Sigma Healthcare (ASX: SIG) has been in the news lately due to its merger with top pharma retailer Chemist Warehouse Group. The merger has created one of Australia’s largest players in the pharmaceutical space.

While the company has taken a beating lately due to some profit-taking by institutional investors/promoters/franchise operators and a closure of the trading window before FY25 results, the long-term opportunity looks great due to the prospects of the merged entity.

The stock was recently included in the MSCI World index and is slated to be included in the FTSE World index next month which should trigger a massive wave of buying. Over the past month, the MSCI index inclusion involved serious selling by franchise operators following which price rebounded swiftly to new highs.

Table of Contents

- 1 About Sigma Healthcare (ASX: SIG)

- 2 Integrated Model And Scale Are Strengths

- 3 Customer Centricity, Regulatory Risk, And Macro Uncertainty Are Weaknesses

- 4 Domestic Growth, Private Labelling, And Ancillary Services Are Opportunities

- 5 Competitive Pressure, Execution Risk, And Oversupply Of Shares Are Threats

- 6 Financial Performance

- 7 Conclusion

About Sigma Healthcare (ASX: SIG)

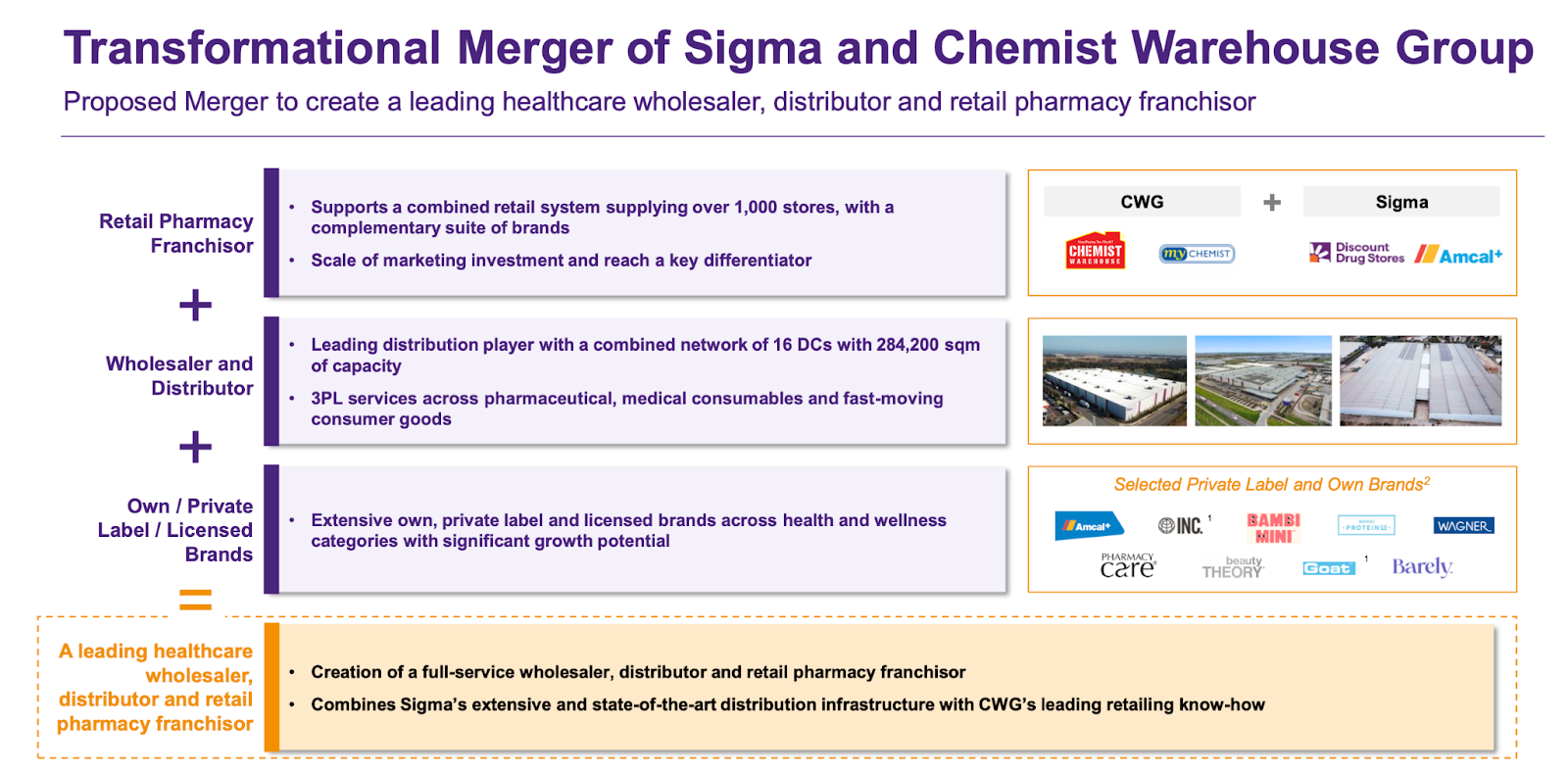

Sigma Healthcare Limited has emerged as a pivotal entity in Australia’s pharmaceutical distribution and retail pharmacy sector following its transformative merger with Chemist Warehouse Group (CWG).

