Spark New Zealand (ASX: SPK) is the leading telecom player in New Zealand with a dominant market position across the entire communications sector. The company is currently facing a very tough operational environment driven by New Zealand’s persistent macroeconomic woes.

After a steep correction, we believe the stock is poised to deliver solid returns as conditions ease given its long-term prospects, cheap valuation, and strong dividend yield.

Table of Contents

- 1 Introduction

- 2 Scale, Pricing Power, And Low Discretionary Exposure Are Strengths

- 3 Slow Growth, Competitive Market Environment And Regulatory Exposure Are Weaknesses

- 4 Data Centres, Enterprise 5G, Asset Monetization, Value Addition And Government Digitization Are Opportunities

- 5 Macro Weakness And Saturation Are Threats

- 6 Spark Financials

- 7 Conclusion

Introduction

Spark New Zealand Limited (ASX: SPK) stands as one of New Zealand’s largest telecommunications and digital services companies, providing essential connectivity and technology solutions across the nation. Formerly known as Telecom New Zealand until its rebranding on August 8, 2014, Spark has evolved from a traditional telecommunications provider to an integrated digital services company.

Source – Spark Strategy Presentation 24-26

The company delivers fixed-line telephone services, mobile services, broadband, and digital technology services including cloud computing, security, digital transformation, and managed services to a diverse customer base ranging from individual consumers to government agencies and large enterprises.

