Today, we will look at why we like City Chic shares (ASX:CCX) and give our views on our CCX share price forecast.

City Chic is a leading plus-size women’s clothing retailer with 801,000 active customers.

We first looked at City Chic back in mid-September 2019 when the CCX share price was trading at around $2.10.

Since then, the CCX share price has rallied over 80% to its current share price of $3.80 at the time of writing.

The company has been going from strength to strength in its business strategy.

City Chic’s focus on an omnichannel model with a heavy focus on online retailing has helped it thrive during the COVID pandemic.

The company has also made a number of great acquisitions, taking advantage of distressed assets due to the pandemic.

In addition, CCX is rapidly growing its footprint in the US and UK which has helped the company achieve 31% revenue growth in FY20.

Table of Contents

City Chic (ASX:CCX) is a global omnichannel retailer with a market cap of $890m, specialising in plus-size women’s clothing, footwear, and accessories.

The company was originally a brand under the Speciality Fashion Group but rebranded as City Chic in November 2018. Subsequently, the company divested from non-plus size clothing brands such as Rivers and Katies.

CCX currently has six brands:

- City Chic

- Avenue

- Hips and & Curves

- Fox & Royal

- CCX (Activewear)

- Evans

The company’s brands offer a variety of products including casual, intimate, and conservative wear, and are targeted towards the 18-55 age group.

Sales Channels

CCX utilizes various sales channels to deliver its products to its customers.

The City Chic online website is the channel that contributes the most to FY20 revenue at 61%.

Physical stores are also maintained in Australia and New Zealand only which contributed 31% to revenue.

The company also utilizes wholesale channels (4% of revenue) where it sells its products to partners such as Macy’s and Nordstrom who then fulfil the sale once it’s made.

Online marketplaces (4%) such as Amazon and ASOS are also used where the company feeds the product via the partners’ platform but City Chic owns the product and fulfils the order.

Source: CCX Annual Reports, MF & Co. Asset Management

Geographical Presence

The company has a presence and generates revenue from the Northern hemisphere consisting of the US, UK, and Europe and the Southern hemisphere made up of Australia and New Zealand.

Source: CCX Annual Reports, MF & Co. Asset Management

The significant increase in Northern hemisphere sales can be attributed to the acquisition of Avenue in the US.

CCX only has a store presence in Australia and New Zealand, its sales in the US, UK, and Europe are made through its websites plus the wholesale and online marketplace channels.

City Chic (ASX:CCX) Business Strategy

Omnichannel Strategy

CCX implements an omnichannel strategy where it leverages its online and store presence to deliver an enhanced customer experience.

The company is utilizing macro trends to its advantage by relatively concentrating its focus on its online business.

This is reflected in its increased investment in and acquisition of e-commerce assets while simultaneously reducing its physical store presence from 107 (H1’19) to 93 (H1’20).

While the company has closed down 30 of its stores that are loss-making since mid-2018, it has only opened 16 new stores in areas where it’s economically viable.

The company maintains physical stores because it’s integral to the holistic execution of its omnichannel strategy.

US and UK Expansion

Core to the company’s business strategy is its expansion into the US and the UK markets.

This was evidenced by the acquisition of Avenue in H1’20 and Evans in H1’21.

Both newly acquired assets only operate online and do not have a physical store presence.

CCX is aiming to make more strategic acquisitions and to enlist more channel partners in both these markets to drive sales and revenue in these markets where sizable growth potential lies.

Industry Analysis

Macro Environment and Trends

As vaccine rollouts in various developed markets gain traction and a post COVID-19 era approaches, consumer discretionary spending is expected to recover gradually as consumer confidence improves.

The Global E-Commerce fashion market is also expected to recover and grow at 11.48% CAGR to $673 billion by 2023.

According to Allied Market Research, the Global Plus size clothing market is expected to grow to $696.71 billion by 2027 from $480 billion in 2019 indicating a CAGR of 5.9%.

Growth in demand is driven by trends in body positivity and a growing overweight global population.

The above macro trends suggest a recovery in spending in the plus-size apparel segment that CCX is positioned to benefit and grow its revenue.

Competitive Landscape

The plus-size clothing market is fairly saturated with numerous brands such as Forever 21+, Taking Shape, and H&M that have limited differentiation.

Because the market has a number of participants with not a few leading brands, the pricing power held by each brand is not significant.

As a result, CCX and other plus-size brands compete on the basis of the price by offering lower prices on products and price discounts to drive sales.

