The new recommendation today is relatively new company with a unique business model that should lead to significant dividend yield within two years. Deterra Royalties Ltd (DRR) came into existence via a de-merger from Iluka Resources (ILU) in October 2020.

Entry : Buy up to $4.35

Position size : 2,000 shares

Stop loss : No stop loss

Deterra’s main asset and the one that is of interest to us is the royalty steam the company receives over Mining Area C (MAC). MAC contains massive deposits of iron ore that are being mined by BHP. MAC has been in production since 2003.

From all the iron ore production in MAC Deterra derives two sources of income:

- 1.232% of Australian dollar Free On Board (FOB) revenue from each Dry Metric Tonne (DMT)

- One off $1 million payment per one million ton increase in annual production.

The MAC has two areas of production North and South Flank. The North Flank has been in production since 2003. Production from South Flank started this year and ramps up over the next two years. Current production rate is 57 million tonnes ramping up to 145 million tonnes over the next two years are South Flank production kicks in. Production is forecast to continue for at least 30 years.

The unique business model comes from the fact that the business requires limited initial investment and no ongoing capital expenditure to generate the royalty income. The operator of the mine BHP takes on all the risk and the capital cost to establish and keep production going in MAC.

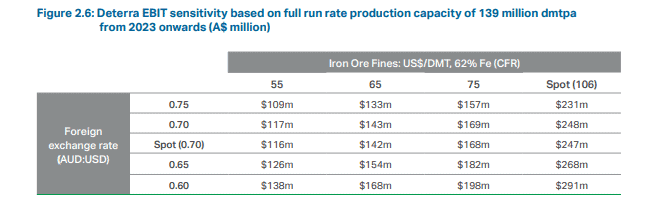

There are two factors that determine the royalty income the company receives; the iron ore price and the AUD:USD exchange rate. In the demerger booklet at the time of listing the table below was provided showing the EBIT when full production is reached based on varying prices for iron ore and the AUD/USD exchange rate.

Using some back of envelope calculation based on the current exchange rate and a future iron ore price closer to $100 the company should be generating EBIT in a range between A$200m to A$250m. The company intends to adopt a dividend policy to a payout ratio of 100% of net profit after tax. This should lead the grossed-up dividends to well over 5% in the next few years.

In the company’s most recent financial results released on the 18TH August the company announced

- Revenue of $145.2 million

- NPAT of $94.3 million

- EBITA of $135.50

- Final dividend of 11.52 cents per shares fully franked with an ex-dividend date of 2nd September

There is also a potential of some form of corporate action in the future as long term investors looking for reliable incoming generating assets.

The advantages of open a position

- Nice grossed up dividend yield

- Strong counter party in BHP that has deep pockets and a long history of running iron ore mines

- Long mine life of 30 years with the potential for this to be extended over time

The main risk I see is management they have a great asset in the MAC and have to do next to nothing over the next 30 years to generate good consistent returns. I am sure Investment Bankers will start whispering to management to take on debt and buy another asset to diversify. If management can resist doing deals this company will be a good dividend play with the potential for corporate action in the future. Management just needs to stick with KISS Keep It Simple Stupid.