Source – FY25 Roadshow Presentation

This integration combines Sigma’s robust wholesale and logistics infrastructure with CWG’s extensive retail network, creating a vertically aligned healthcare powerhouse. The merger, valued at over $8 billion, positions the combined entity among Australia’s top 100 companies, with a strategic footprint across wholesale, distribution, and franchised retail operations.

Sigma’s state-of-the-art distribution centers and CWG’s consumer-centric retail model, aiming to redefine market dynamics through operational synergies and expanded service offerings.

The post merger Sigma Healthcare has a market capitalization of A$37.4 billion at time of writing.

Integrated Model And Scale Are Strengths

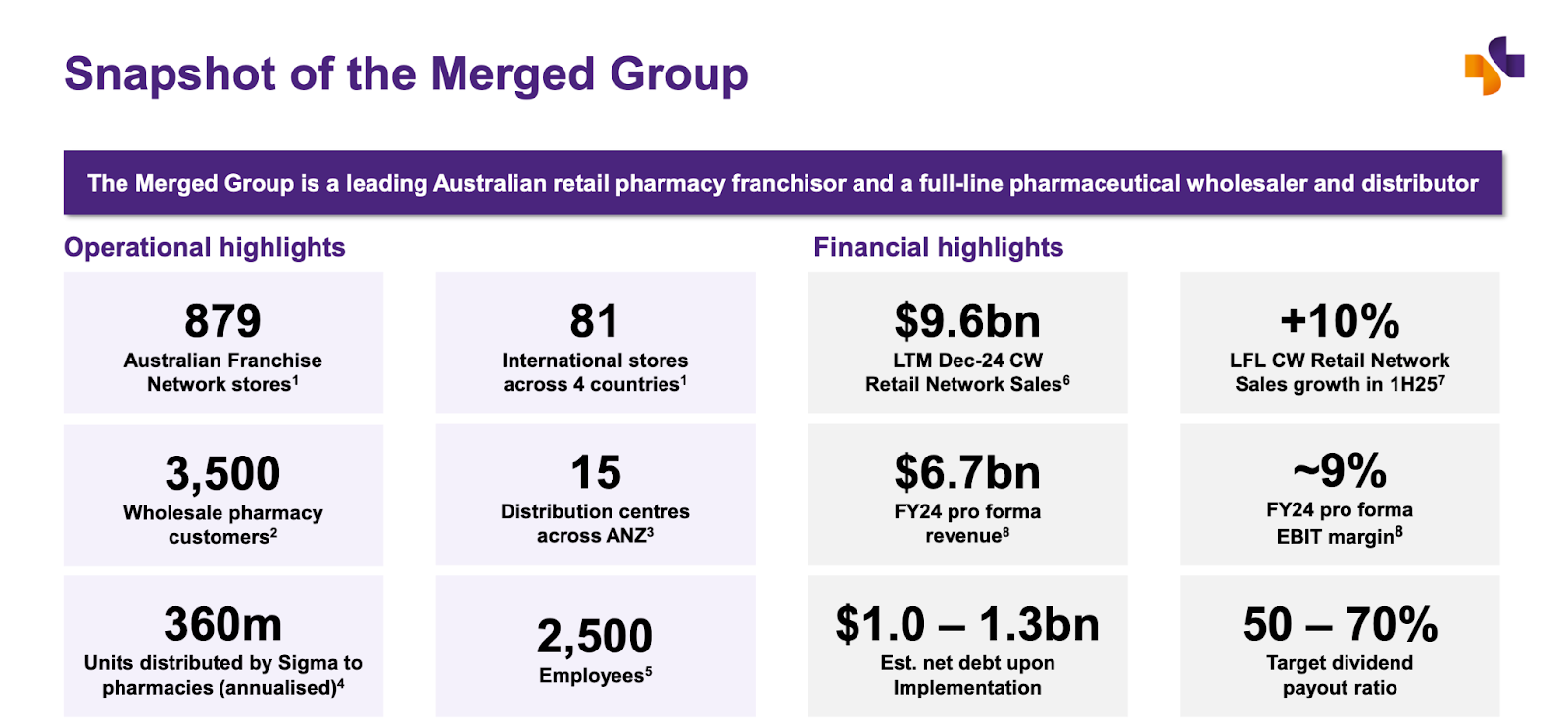

The combination of Sigma Healthcare (ASX: SIG) and Chemist Warehouse positions it as Australia’s largest integrated pharmaceutical wholesaler and retail franchisor, servicing over 3,500 pharmacies and commanding approximately 16% of the retail pharmacy market. This scale translates into significant bargaining power with suppliers, allowing the group to negotiate better pricing, secure exclusive product lines, and expand private-label offerings.

Source – FY25 Roadshow Presentation

Chemist Warehouse’s retail network has demonstrated sustained growth, with a consistent like-for-like sales increase averaging around 10% annually over recent years, while Sigma’s wholesale business has shown steady growth and operational resilience. The merger thus creates a diversified revenue base spanning wholesale distribution, franchise fees, advertising income, and private-label product sales, enhancing financial stability.

