from 13.7% in 2H25, which is meaningfully above the company’s own 20-year CAGR of 12%. That acceleration is not being driven by one-off factors. It reflects the compounding benefits of branch productivity improvements, expanding inventory depth and a growing catalogue of parts that makes Multispares the go-to supplier for workshops and fleet operators.

To put the branch productivity numbers in context, average revenue per store reached A$15.2 million in FY25, up from just A$3.9 million in FY13. That is a nearly fourfold increase in per-branch output over 12 years, demonstrating that Supply Network does not just grow by adding new locations. It gets materially better at extracting revenue from each existing site through deeper product ranges, improved systems and stronger customer relationships.

Disciplined Capacity Expansion

Supply Network has a deliberate and disciplined approach to network expansion that avoids the pitfalls of overextending the balance sheet or stretching management attention. The near-term pipeline is well-defined and manageable:

- A new branch in Rosedale, New Zealand, opening from March 2026

- Capacity upgrades scheduled for three existing sites in early FY27, with Toowoomba in 1Q27, Perth in 2Q27 and Brisbane in 3Q27

- The current network of 26 branches provides a strong foundation with meaningful room to grow revenue per site before new greenfield locations are needed

This is not a business that chases growth through acquisitions. Management has been clear that its strategy is organic, with excess cash returned to shareholders rather than deployed on M&A. That discipline is a key part of the investment case. Supply Network reinvests in inventory, systems and site capacity to drive same-store growth, and distributes the rest. It is a simple model, executed consistently over two decades.

Structural Tailwinds in Australian Trucking

The industry dynamics underpinning Supply Network’s growth are not cyclical. They are structural, and they are moving in the company’s favour. Several long-term trends are converging to support growing demand for aftermarket truck and bus parts:

- Road freight volumes continue to grow faster than rail and coastal shipping, increasing the size and utilisation of the Australian truck parc

- The fleet is becoming more complex, with a wider range of makes, models and technology platforms requiring broader parts coverage and deeper technical expertise

- The industry is shifting from repair toward replacement, increasing the frequency and value of parts purchases per vehicle

- Workshops and fleet operators are increasingly favouring aftermarket suppliers over OEM dealers, prioritising service, availability and value over brand-specific channels

These trends play directly to Supply Network’s strengths. The company’s investment in inventory breadth and systems capability means it can serve the long tail of parts demand across a complex fleet more effectively than smaller independent distributors or OEM dealer networks focused on specific brands. That competitive advantage compounds over time as the truck parc grows and diversifies.

Financials and Earnings Outlook

The financial profile over the forecast period tells the story of a business that continues to compound at attractive rates while maintaining a clean balance sheet and strong returns on capital:

- Revenue grows from A$348.8m in FY25 to A$508.3m in FY28, representing a three-year CAGR of roughly 13%

- EBITDA improves from A$68.8m to A$104.3m over the same period, with stable gross margins around 43%

- NPAT moves from A$40.0m in FY25 to A$62.9m in FY28, an 18% CAGR that reflects genuine operating leverage

- EPS grows from A$0.94 in FY25 to A$1.48 in FY28

- Dividend yields build from 1.5% in FY25 to 3.4% in FY28, supported by a consistent payout ratio around 70%

- ROE remains elevated at 31% to 34% across the forecast period, and ROIC improves from 28.9% in FY25 to 35.9% in FY28

The balance sheet is pristine. Supply Network held A$22 million in net cash at the end of 1H26, with no debt. Free cash flow is expected to be A$46.5 million in FY26 and A$50.3 million in FY27, comfortably funding both dividends and ongoing investment in inventory and capacity. This is a business that generates cash well in excess of its growth requirements, which means shareholders receive a meaningful and growing income stream without the company needing to compromise its reinvestment program.

New Zealand Progress

New Zealand has been a tougher market for Supply Network, but the business is making headway. NZ sales grew 8.1% in 1H26, and management is working to align NZ systems and processes with Australian practices by the end of FY26. The new Rosedale branch opening in March 2026 will add to the company’s NZ footprint and provide incremental capacity to serve the growing parts demand in that market. While NZ is not the primary growth driver, it represents a meaningful option on further geographic expansion once the operating model is fully optimised.

Valuation

At A$34.53, Supply Network trades on approximately 32x FY26 earnings and 27x FY27 earnings. Those multiples look elevated on a standalone basis, but when assessed against the company’s growth profile and return on capital, they are reasonable. Research from a leading investment bank supports a Buy rating with a price target of A$38.10, using the blended DCF and PE approach outlined above. We agree with that framework.

The premium to auto distribution peers is warranted. A business delivering 13% revenue growth and 18% EPS growth over the forecast period, with 30%+ ROE and a net cash balance sheet, should not trade at 17x earnings alongside peers growing at mid-single digits. The question is whether the premium is sufficient, and on our numbers we think there is room for further upside as the market gives Supply Network credit for its sustained outperformance and improving cash generation.

On the M&A front, Supply Network has strategic appeal given its market-leading position in a niche and growing segment, though geographic complexity and the organic growth culture would make any acquisition process less straightforward. We assign a moderate M&A ranking and do not factor any takeover premium into our target.

Key Risks

The primary risk is competitive pressure from independent parts suppliers, wholesalers and OEM dealer networks. Supply Network’s competitive advantage is built on availability, catalogue depth and service quality. Any erosion in those areas, whether through new entrants, pricing aggression from competitors or supply chain disruptions from international suppliers, could impact growth rates and margins.

Reputational risk is meaningful in this business. Workshops and fleet operators depend on parts arriving quickly and being fit for purpose. Quality failures or service lapses could damage customer relationships that have taken years to build. Supply Network’s track record here has been strong, but it is a risk that requires ongoing attention as the network expands and the product catalogue grows.

Execution risk on new branches and capacity upgrades is manageable but worth monitoring. The Brisbane, Toowoomba and Perth upgrades in early FY27 represent a concentration of capital projects over a short period, and any delays could create short-term disruption to operations in those markets. Labour shortages across the logistics sector are an additional headwind that could constrain the pace of expansion or put upward pressure on operating costs.

Finally, unfavourable vehicle trends, such as a shift toward electric trucks that are less parts-intensive or a slowdown in road freight volumes, could impact the long-term demand outlook. We view these risks as low probability over our forecast horizon but relevant for longer-term investors.

Our View

Supply Network is a genuine compounder on the ASX. Twenty years of 12% revenue growth and 19% NPAT growth is a track record that very few Australian companies can match, and the business shows no signs of slowing down. Australian sales are accelerating, branch productivity continues to climb, the balance sheet carries net cash and management returns excess capital to shareholders rather than chasing acquisitions. The structural tailwinds in Australian road freight, increasing truck parc complexity and the shift toward aftermarket parts suppliers are durable and play directly to Supply Network’s competitive strengths. At A$34.53 with a credible path to A$38.10 over 12 months, we think the stock offers an attractive entry point into a high-quality industrial compounder with a long runway of organic growth ahead.

If you would like to discuss Supply Network or how it might fit within your portfolio, request a callback or call us on 1300 889 603.