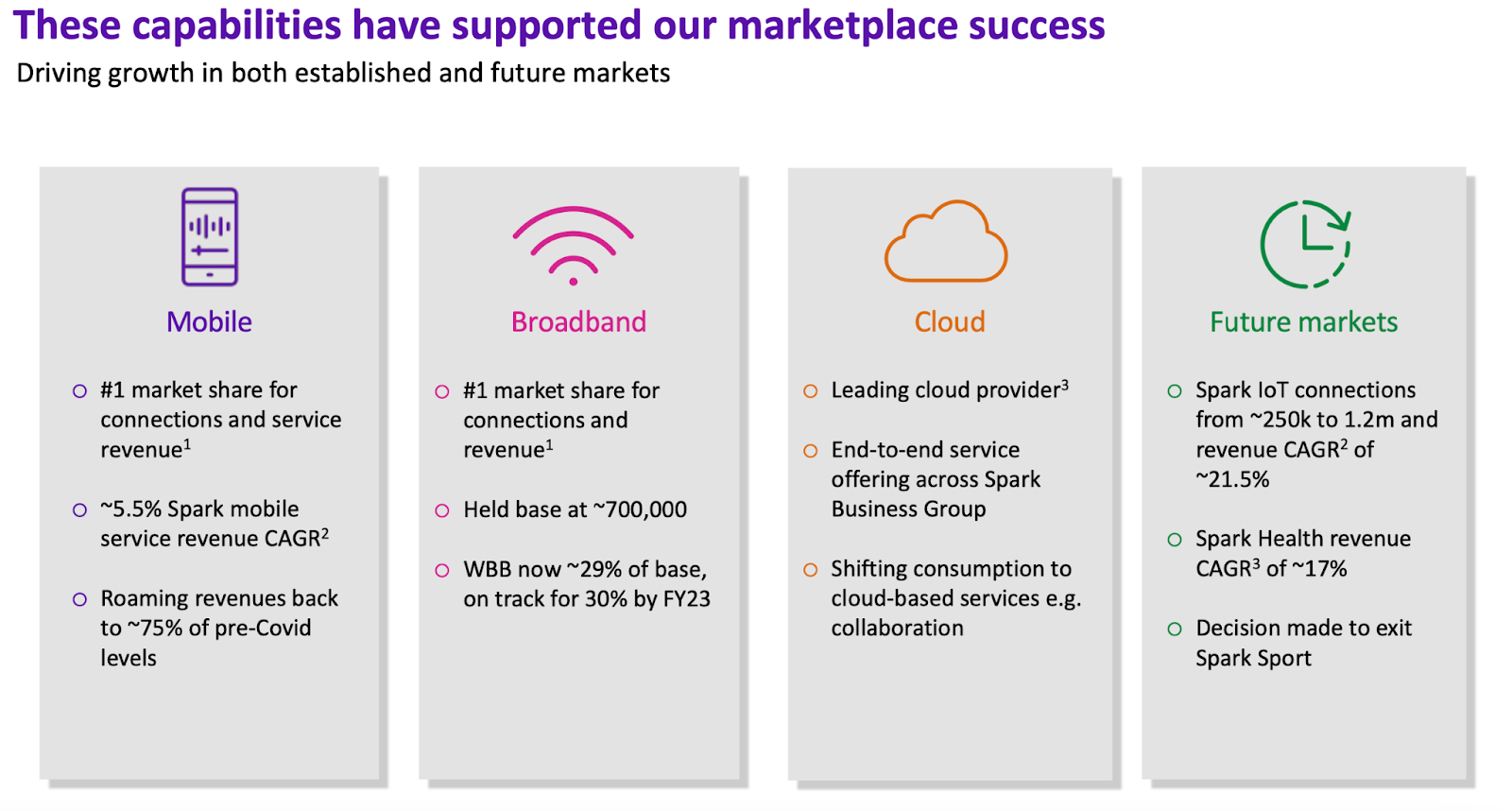

With a mobile network that reaches 98% of New Zealand’s population, Spark maintains over 2.7 million mobile connections and 687,000 broadband connections.

Spark New Zealand’s operational framework is strategically segmented to leverage its market leadership while diversifying revenue streams across consumer, enterprise, and emerging technology verticals.

The Spark Home, Mobile & Business division commands a dominant 50% share of New Zealand’s mobile market, supported by infrastructure covering 98% of the population. This segment benefits from low cyclicality due to the essential nature of connectivity services, with pricing power derived from premium offerings like unlimited 5G data plans and bundled entertainment subscriptions.

The Spark Digital unit focuses on enterprise and government clients, providing mission-critical cloud infrastructure, cybersecurity, and IoT solutions. The Spark Ventures division incubates high-growth opportunities like MATTR’s digital identity platform and satellite partnerships, ensuring exposure to next-generation technologies while mitigating reliance on traditional telecom margins.

Spark New Zealand is trading at an A$3.93 billion valuation.

Scale, Pricing Power, And Low Discretionary Exposure Are Strengths

A key operational strength lies in Spark’s (ASX: SPK) hybrid infrastructure strategy, blending owned assets with strategic partnerships to optimize capital efficiency. The company operates New Zealand’s largest data center network at 87% utilization while collaborating with Microsoft to resell Azure public cloud services, creating a seamless “connectivity-to-cloud” proposition.

This approach allows Spark to capture margin in high-value private cloud deployments while participating in hyperscaler growth without bearing full infrastructure costs.

Spark’s pricing strategy exhibits disciplined segmentation across customer cohorts. Consumer mobile plans utilize tiered pricing with perks like Spotify Premium to maintain ARPU, while enterprise clients are transitioned to value-based pricing models tied to productivity gains from cloud migration or IoT deployments.

This dual approach-defending market share in saturated consumer markets through bundling while monetizing digital transformation in enterprise segments-provides revenue stability. The company’s 5G Standalone network rollout further enhances pricing power, enabling premium charges for ultra-low-latency industrial applications and private network solutions unavailable through competitors.

Source – Spark Strategy Presentation 24-26

Operational resilience is reinforced through Spark’s agile delivery model, which replaced traditional silos with cross-functional “tribes” focused on specific customer outcomes. This structure enabled rapid deployment of cost-competitive wireless broadband plans during recent economic headwinds, capturing share from fixed-line alternatives.

The operating model’s flexibility is evidenced by the SPK-26 transformation program, which consolidated technology delivery teams, automated 40% of network operations via AI, and reduced workforce costs by NZ$80-NZ$100 million annually without service degradation.

Strategic partnerships amplify Spark’s capabilities while containing R&D expenditure. The Nokia alliance accelerates 5G Standalone deployment using shared R&D resources, while the Infosys collaboration embeds AI-driven customer experience tools across Spark’s platforms.

These partnerships enable swift adoption of global innovations tailored to local market conditions-a critical advantage given New Zealand’s unique geographic and regulatory environment.

The company’s vertical integration between infrastructure and services creates competitive moats. By combining owned fiber backhaul, data centers, and IoT platforms, Spark delivers end-to-end solutions that competitors relying on wholesale infrastructure cannot replicate economically.

This integration is particularly evident in the healthcare sector, where Spark provides HIPAA-compliant connectivity, cloud hosting for patient records, and IoT-enabled medical devices under unified SLAs-a proposition that commands 20-30% price premiums versus piecemeal solutions.