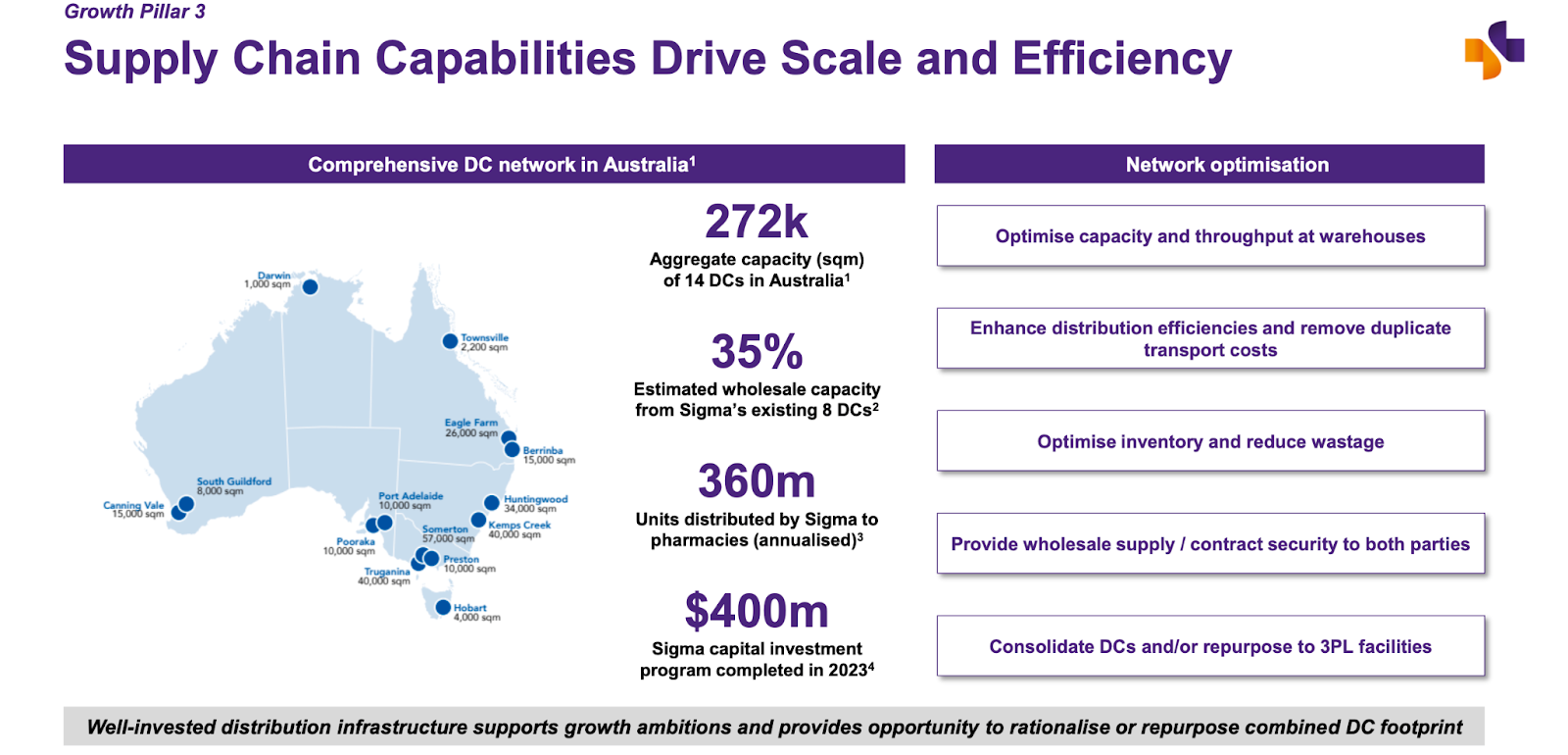

The merged entity’s distribution network stands as a cornerstone strength, comprising 15 strategically located distribution centers across Australia and New Zealand. These facilities enable the annual distribution of over 360 million units to pharmacies nationwide with delivery-in-full rates consistently exceeding 99%. The merger amplifies these capabilities by integrating CWG’s retail expertise, which includes a network of 879 Australian franchise stores and 81 international outlets.

Operational resilience is another critical strength. Sigma’s $400 million capital investment in infrastructure over four years has created excess distribution capacity, allowing seamless absorption of CWG’s supply contract volumes. This investment ensures the merged group can efficiently fulfill the new five-year Chemist Warehouse supply contract, which alone represents approximately $3 billion in annualized sales starting July 2024. The ability to scale without immediate need for further capital expenditure provides a competitive edge and supports aggressive growth plans.

Source – FY25 Roadshow Presentation

This scale not only supports the efficient supply of an extensive product range but also enables the merged entity to optimize warehouse capacity, consolidate transport routes, and reduce duplication, contributing to targeted annual cost synergies of approximately $60 million to be realized within four years. For example, the consolidation of CWG’s Preston distribution center with Sigma’s Truganina facility is expected to reduce freight expenses by over 8%, highlighting tangible operational efficiencies.

Lastly, brand strength and marketing capability are additional pillars of the merged entity’s competitive advantage. Chemist Warehouse is one of Australia’s most recognized retail pharmacy brands, known for its warehouse-style stores that offer a broad assortment of discounted pharmaceuticals, beauty, wellness, and front-of-store products.

This brand recognition drives high foot traffic and customer loyalty, supported by extensive advertising campaigns across television, radio, print, and digital media. Sigma complements this with its heritage pharmacy brands such as Amcal and Discount Drug Stores, which are undergoing revitalization through brand consolidation and enhanced franchisee support.

Customer Centricity, Regulatory Risk, And Macro Uncertainty Are Weaknesses

A historical vulnerability for Sigma (ASX: SIG) has been its dependence on a concentrated customer base, which previously exposed it to revenue volatility. Although mitigated by the CWG supply agreement, this risk persists in the wholesale segment, where client attrition could impact margins.

