Today we are looking to take a position in one of the strongest stocks in the strongest sector (Consumer Discretionary) year to date. The purpose of this approach is to create greater alignment with the market, and let the market carry our stock selection higher.

Accent Group (AX1) is a footwear and apparel retailer and distributor with 750+ stores based in Australia and New Zealand.

AX1 started as a New Zealand wholesale distributor in 1988 and has since grown on to include 36 websites, 26 different retail banners and 9.3 million contactable customers.

AX1 has a number of stores, networks and distribution arrangements with global brands with expiration dates ranging from 2022 to 2032.

As a growth story, AX1 is placing increasing focus on owning more retail verticals just like the recent acquisitions of Glue Store in 2021 along with the rollout of Stylerunner.

The business has a strong store roll-out opportunity, with incremental store opportunities from key footwear banners (Sketchers, Platypus) and growth in apparel banners (Glue, Stylerunner & Nude Lucy). Reports suggest AX1 is on track to open around 50 new stores in H1 ’23 and targeting a growing customer database to 10 million customers in FY ’23.

In addition to its retail footprint, AX1 has a distribution business with exclusive distribution rights to a number of high growth global brands (Dr Martens, CAT, Timberland, Hoka, Vans) for the Australian market. The combination of the distribution business, vertically owned brands, and a store network – presents a growing opportunity to increase gross margin through vertical integration.

While there have been concerns on weakening economic growth, the young Australian consumer (age 15 -24) has proven to be very extremely resilient (when compared to the US) to inflationary and broader economic pressures given (1) a high proportion live at home; (2) more than two-thirds are working; (3) high and increasing minimum wage entitlements and; (4) a heavy skew towards discretionary spending.

Not surprisingly, on the 24 of February 2023 at AX1’s most recent trading update, management mentioned trade for the first 7 weeks of H2 has been positive. Like-for-like sales were up 16% in the prior year and including week 27 for the last 8 weeks are were 24%. Noting the first 7 weeks of H2 last year were significantly impacted by Covid.

Financials

In regard to the financials, group sales are now approaching $1.3 billion, up 11.3% to the prior year. This was despite losing 95 million to in FY22 due to government mandated lockdowns (July to October).

AX1’s net profit is expected to grow from a $32 million in FY22 to $68 million net profit in FY23, followed by $79 million net profit in FY24.

AX1 has a strong net cash balance of $85 million in the bank with 550 million debt. Although management said they don’t expect to take on more debt as circumstances over the last couple of years have been unusual. Further, when AX1 has excess cash, they will use that cash to either reduce debt or provide dividends to shareholders.

In regard to dividends, AX1 is looking to provide shareholders with a fully franked dividend of 12 cents per share (roughly 6% yield) for FY23.

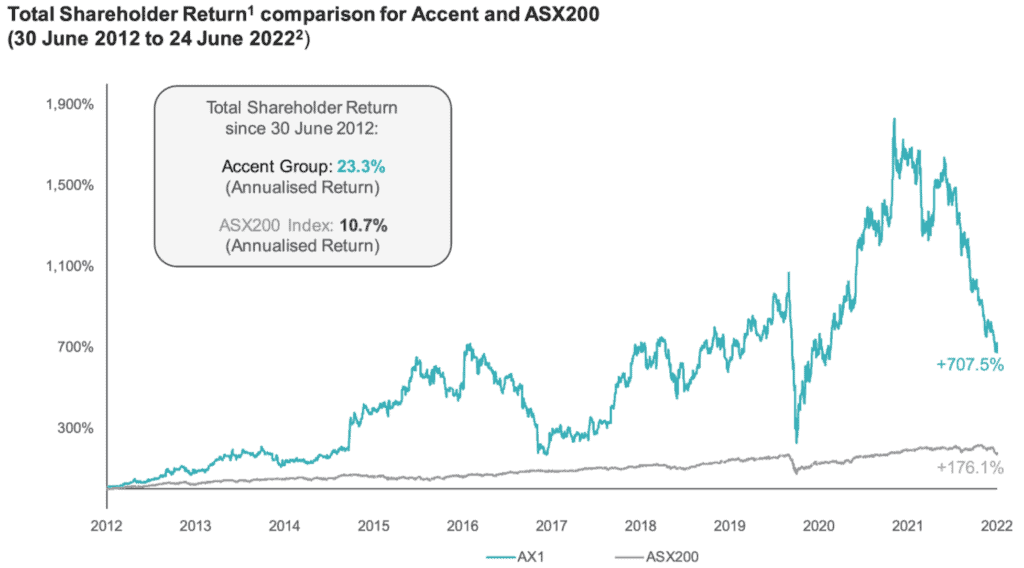

Turning to the graph below, in spite of a disrupted FY ’22 year, and since 2012, AX1 has delivered a 23.3% per annum compounding annualized return, outstripping that of the ASX 200 at 10.7% per annum compounding annualized return. This is evidence AX1 has delivered long-term shareholder growth over the last 10 years – which is more than double that of the ASX 200.

Not surprisingly, year to date AX1 continues to show strength when compared to the ASX 200 (white) and the Small Ordinaries Index (orange).

Finally, we believe there is significant upside still to come from AX1 regarding 1) store roll outs in key footwear banners, 2) margin expansion from global distribution brands, and 3) margin upside from growing vertical products i.e. rolling out compelling apparel (which compared to footwear) offers a greater opportunity to grow higher margin vertical sales.

TRADE ACTION

Quantity : Buy 2,000 shares

Entry : Buy up to $2.32

Stop Loss : $2.00

Target Price : $2.90