Spark’s market position is further fortified by its role as a quasi-national champion in digital infrastructure. As the primary provider of emergency communication systems and partner on smart city initiatives, the company maintains privileged access to policy discussions and infrastructure permits. This symbiotic relationship with government entities ensures Spark remains central to national digitalization agendas, providing early insight into regulatory changes and funding opportunities.

The convergence of these operational strengths-segmented market focus, hybrid infrastructure strategy, agile delivery, and strategic partnerships-positions Spark to sustain EBITDA margins above industry averages despite sector-wide ARPU pressures.

By continuously reallocating resources from legacy voice services (which declined 9.4% YoY in H1 FY25) to high-margin digital verticals, Spark demonstrates an institutional capacity for profit pool migration that underpins its premium valuation relative to pure-play telecom peers.

Slow Growth, Competitive Market Environment And Regulatory Exposure Are Weaknesses

Revenue challenges in Spark’s (ASX: SPK) core business segments represent a significant weakness, with H1 FY25 results showing an overall decline of 1.9% in revenue. Particularly concerning is the performance of the mobile segment, where aggressive price competition and subdued business sector spending have led to expectations of a total mobile service revenue decline of approximately 1% year-over-year in FY25.

This includes a largely flat performance in Consumer and SME segments, and further declines in Enterprise and Government business. The mobile segment has historically been a key growth driver for Spark, and this stagnation raises concerns about the company’s ability to maintain momentum in one of its core markets.

Competition in Spark’s core markets has intensified, with aggressive price competition noted particularly in the mobile segment. As telecommunications services become increasingly commoditized, differentiation becomes more challenging, putting pressure on margins and market share.

The ongoing migration from private cloud to public cloud has changed competitive dynamics in the IT services market, with global hyperscalers gaining market share from traditional IT service providers like Spark. These competitive pressures may limit Spark’s ability to grow revenue and maintain margins across its portfolio.

Additionally, digital disruptors focusing primarily on the customer experience layer are setting new benchmarks for digital services, requiring Spark to continuously enhance its offerings to remain competitive.

Regulatory changes and compliance requirements pose ongoing threats to Spark’s operations and profitability. As a major telecommunications provider, Spark operates in a heavily regulated environment that can impact pricing, competition, and infrastructure investment requirements. For example, Spark recently hiked prices for customers of its broadband plans citing higher operating costs and higher prices from operating partners such as Netflix.

Given New Zealand’s present economic woes, Spark’s abilities to hikes prices to respond to higher inflation or any other reasons may be limited.

Changes in privacy regulations, cybersecurity requirements, or telecommunications policy could necessitate additional investments or restrict certain business practices. Additionally, as Spark expands into new technology domains such as AI and digital identity, it may face evolving regulatory frameworks that could impact the development and deployment of these services.

Data Centres, Enterprise 5G, Asset Monetization, Value Addition And Government Digitization Are Opportunities

Source – Spark Strategy Presentation 24-26

Spark’s (ASX: SPK) data center strategy represents its most substantial near-term growth vector, with the company positioned to capitalize on New Zealand’s projected 5x increase in data center capacity by 2030.

The current development pipeline includes 118MW across three strategic Auckland sites-Takanini (10MW operational), Aotea (1MW expansion nearing completion), and North Shore (40MW planned). This infrastructure aligns with enterprise demand for hybrid cloud solutions, where Spark’s ownership of physical assets enables it to offer bundled connectivity+hosting packages that global hyperscalers cannot replicate.

Source – Spark Strategy Presentation 24-26

The 87% utilization rate across existing facilities demonstrates pricing power, while contracted long-term leases with government agencies and financial institutions provide revenue visibility. Spark’s exploration of a NZ$1B+ external investment vehicle for this segment could accelerate capacity deployment while optimizing capital structure, transforming data centers from a cost center to a profit engine.

The NZ$40-NZ$60M investment in 5G Standalone (SA) technology through FY26 unlocks premium enterprise monetization opportunities beyond conventional mobile services. By implementing network slicing capabilities, Spark can offer guaranteed service-level agreements (SLAs) for latency-sensitive applications-critical for industrial IoT in manufacturing and automated port logistics.

The partnership with Nokia provides access to global 5G SA deployment expertise, reducing R&D costs while enabling rapid commercialization of private network solutions. Early trials with maritime operators and smart city projects position Spark as the de facto provider of mission-critical 5G infrastructure, commanding 30-50% price premiums over legacy LTE solutions.