Regulatory scrutiny remains a persistent threat, as evidenced by the ACCC’s court-enforceable undertakings during the merger approval process. These mandates could limit strategic flexibility in pricing and supplier negotiations.

The global tariff war unleashed by the Trump administration could pose operational challenges for Chemist Warehouse’s international store footprint as it could lead to supply chain disruption and higher costs. This is very important to CWG’s business model as most of its over-the-counter/wellness goods are sourced from heavily tariffed destinations such as China.

Domestic Growth, Private Labelling, And Ancillary Services Are Opportunities

Domestic store rollout presents the biggest growth opportunity for Sigma Healthcare (ASX: SIG). Chemist Warehouse has a proven track record of sustained expansion, opening an average of 30 new stores annually over the past decade. The merged group plans to maintain this pace, targeting over 1,300 outlets by 2030.

This expansion is supported by under-penetrated markets in certain Australian states and territories, where the group can increase its franchise presence, including through the conversion of pipeline stores and legacy Sigma pharmacies to the Chemist Warehouse brand. The revitalization of Amcal and Discount Drug Stores also offers organic growth potential by enhancing retail propositions and attracting new franchisees.

International expansion presents another significant opportunity. Chemist Warehouse’s existing footprint in New Zealand, China, Ireland, and Dubai demonstrates the brand’s transportability and acceptance in diverse markets.

The merged entity intends to take a measured approach to growth in these geographies, leveraging Sigma’s distribution expertise to support supply chain efficiency and product availability.

China, in particular, represents a large and rapidly growing healthcare market, where the group currently sells front-of-store and over-the-counter products. Expansion into new international markets is also under evaluation, potentially broadening revenue streams and reducing reliance on the Australian market.

Private-label proliferation is another key opportunity. With CWG’s retail network generating $821 million in private/exclusive label (PEL) sales in FY24, Sigma aims to expand this segment to 10% of total revenue by FY26. The launch of celebrity-endorsed product lines, such as the Messi fragrance range, exemplifies the potential for brand-driven margin expansion.

