Seven West Media (SWM) is a national media business with both old and new media assets, with the former comprising of free to air tv, the West Australian newspaper, and an array of regional newspapers and radio stations whilst the latter includes assets such as Seven plus (digital).

In recent news, SWM completed the acquisition of Prime Television in late 2021, extending the companies reach not just into metropolitan but rural and regional areas. The combination of SWM and Prime gives advertisers one platform to reach audiences nationwide. This is a significant advantage over the competition at channel 9.

Importantly as part of the Prime takeover, SWM entered into a new funding facility in October 2021, which halved funding costs from the previous facility.

SWM saves on the interest rate, and estimates cost synergies of $5m to $10m on an annual basis to be achieved in 12 to 18 months from the merger with prime.

Plus, as prime did not have a stake in the seven networks’ digital assets, they did not advertise this product at the end of segments, leading to lower uptake in regional areas. Digital revenue is undoubtedly the future. SWM has increased digital revenues steadily over the last few years. If SWM can replicate digital uptake with the Prime audience, digital revenue will continue to grow and form an increasing part of overall revenue.

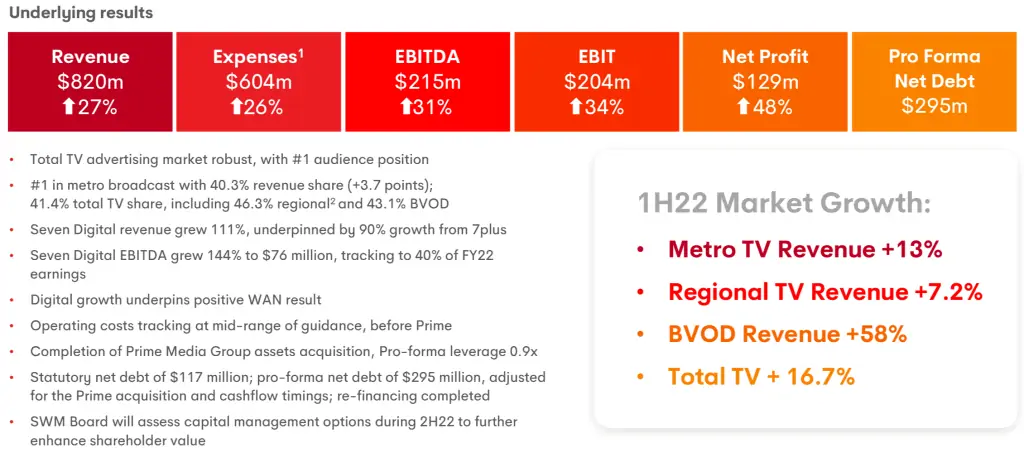

SWM results released on the 15th, February were broadly positive, with Net Profit increasing to $129Million.

What does the future hold for SWM?

Management has upgraded their FY22 EBITDA guidance to $315 – $325m. They can upgrade guidance based on several factors:-

- Digital revenue will continue to increase, reaching 40% of revenue in FY22

- As lockdowns end, the advertising market is recovering. Meto free to air ad market grew 13% in 1H22. This growth is likely to accelerate

- Rating tailwind from the winter Olympics

- The return of the Voice, which is apparently Australia’s number1 rated tv series

- Australian federal government election must be held no later than 21 May 2022. Spending on election ads only increases each election cycle.

So there is a lot to like going forward, and no reason guidance can not be met.

They also mentioned that the SWM board would assess capital management options during 2H22 to enhance shareholder value further. With Pro-forma net debt of $295m adjusted for the prime acquisition, the company trades on a leverage ratio of 0.9, below the company’s target range of 1 – 1.5x.

Further, capital management might take the form of dividends or buybacks. The announcements of either a dividend or buyback are likely to increase the share price and attract more investor interest from the investment community.

Lastly, SWM offers exceptional value in a market that has switched from growth to value. Therefore, we see no reason why the share price can not trade back to recent highs.

Trade Action

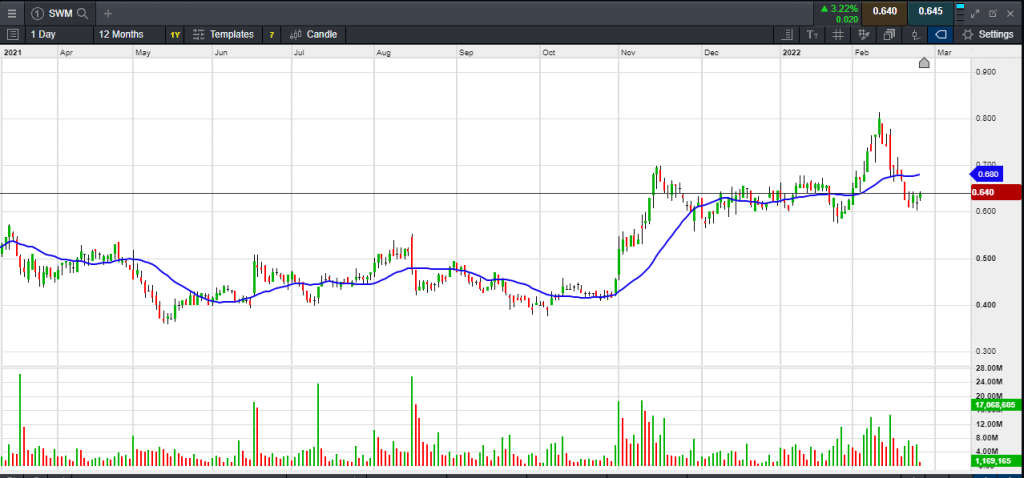

Entry: Buy 10,000 shares paying up to $0.65

Stop loss: $0.47

Target price: $0.90