With 1.8M+ IoT connections and 26.9% revenue CAGR since FY21, Spark’s IoT division is primed to leverage New Zealand’s 13.34% projected IoT market growth through 2030. The convergence of 5G SA and edge computing enables high-value industrial deployments-predictive maintenance for dairy processing plants, real-time freight monitoring, and precision agriculture sensors.

Spark’s vertical integration (owning connectivity backbone + cloud infrastructure + analytics platforms) allows it to capture margins across the IoT value chain, unlike pure-play connectivity providers. Recent wins in smart meter deployments with energy retailers and telematics partnerships with logistics firms demonstrate ability to monetize IoT at scale.

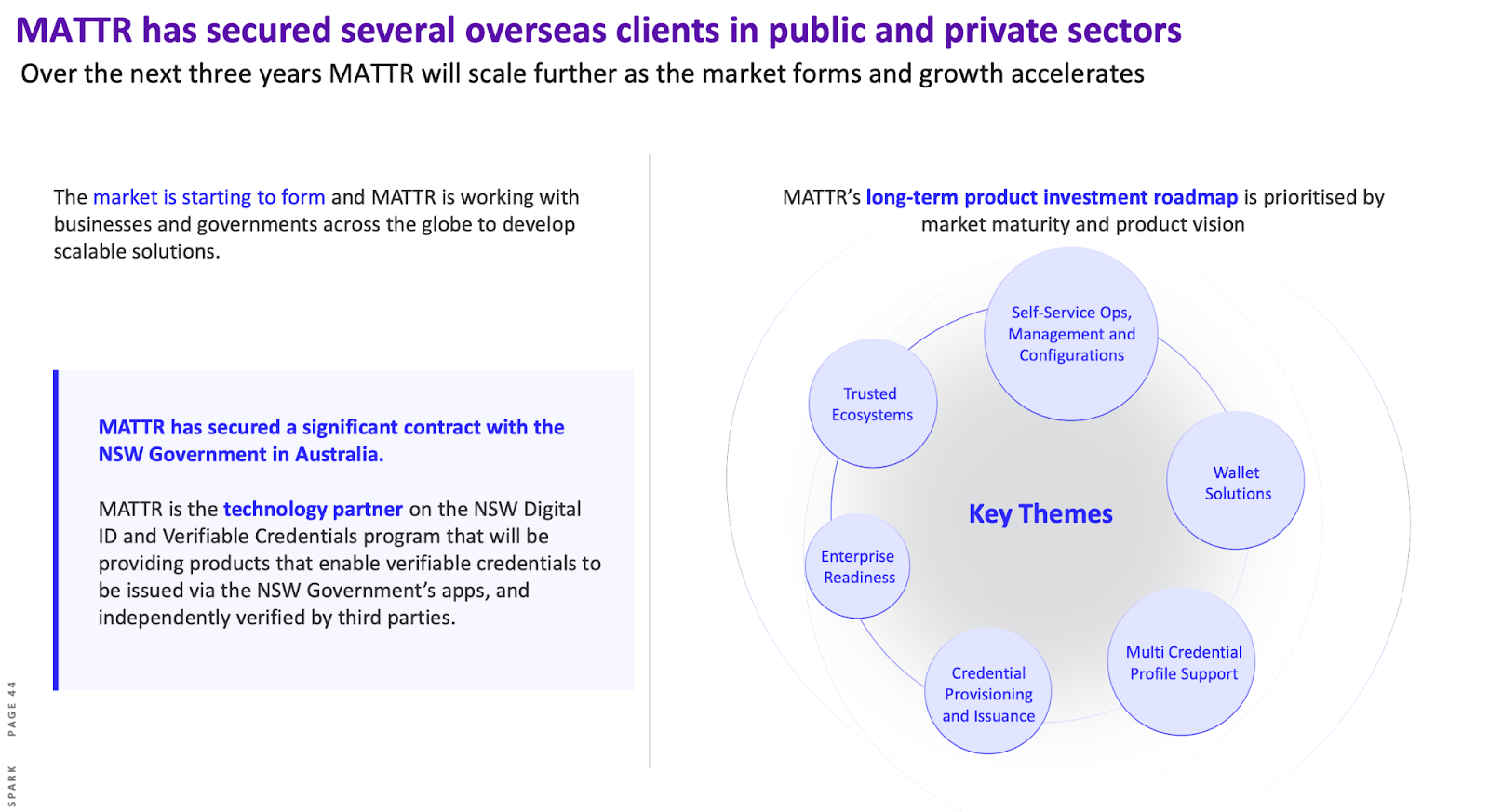

Spark’s MATTR platform sits at the nexus of regulatory tailwinds, with New Zealand’s Digital Identity Services Trust Framework creating a NZ$200M+ addressable market. MATTR’s verifiable credentials technology, already deployed for NSW Government in Australia, positions Spark as the regional leader in compliant digital ID solutions.