Source – FY24 Results Presentation

Sigma is actively building internal capabilities to accelerate product development and market penetration. With over 250 products in the pipeline and plans to launch 80% of these in the near term, Private label sales are targeted to grow by 50% in FY25. This expansion diversifies income sources and enhances customer loyalty through unique product offerings.

Omnichannel retailing to further augment growth prospects. Chemist Warehouse’s online platform, which accounted for approximately 16% of sales in FY24, offers a seamless shopping experience through click-and-collect and fast delivery options.

The merger enables integration of Sigma’s logistics capabilities with CWG’s digital infrastructure, enhancing customer convenience and supporting evolving consumer preferences toward online healthcare shopping. This omnichannel approach also supports expanded marketing reach and data-driven customer engagement.

Third-party logistics (3PL) services represent an additional growth avenue. Sigma’s expanded distribution facilities, notably the Truganina DC extension, have increased capacity for temperature-controlled warehousing and logistics services.

The 3PL business, which serves pharmaceutical, medical consumables, and fast-moving consumer goods sectors, has demonstrated revenue growth of 17% and good capacity utilization. The merged group plans to leverage this platform to pursue new contracts and expand margin-accretive logistics services, further diversifying revenue.

Source – FY24 Results Presentation

Competitive pressures are intensifying, with rivals like EBOS Group (Symbion) and API Retail aggressively expanding their wholesale and retail footprints to compete with Sigma Healthcare’s (ASX: SIG) integrated model. Additionally, the shift toward online pharmacies and quick commerce could erode foot traffic in traditional retail stores, challenging CWG’s brick-and-mortar dominance.

The integration timeline introduces execution risk. Historical precedents suggest cultural misalignment and system incompatibilities could delay synergy realization. The merged entity’s $1.3 billion net debt position-funded partly through a $1 billion facility from ANZ and NAB-exposes it to interest rate volatility, particularly in a tense macro environment.

Lastly, the promoters of the Chemist Warehouse Group (the Vance and Verrocchi families) who own 49% of the merged entity have just landed themselves a liquidity event as CWG was private before this merger. While the transactions have covenants on when and how much they could sell, the families can resort to selling up-to 100% of their stake by August 2026, which could put pressure on prices due to their massive position.

Financial Performance

Sigma Healthcare’s (ASX: SIG) financial trajectory from FY24 to HY25 reflects a period of strategic transformation, marked by operational improvements, merger-related costs, and the integration of Chemist Warehouse Group (CWG).

FY24 saw Sigma pivot toward its merger with CWG. While statutory sales revenue declined 9.2% to $3.32 billion due to reduced RAT (Rapid Antigen Tests) and hospital segment sales, like-for-like revenue grew 4.3%.

EBIT rose 62.7% to $31.4 million (excluding $8.2 million in merger costs), reflecting cost efficiencies and warehouse productivity gains. A $400 million equity raise strengthened the balance sheet, leaving net cash at $356.5 million.

However, the year ended with a net loss of $13.8 million after absorbing merger-related expenses. Key milestones included securing a five-year CWG supply contract ($3 billion annualized revenue) and advancing private-label product development.

For FY25, we have very limited data as the combination happened midway through the year. Sigma Healthcare Limited’s trading update following its merger with Chemist Warehouse Group (CWG) highlights robust financial performance for the nine months ending March 31, 2025.

The Group’s Normalised EBIT growth is broadly consistent with the 36% growth achieved by CWG for the first half of FY25 compared to the same period in FY24. CWG’s Statutory EBIT for 1H FY25 was $438.0 million, a 35% increase from $324.3 million in 1H FY24.

Transaction costs recorded were $8.1 million for 1H FY25, similar to the $8.6 million incurred for the entire FY24. Excluding these transaction costs, Normalised EBIT for 1H FY25 reached $446.1 million, reflecting a 36% increase from $328.4 million in 1H FY24.

Sigma plans to release its full statutory results for the twelve months ending June 30, 2025, in August 2025.

Conclusion

The Sigma-Chemist Warehouse (ASX: SIG) merger creates Australia’s largest integrated pharmaceutical entity, blending wholesale efficiency with retail agility. While short-term financial headwinds-including integration costs and debt servicing-are evident, the strategic rationale remains compelling.

Success hinges on seamless execution of synergy initiatives and leveraging CWG’s brand equity to drive private-label growth. The merger’s long-term value proposition lies in its ability to drive growth through scale, innovation, and consumer-centric solutions.

The combined size of the entity is slated to drive a wave of passive investment due to its inclusion in the ASX200. Hence, the dip due to profit booking/promoter sales before closure of the trading window combined with a solid outlook for results presents an opportunity for investors.