Today we have identified what we believe is an undervalued company on the ASX that is a long term beneficiary of the Covid-19 virus. The company is Australian clinical Labs (ACL) the third largest provider of pathology services in Australia

ACL is a relatively new company on the market having only been listed in May 2021.

The pathology market is dominated by Sonic Healthcare (SHL) and Healius (HLS) with ACL coming in third place with a 16% market share. ACL business services 90+ hospitals, operates 988 approved collection services, 80+ accredited laboratories and 30 specialist skin cancer clinics.

As per the company’s recently released FY 21 financial results, its first as a listed company Medicare funded pathology market had growth of 5.2% CAGR between FY2000 and FY2021. Modest growth but nothing spectacular, while ACL non-COVID revenue growth was 6.3% in FY21. So the underlying business is ticking along nicely even without the boat in COVID testing.

ACL also did one thing that all new companies must do when they first release financial results as a newly listed company, that is, to comfortably beat prospectus forecasts.

Revenue 4.2% ahead of prospectus

EBITDA 11.1% ahead of prospectus

NPAT 19.2% ahead of prospectus

What we believe the market is not taking into account and why we think the company is undervalued is potential for elevated levels of COVID testing for the next few years. No matter what you think about COVID it is in the community and likely to be circulating for years to come.

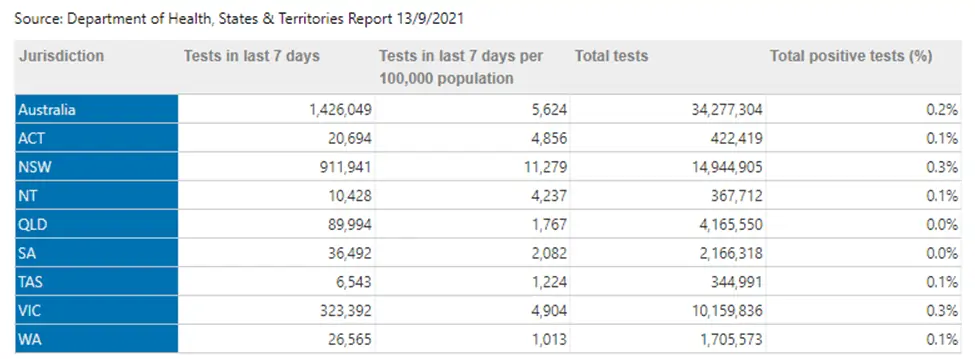

According to the department of health 1,426,049 tests have been completed in the last 7 days and this number is likely to remain steady or even increase.

As we have seen internationally even with countries like Israel which rolled out the vaccine early and led the race to vaccinate, inoculating almost 80% of its citizens by June. The lifting of restrictions, the re-opening of business, the discarding of face masks and larger public gatherings (weddings, sporting events) lead to a substantial increase in the number of cases. It is likely Australia will experience a similar increase in the number of cases as we reopen in the coming months.

The point is, continuing COVID testing will be required going forward for international and interstate (think WA) travellers, work related requirements, hospitals and clinics etc. Just because we reach the magical 70% vaccination rate does not mean testing stops. Each time one visits a doctor or feels a fever coming on, the response will be the same, we better get tested just in case.

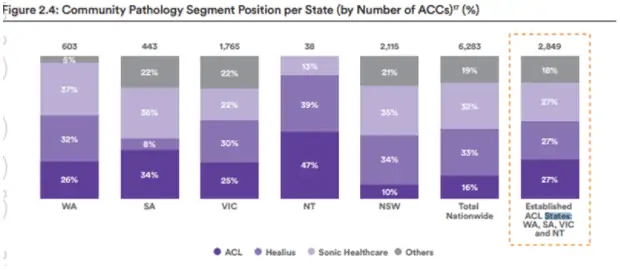

As per the chart from page 36 of the company’s prospectus, ACL is under-represented in NSW and QLD. With net debt excluding leases of $64m the company has more than enough head room to expand with small bolt on acquisitions, which they have started by acquiring Sun Doctors a leading skin cancer clinic business.

Risks

1.Development of new testing methods that replace the current PCR method (someone builds a better mousetrap)

2. Reduction in Medicare price for COVID PCR test

3.Relationships – business is referred to ACL from hospitals, doctors etc if a relationship breaks down the referred business might go elsewhere

In summary an underlying business growing modestly, potential for earnings accretive acquisitions that add to revenue and profit, the potential for earnings growth to accelerate if COVID testing rates remain elevated and the potential for dividends early in 2022. What’s not to like.

TRADE ENTRY DETAILS

Entry : Buy at a limit price of $4.40

Position Size : 2,000 shares

Stop Loss : $3.35

Initial Target Price : $5.50

Notes : The ACL share price closed at $4.45 yesterday typically we would set a limit buy price just above the last traded price to give subscribers room to enter a position. This time because the shares look like they will open slightly lower we are setting a limit buy price just under the last traded price. We are willing to sit back and let the market come to us.