Source – Spark Strategy Presentation 24-26

Use cases span age verification for telco customers, professional credentialing for healthcare, and anti-money laundering (AML) checks for financial institutions. The platform’s architecture-decentralized, blockchain-adjacent-aligns with global privacy trends, enabling Spark to license the technology to ASEAN governments and multinational corporations.

Spark’s pivot to hybrid cloud solutions addresses the margin compression caused by public cloud migration, leveraging its unique combination of local data centers and Azure/GCP partnerships. The “Cloud Matrix” offering-a unified management portal for on-prem, colocation, and public cloud environments-has gained traction with regulated industries requiring data sovereignty.

Bundling this with cybersecurity services (Endpoint Detection & Response, Zero Trust Architecture) creates sticky, high-margin contracts. Recent wins include a whole-of-government cloud modernization contract valued at NZ$120M over five years, demonstrating Spark’s ability to outmaneuver global SIs through localized compliance expertise.

Despite public sector budget pressures, Spark Health is pivoting to private healthcare providers with modular SaaS solutions-telehealth platforms, EHR interoperability tools, and IoT-enabled medical device management. The division’s 12.3% revenue CAGR (FY21-FY23) provides a foundation for upselling converged solutions combining 5G, AI diagnostics, and cybersecurity.

Partnerships with medical device OEMs to embed SIMs in equipment create annuity revenue streams, while the pending launch of a health app marketplace (co-developed with insurers) targets direct-to-consumer monetization.

Spark’s tower portfolio of 6,000+ sites following the TowerCo divestment-remains a latent monetization opportunity.

The company retains rights to 20-year master lease agreements (MLAs) with favorable escalation clauses, providing cash flow stability. This infrastructure could be repurposed for edge computing nodes or small cell deployments, creating new revenue streams.

Exploratory discussions with renewable energy providers about colocating microgrids at tower sites demonstrate Spark’s asset optimization mindset, potentially converting passive infrastructure into smart energy hubs.

Macro Weakness And Saturation Are Threats

The persistent economic uncertainty in New Zealand and globally poses a significant threat to Spark’s (ASX: SPK) performance, particularly in business-oriented segments. The company has highlighted subdued business sector spending as a key factor affecting mobile service revenue and IT services.

With inflation and interest rates continuing to impact business investment decisions, there is a risk that the anticipated recovery in business spending may be delayed further than expected.

This economic environment particularly affects Spark’s Enterprise and Government division, where customers are more likely to delay or reduce technology investments in response to financial pressures.

If the challenging economic conditions persist longer than anticipated, Spark may face difficulties in achieving its growth targets and realizing the benefits of its strategic investments.

Market saturation in core segments represents a fundamental threat to Spark’s growth prospects. With mobile penetration already high in New Zealand at 70% smartphone ownership, opportunities for new customer acquisition are limited, increasing the importance of customer retention and average revenue per user growth.

Similarly, the fixed broadband market shows signs of maturity, with Spark focusing on shifting customers to higher-margin wireless broadband services rather than overall connection growth.

This saturation in core markets increases the importance of Spark’s diversification into high-tech solutions and data centers, but also heightens the risk if these growth initiatives fail to compensate for stagnation in traditional services.

Spark Financials

Spark New Zealand (ASX: SPK) demonstrated strategic financial management amid evolving market conditions from FY23 through the first half of FY25, balancing dividend commitments with investments in growth initiatives.

In FY23, the company reported adjusted NPAT of NZ$433 million, a 5.6% increase year-over-year, driven by mobile service revenue growth of 9% and disciplined cost control. This performance supported a total dividend of 27 cents per share, up 2 cents from FY22, reflecting confidence in free cash flow generation and a 90% payout ratio.

The dividend increase marked Spark’s first since 2016, funded by earnings growth and the partial return of NZ$146 million from TowerCo divestiture proceeds through share buybacks.