City Chic (ASX:CCX) Financial Overview

Financial Performance

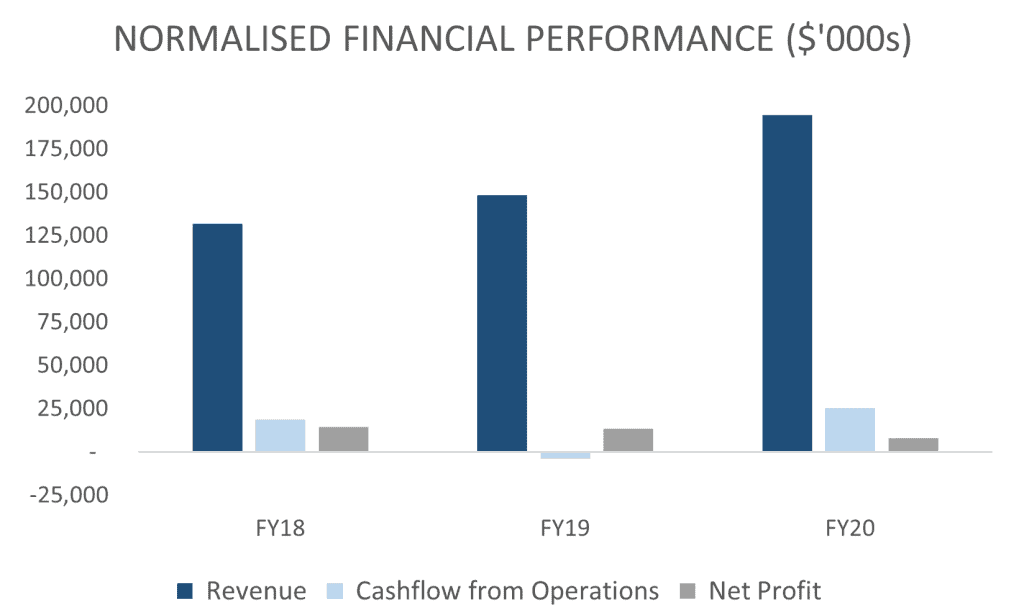

In FY20, City Chic shares’ revenue from core operations grew 31% from $148m to $194m mainly driven by the acquisition of Avenue and growth in online sales.

The gross profit margin declined from 58% to 48% YoY which was also reflected in the net profit margins which also declined YoY from 9% to 4%.

Weakening profit margins are mainly attributed to the change in product mix to include lower-priced, lower-margin products.

Declining margins were also due to the offering of price discounts on products to drive sales due to the onset of the COVID-19 pandemic.

Source: CCX Annual Reports, MF & Co. Asset Management

City Chic shares are also cash-flow positive having received net cash from operations of $31m in the trailing 12 months versus $20m in the previous corresponding period.

Relevant metrics of operational efficiency such as inventory turnover and both trade payables and receivables outstanding days remained constant from FY18 to FY20.

Financial Position

City Chic shares have $83m in cash and $23m in total debt all representing lease liabilities.

The company raised $111.1m to finance acquisitions and funding other expansionary expenditures in the US, UK, and Europe.

City Chic (ASX:CCX) Investment Case

Sustained Capitalization of Online Sales Growth Opportunities

Since the restructuring, City Chic has embraced the digital transformation in its business model.

This is evidenced through increased investment in eCommerce and IT assets in addition to offering 3.5x more products online than available in stores.

A targeted focus on growing its online business has contributed to the company’s resilience and has future-proofed its business model.

Online penetration has also increased from 40% to 65% indicating that an increasing number of active customers are shopping from the company’s online channels.

Source: CCX Half Year Reports, MF & Co. Asset Management

The accelerated adoption of online shopping due to the pandemic provides a tailwind for online sales to grow further.

Distinct Omnichannel Strategy

CCX use of an omnichannel strategy is strategically aimed at generating the most value from customers.

Omnichannel customers are proven to be more valuable according to the Harvard Business Review, evidenced through average spending of 4% more in-store and 10% online on every shopping occasion relative to single-channel customers.

According to Mckinsey Industry forecasts, 100% of growth in the US apparel market will originate from omnichannel sales by 2023.

CCX is capitalizing on this trend and is anticipated to contribute to top-line revenue growth in the medium to long term.

Value Adding Strategic Acquisitions

City Chic (ASX:CCX) has taken advantage of the increasing number of bankruptcies due to the pandemic to make strategic acquisitions for its brand and eCommerce portfolio.

Avenue significantly contributed to the top line. Avenue, which CCX acquired for $25m in Oct 2019 contributed $48m to total revenue in the following months to June 2020.

CCX acquired Evans on 21 Dec 2020 for $41m and prior to Evan’s parent company Arcadia Group entering administration, Evans’ eCommerce business generated $46m in revenue in the trailing 12 months.

Commencement of revenue contribution from Evans to the company’s revenue is thus expected to be a potential catalyst.

Continued Investment in Online Business Strategy

CCX continues to invest in enriching customer experiences online through the launch of a new global integrated eCommerce platform.

