Who is Megaport?

Megaport (MP1) is a leading software-defined networking platform that connects customers through data centers to cloud service providers and other network service providers in a very seamless way. Customers pay as they use – the same way as cloud consumption is consumed, in a very secure and on-demand fashion.

MP1 is also a first mover in the Network-as-a Service (NaaS) space and have built up a unique customer base which is extremely difficult to replicate.

For example, MP1’s nearest competitor is arguably the world’s largest data centre provider Equinix, however, Equinix is limited in its capacity to facilitate connections within its own 200 data centre locations, whereas, MP1 has over 700 locations and growing. Therefore, we see MP1 as a leader in the market as they’re unmatched in terms of diversity for their platform. Being in over 700 data centres and close to 250 cloud onramps clearly differentiates MP1 from the rest.

MP1 Growth Drivers

The first growth driver is MP1’s new product called Megaport Virtual Edge. This new product takes MP1 ‘s core platform beyond connecting data centres to enable businesses to connect to services through Megaport from more locations around the globe, such as branch offices, corporate campuses, and point-of-sale locations. What’s important here is that prior to this new product release, MP1’s clients were mostly data centres, however, the release of MVE broadens MP1’s ability to sell to anyone on a branch network (as opposed to just a head office) thereby broadening MP1’s total addressable market by 100%. This huge jump in addressable market is simply achieved because MVE is much more flexible product giving MP1 the ability to sell into that Small and Mid-size Enterprise (SME) market as opposed to just those large major head office networks. Importantly, with the launch of MVE, MP1 has gone from a 7 Billion addressable market to a 14 billion addressable market.

The other growth driver which we think will assist in propelling MP1’s earnings is their newly built partnership channel. MVE is an excellent product although MP1 need the right sales team to go to market. What MP1 have done is set up reseller partnerships with some of the giants of the networking industry. MP1’s direct sales team of 40 is now leveraging off Fortune 500 companies such as CISCO, VMware and Fortinet sales teams, thereby taking MP1’s direct sales team of 40 to an indirect sales team of 40,000.

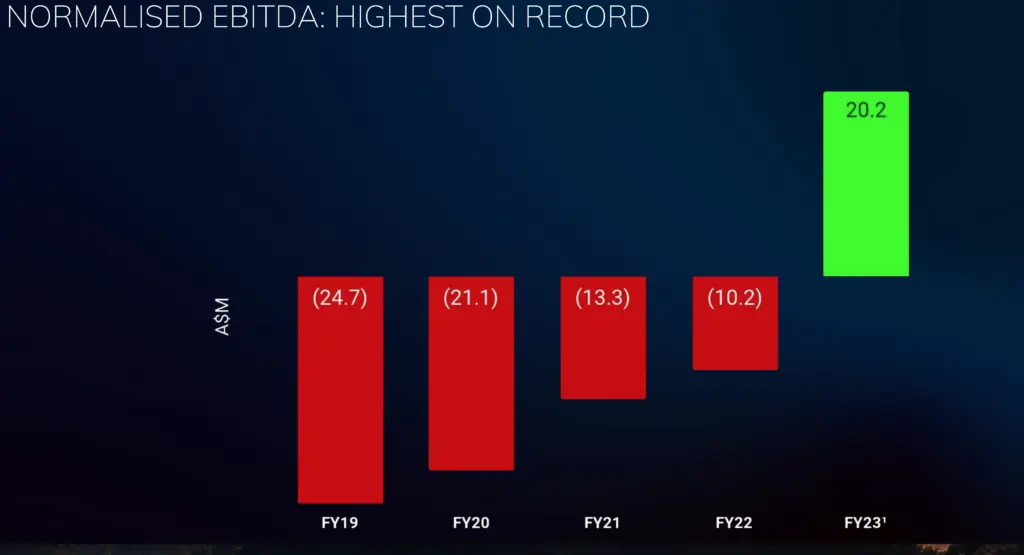

MP1’S Recent FY23 Results

It was clear from recent reporting that MP1’s core business is experiencing rapid record growth. Amongst the milestones announced include:

- Revenue growth up 40% (year on year).

- Gross profit up 52% (year on year).

- After posting 4 consecutive normalised EBITDA losses in FY 19, 20, 21 and 22, MP1 finally turned around its losing streak.

As the graph below shows, over the last 5 years, MP1 has increased it’s normalised EBITDA, from churning out negative $24.7 million in FY19 to turning positive (with the green line) of $20.2 million in FY23.

Although, since reporting, shares in MP1 have pulled back as much as 8%, now sitting 12% off its 52-week high.

The stock is currently trading in a triangle pattern where price is squeezing between buyers and sellers. As they squeeze towards each other, we think buyer will prevail given MP1’s growth potential along with its record FY23 highlights.

TRADE ACTION

Quantity : Buy 400 shares

Entry : Buy up to $11.70

Stop Loss : $10.50

Target Price:- No target price to start with. We will look to place a target price following the result half results on the 31st of October.