FY24 saw heightened macroeconomic pressures, with reported NPAT declining 72.2% to NZ$316 million due to booking of the TowerCo gain and Spark Sport exit in FY23. Adjusted for these one-offs, NPAT declined moderately, impacted by lower IT services demand and competitive pricing in business mobile.

Despite a 1.2% drop in adjusted revenue to NZ$3.86 billion and a 2.5% EBITDA decline to NZ$1.16 billion, Spark maintained its total dividend at 27.5 cents per share. The payout ratio rose to 95%, signaling management’s commitment to shareholder returns even as earnings softened. This decision reflected Spark’s resilient cash flows from core connectivity services and prudent capital allocation, including reduced capex to NZ$415–435 million.

The first half of FY25 revealed intensified challenges, with reported NPAT collapsing 77.7% year-over-year to NZ$35 million (adjusted NPAT: NZ$56 million), driven by a 15.5% EBITDA decline to NZ$448 million. Mobile service revenue fell 3.7%, particularly in enterprise fleets (-17.7%), while IT services faced margin compression from cloud migration trends.

Part of the NPAT decline (NZ$29 million) was due to higher depreciation and amortization costs stemming from the company’s operating model transformation and cost cutting investments in IT/AI.

The telco reduced its FY25 earnings guidance from between NZ$1.12 billion (NZ$1.01 billion) and NZ$1.18 billion, to a range of NZ$1.04 billion and NZ$1.1 billion.

Despite these headwinds, Spark declared an interim dividend of 12.5 cents per share, down 1 cent from H1 FY24, with total FY25 guidance reduced to 25 cents per share. The dividend cut aligned with lower earnings and prioritized funding for strategic initiatives like 5G Standalone and data center expansions, while maintaining a sustainable payout ratio.

Free cash flow improved 67% to NZ$77 million in H1 due to capex discipline and working capital management, providing flexibility to navigate near-term pressures.

The significantly expanded SPK-26 Operate Programme represents a comprehensive approach to transforming Spark’s cost base, with expected net labor and opex reduction of NZ$80-100 million in FY25, with NZ$29 million already reported in the H1 FY25 results.

This increases to NZ$90-NZ$110 million on an annualized basis by the end of the financial year, with additional benefits of NZ$20-NZ$30 million anticipated from FY26-FY27. By FY27, the program is forecast to deliver NZ$110-NZ$140 million in annualized benefits.

Spark’s dividend policy shifted strategically across this period. The FY23 increase to 27 cents reflected post-pandemic recovery in roaming revenue and TowerCo divestiture proceeds, enabling higher shareholder returns.

In FY24, maintaining the dividend at 27.5 cents despite earnings pressure demonstrated management’s confidence in long-term cash flow stability, though it strained the payout ratio.

By 1H25, the reduction to 25 cents annually acknowledged persistent macroeconomic uncertainty, with management rebalancing shareholder returns against the need to fund NZ$1B+ data center investments and SPK-26 cost transformation programs.

This phased approach underscores Spark’s adaptive capital management, prioritizing structural reforms and growth investments while sustaining moderate dividends through cyclical downturns.

Spark is currently trading at historically low multiples individually and against peers in terms of forward P/E, EV/EBITDA, P/B, and P/S ratios.

Source – Reuters

Spark is currently trading at a dividend yield of 11.8% on a trailing twelve month basis. Investors should expect 5%-7% yield in the short term to reflect possible reduction in dividends as the company focuses on streamlining operations and funding new investments.

However, the combination of stock re-rating in the medium term and possible growth in dividends off a low cost base present investors a serious opportunity with low risk.

Conclusion

Spark (ASX: SPK) is a non-discretionary infrastructure essential in one of the most developed economies in the APAC region with solid market positioning and pricing power which is available at a historic discount to peers due to a slowdown in the New Zealand economy.

The company has put in place a cost reduction strategy to streamline operations, lower operating costs and resume a growth trajectory which is already showing results as expected.

Spark has direct long-term exposure to ever growing digital consumption and is a indirect proxy to evolving megatrends such as AI, evolving forms of media such as gaming and VR, IoT, modernization of government, telemedicine, remote surgery, etc.

The current economic lull in New Zealand will not have long-lasting impacts on Spark’s stock as the company is an essential service provider and the stock has already priced in the worst. As the economy recovers, lower rates and a return to consumption should put Spark back on a growth trajectory.

The stock has just begun an upward trajectory after a very steep fall and offers investors a solid long-term play at a reasonable price along with a solid dividend yield.