During reporting season, there are certain news events that can send a stock propelling in an upward direction. Some of these include an announcement about improved margins, an increase in market share, revenue significantly better than expected, or raising guidance going forward.

We want to focus on the last two. Any time you read a company that comes out with revenue significantly better than expected, this can create a powerful move to the upside given that revenue is a crucial gauge of how the core business is performing.

Similarly, when a company comes out and raises guidance going forward, this can drastically change investors’ expectations of the stock’s upside. Since the market looks 6 – 8 months ahead, a company’s guidance is more important than the bottom line for any reported quarter (an important distinction to understand).

For this reason, we are establishing a new position in the building and restoration businesses of Johns Lyng Group (ASX code JLG) on the back of today’s reporting where both revenues are significantly better than expected along with raising guidance going forward.

The major highlights of reporting include:

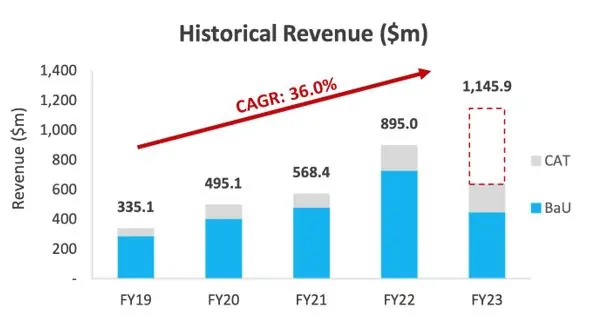

- Group Sales Revenue for the period increased by 71.2% on 1H22 to $635.6 million

- Net Profit After Tax (NPAT): $34.1m / +83.6% (1H22: $18.6m)

- Full-year forecast Group Sales Revenue has been upgraded to $1.146 billion – previously forecasted 1.080 billion in August 2022 (11.2% upgrade)

JLG finished the half with a solid net cash balance of $29 million and the company noted in this morning’s conference call that they have sufficient balance sheet capacity to fund organic growth and bolt-on acquisitions.

A recap of our previous research on JLG in April 2022 can be found in the below link:

Position Size: 1,000 shares

Entry: Buy up to $6.55

Stop Loss: – $6.00

Target Price: – $7.50