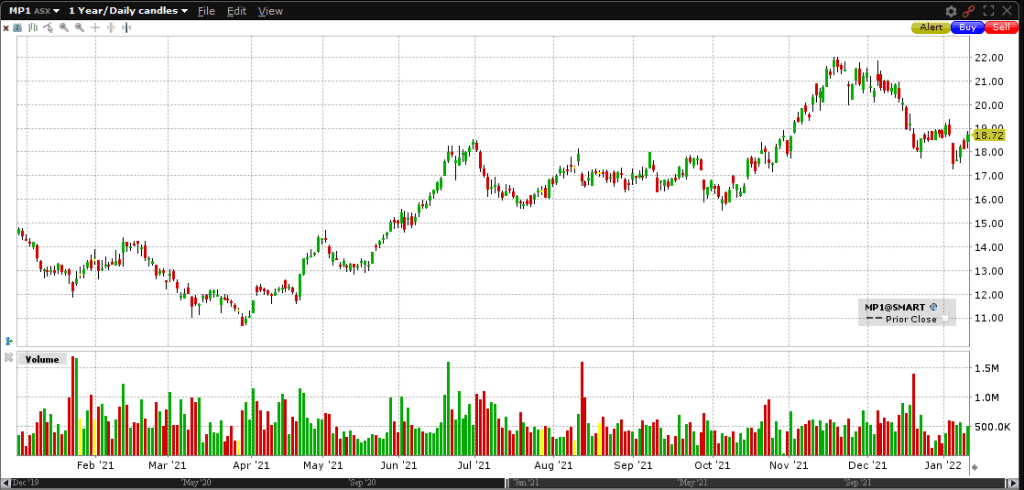

For those who are familiar with receiving MF & Co free research may remember we analysed a company called Megaport (MP1) in March 2021.

Here we outlined how MP1 is a Software-Defined Networking (SDN) company founded in Australia in 2013 and has become a leading global provider for software-based elastic interconnection services.

For those wanting to get up to speed with MP1 operations, a full recap of this research can be found here.

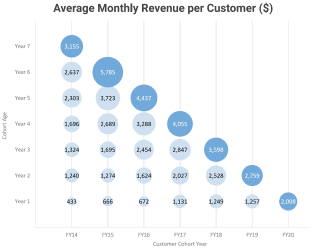

We continue to like MP1 as the core business is experiencing extremely low levels of customer churn (less than 1%). At the same time, MP1 customer spend is rising by 50 % every year. This tells us MP1 has built an exceptionally loyal customer base who spend more year on year, highlighting MP1 excellent organic growth. The below graph highlights MP1 average customer spend increase 50% year on year:

We also like the fact that MP1 is the first mover in the Network-as-a Service (NaaS) space who have built up a unique customer base which is extremely difficult to replicate.

MP1 nearest competitor is arguably the world’s largest data centre provider Equinix, however, Equinix is limited in its capacity to facilitate connections within its own 200 data centre locations, whereas, MP1 has over 700 locations and growing

Therefore, we see MP1 as a leader in the market as they’re unmatched in terms of diversity for their platform. Being in over 700 data centres and close to 250 cloud onramps clearly differentiates MP1 from the rest.

Furthermore, MP1 continues to innovate products within their NaaS category as MP1’s founder Bevan Slattery has a knack of foreseeing telecommunication problems and building solutions in advance. Bevan is also aware of customer demands where agility and flexibility is the name of the game. Being faster and cheaper than traditional telecommunication companies has also seen MP1 growth rate exceed 50% pa over the last 3 years

Given this, MP1 has built a powerful global network effect (below) where they are constantly adding more and more service providers to their ecosystem which compound the value of the platform. Importantly, being the first mover in this space will only make MP1 difficult to compete with as they capture greater US and European market share in conditions where businesses are increasingly adopting agile networking.

There are also 2 other growth drivers which, when combined, have the potential to significantly change the earnings outlook for this stock.

The first growth driver is MP1’s new product called Megaport Virtual Edge. This new product takes MP1 ‘s core platform beyond connecting data centres to enable businesses to connect to services through Megaport from more locations around the globe, such as branch offices, corporate campuses, and point-of-sale locations.

What’s important here is that prior to this new product release, Megaports clients were mostly data centres, however, the release of MVE broadens MP1’s ability to sell to anyone on a branch network (as opposed to just a head office) thereby broadening MP1’s total addressable market by 100%.

This huge jump in addressable market is simply achieved because MVE is much more flexible product giving MP1 the ability to sell into that Small and Mid-size Enterprise (SME) market as opposed to just those large major head office networks. Importantly, with the launch of MVE, MP1 has gone from a 7 Billion addressable market to a 14 billion addressable market.

The other growth driver which we think will assist in propelling MP1’s earnings is their newly built partnership channel. MVE is an excellent product although MP1 need the right sales team to go to market. What MP1 have done is set up reseller partnerships with some of the giants of the networking industry. MP1’s direct sales team of 40 is now leveraging off Fortune 500 companies such as CISCO, VMware and Fortinet sales teams, thereby taking MP1’s direct sales team of 40 to an indirect sales team of 40,000.

In Summary, MP1 have a proven product and service which has experienced low customer churn and yearly increase in customer spend. They also have a unique product offering and customer base that will be difficult for competition to replicate – particularly through the lens of the above network effect. When adding the two growth drivers of MP1’s new product (MVE) that increases their addressable market by 100% together with a sales force army of 40,000, we believe the time is now for MP1 and expect positive news flow regarding an uplift in sales momentum with new customers, ports, services along with healthy revenue.

Trade Action

Buy 525 MP1 paying no more than $19.00

Stop loss $15.50

Profit target $30.00