This was also evidenced by the launch of a new Customer Relationship platform to gain further customer insights and utilize predictive modelling.

Investment in the website and other digital assets has increased 21x from $0.1 in FY18 to $2.1m in FY20 with IT investment now representing 41% of total Capex compared to 3% in FY18.

This indicates conviction in developing the digital revenue-generating aspects of its business.

City Chic (ASX:CCX) Risks

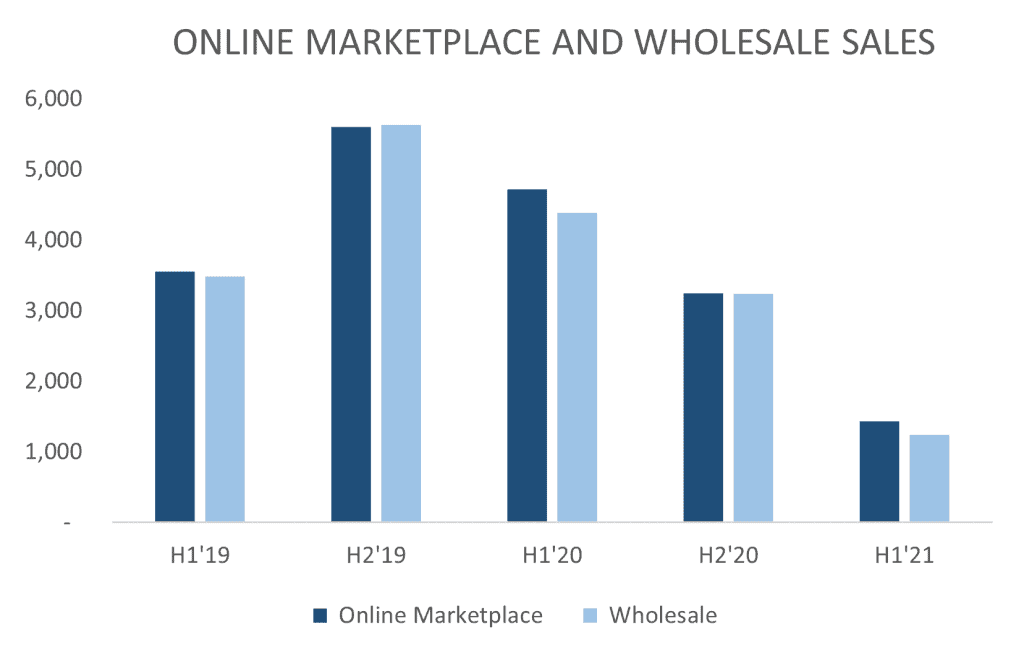

Declining Revenue Contribution from Partnerships

Total revenue generated from Online marketplace and Wholesale partnerships with retailers such as Amazon and Macy’s respectively have declined by 76% from $11.2m in H1’19 to $2.7m in H1’21.

This was mainly driven by business disruptions to partners especially brick and mortar wholesale partners in the US and UK which were mandated to temporarily close due to the pandemic.

Source: CCX Half Year Reports, MF & Co. Asset Management

The decline can also be explained by the shift of customers from the company’s partners to shopping from new brands acquired by CCX such as Avenue hence indicating cannibalisation of sales.

The company is however currently focused on actively pursuing additional partnerships in Europe and the US in order to revitalize and this declining segment.

Limited Product Differentiation

CCX’s products are not significantly differentiated from competing products and target consumers make purchase decisions based on price.

As a result, CCX has to offer price discounts regularly in order to drive/maintain revenue and remain competitive.

This adversely affects the company’s profit margins and is thus expected to exert downward pressure on the company’s financials if price discounts continue to be offered.

City Chic (ASX:CCX) Peer Analysis

Peer companies were selected on the basis that they had a substantial amount of sales in the US and/or Australia.

Peers selected also sold mid to highly-priced apparel as the main business activity similar to CCX in addition to generating a significant level of sales through online channels.

Source: Bloomberg, MF & Co. Asset Management

City Chic shares at the current CCX share price appears fairly valued when compared to peers.

Even though at the current CCX share price the forward P/E is quite high, a significantly above median growth rate in forwarding revenue justifies its higher multiples.

Conclusion

With its restructuring, CCX is integrating general trends into its business model and strategy which is a strong strategic move by the management team.

The company aims to grow sales through acquisitions of attractive businesses, further development of its online sales channel and focus on partnerships.

This is aimed at expanding the company’s footprint in large markets such as the US and UK which provide strong potential for revenue and earnings growth.

While no significant macro trends or tailwinds exist in the short term, City Chic’s business model is best positioned to perform resiliently in the medium to long term.

This should translate to strong potential upside for the CCX share price.