Johns Lyng Group (ASX: JLG) is an integrated building and services group delivering building and restoration services across Australia and the USA.

The company provides building fabric repair, contents restoration, hazardous waste removal, strata management services, residential and commercial flooring, emergency household repairs, shop-fitting, HVAC mechanical, and pre-sale property staging services.

The company’s success has been built around work for insurance companies. With climatic catastrophes increasing (the rain in Sydney this year is an example) each time a house needs to be rebuilt or restored following a fire or flood, JLG, through its Insurance Building & Restoration Services (IB&RS) business, bids on the work.

Notably, the Insurance Building and Restoration Services (IB&RS) work is non-discretionary. Therefore, if a fire, flood, or other natural disaster damages your residence, work must be undertaken to make the home habitable again. It is not a case of getting around to a new kitchen fit-out at some point in the future. Work must be completed.

As mentioned in the previous market update, we highlighted characteristics we look for in leading stocks, and JLG showed remarkable strength off the bottom during July when compared to the rest of the market that was starting to show signs of turning. JLG has had a highly volatile share price despite stable and improving earnings.

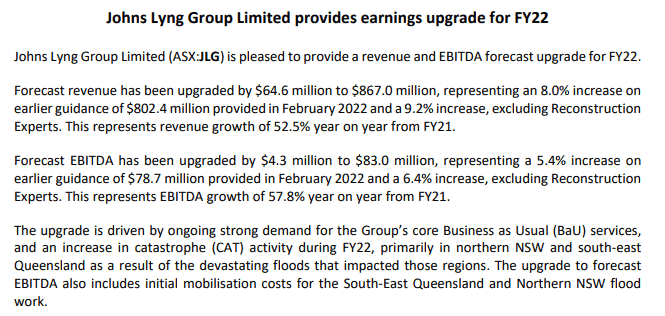

Although, the recent weather events over the second half of 2022 as well as the underlying business outperforming saw JLG increase its FY22 guidance on the 9th of June. As JLG stated, below:

We see further opportunities arising from continued growth in Australia across it’s IB&RS division, a healthy pipeline of catastrophic works given recent weather events, along with a meaningful expansion into the US through JLG’s recent acquisition of Reconstruction experts.

We believe this recent acquisition provides a springboard into launching JLG’s full suite of capabilities into the US. Reconstruction experts has a well-established business (in Colorado, Florida, California, and Texas) with authorisations in place to work in another 13 states. With 80% of its revenues generated from defect and damage insurance-related work (fixing construction defects and man-made or weather-related property damage). As a new shareholder, we are excited by this platform for further US expansion as JLG is a pioneer in its field of expertise, disrupting a fragmented market. Therefore, if JLG can replicate its success from the Australian market in the USA, strong revenue growth could continue for many years.

The main risk we see going forward is the increasing costs for labor and the construction materials to complete the works the company undertakes. But with a CEO who has been in the job for more than 17 years and a well-established board, they are well position to manage the risks.

When you look at the company’s value, the current forward PE is 50.3 times earnings, but if the company can continue its current growth trajectory, the high PE will very quickly be reduced.

If natural disasters keep occurring in number and severity, JLG is in the box seat to be profitable well into the future.

Please see our previous research report on JLG conducted on April 7, 2022

Number of shares: 1,000

Buy up to: $7.85

Stop Loss: $6.85

Target: $9.25