Aussie Broadband is a telecommunications company that was formed in 2008. The Company’s main focus is offering NBN subscription plans and bundles to a wide range of customers including residential homes, small businesses, not-for-profits, corporates and managed service providers.

As a licensed carrier, ABB provides these services through a wholesale agreement with NBN Co, a mix of leased backhaul infrastructure from third parties and its own network equipment. The Company also offers a range of other telecommunications services including VOIP (voice over internet protocol), mobile plans and entertainment bundles through its partnership with Fetch TV and connections through the Opticomm network.

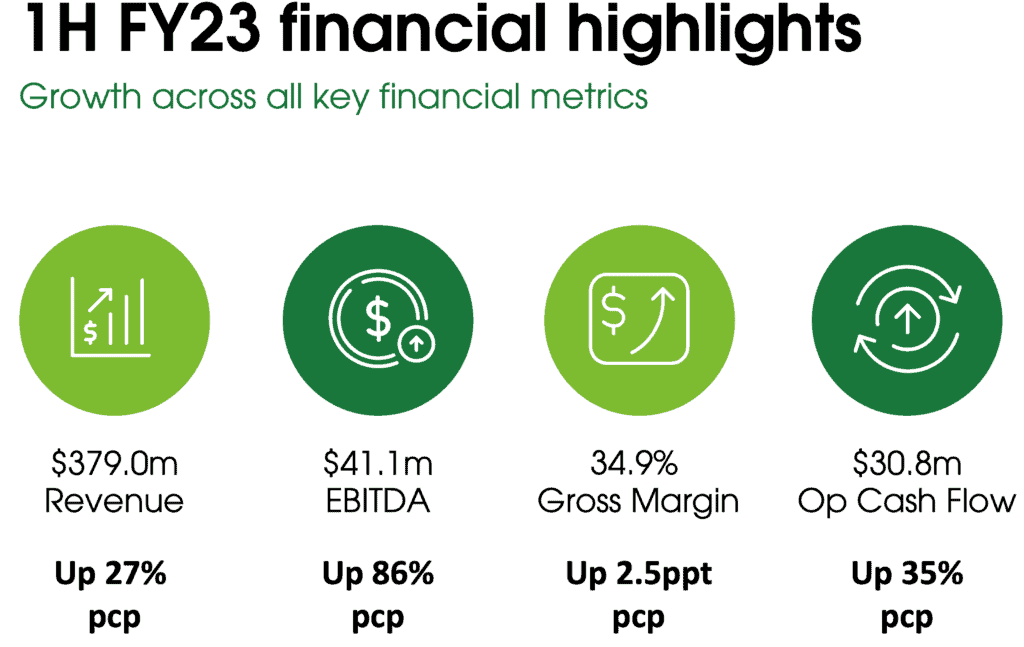

We like ABB because it’s one of the fast-growing telecommunication providers in Australia. This was demonstrated in their recent first half results presentation as ABB continues to show excellent subscriber growth. In fact, from a presentation slide below, ABB demonstrated that they have continued to grow across all key metrics when compared to last year. Revenue is up 27% to $379 million, EBITDA grew impressively by 86% to $41 million, with operating cash flow was up 35% to almost $31 million.

What’s also caught our attention is that the stock has substantially pulled back despite maintaining healthy subscriber growth, improved earning mix with prudent costs oversight. The pulled back from lofty valuation means ABB now trades at a more attractive valuation, and we think the stock is at a point where it represents an attractive buy.

TRADE ACTION

Quantity: Buy 1,000 shares

Entry: Buy up to $3.90

Stop Loss: $3.60

Target Price: $4.90