A rules-based quantitative approach to global equity markets. Built to compound across cycles, not chase them.

Results on this page are updated periodically as the strategy runs forward. Last updated: 24 July 2026.

Important risk information

The performance shown on this page is hypothetical. The 2018 to 2024 record is a backtest and the 2025 to June 2026 record is a frozen-rules forward out-of-sample simulation, not the result of actual trading, and past performance is not a reliable indicator of future performance. The strategy trades two- and three-times leveraged ETFs, which are high-risk, can move sharply, and can decay in volatile or sideways markets, so you could lose a substantial part, or all, of the capital you invest. This is general advice only and does not take into account your objectives, financial situation or needs. Consider whether it is right for you, read our Financial Services Guide, and seek personal advice if you are unsure. Full disclosures are set out at the bottom of this page.

MFAM's Quantitative Leveraged ETF Strategy is a fully rules-based trading system combining three complementary quantitative engines, trend-following on the long side, mean reversion, and trend-following on the short side, across a basket of leveraged US and Chinese equity ETFs. In plainer terms, one engine rides rising markets, one buys sharp dips for the bounce back, and one makes money when markets fall. All three run at the same time, and the rules lean on whichever engine suits what the market is doing. Every entry, exit, and position size is driven by mathematical rules. There is no discretionary override.

Built on the concepts taught in our free trading course

The trend-following, mean-reversion, volatility-adjusted stops and regime-filter frameworks that drive this strategy are the same concepts taught step by step in the MFAM free trading course. If you want to understand how and why this system works, the course walks through the underlying mechanics in plain language. Access the free trading course here.

The short version

- 57.2 per cent annualised return versus 14.9 per cent for the S&P 500, January 2018 to June 2026, all results net of an all-in 30 basis-point per-fill charge that bundles MFAM commissions, broker fees and execution slippage. No separate management or performance fee.

- Maximum drawdown -24.1 per cent versus -33.7 per cent for the benchmark. Higher return at lower drawdown is the alpha signature of the strategy.

- Calmar ratio 2.38 versus 0.44 for SPY. Roughly five times the return per unit of worst-case drawdown.

- A diversified basket of leveraged ETFs across three engines, trend-following on the long side, mean-reversion, and trend-following on the short side. The engines rotate leadership across regimes so the strategy is rarely flat across all three at once and rarely fully exposed across all three at once.

- Cash account at Interactive Brokers, no broker margin. The investor holds custody of their own account. MFAM never holds investor funds.

- Non-discretionary general advice. Every trade signal requires the investor's explicit yes before the MFAM adviser places the order.

- Minimum investment AUD 20,000.

The full detail — methodology, the alpha-versus-beta split, engine design, the drawdown framework, the curve-fitting tests and the access mechanics — is set out in the sections below.

Historical Performance

The strategy was built and tuned in-sample on market data from 2018 through 2024. The 2025 to June 2026 period was held out as a forward out-of-sample test, run on the same rules with every parameter frozen, so it reflects data the system never saw during the build. Over the in-sample window the strategy compounded at 57.7 per cent a year. Its worst fall from a peak along the way, the maximum drawdown, was -24.1 per cent. Dividing the annual return by that worst fall gives a Calmar ratio of 2.40. For scale, a passive S&P 500 investment over the window shown on this page scores 0.44 on the same measure, so the strategy earned roughly five times as much return for every unit of worst-case loss. Over the out-of-sample window it compounded at 53.6 per cent a year at a -21.5 per cent maximum drawdown, a Calmar of 2.49, close to the in-sample figure. That 53.6 per cent is annualised from the daily equity curve over the eighteen months from the last close of 2024 to 30 June 2026, so the calendar-year bars further down the page, where 2026 is only a half year, will not reproduce it exactly. The edge holding up on unseen out-of-sample data is the central check that it is real rather than curve-fit. Across the combined 2018 to June 2026 period the equity curve has meaningfully outpaced a passive S&P 500 investment.

Returns shown are already net of strategy fees

Every figure on this page — the +4,500% total return, the 57.2% CAGR, the equity curve, the per-year results, the parameter sweeps, all of it — is calculated net of an all-in 30 basis-point per-fill charge applied to every entry and every exit. The 30 bps is the actual per-fill figure, not a conservative placeholder. It bundles the MFAM management commission, broker commissions, bid-ask spread, and realistic execution slippage on the underlying leveraged ETFs into a single number. There is no separate management fee, performance fee, or platform fee layered on top of the figures shown. Exchange and regulatory pass-through fees, which a broker always charges on top of commissions, sit outside this 30 bps figure, as does tax, which depends on the investor's individual circumstances. The headline performance is materially above the S&P 500 with this real per-trade drag already applied to every fill in the calculation.

The strategy outperformed the benchmark in all 9 calendar years from 2018 through 2026 year to date, beating it by a wide margin in most of them. The narrowest gap so far is 2026 year to date, at 14.0 per cent for the strategy against 11.2 per cent for the S&P 500, a year that included the 2025 to 2026 drawdown covered further down the page. The margin varies year to year because the system is built to capture large directional moves rather than to track the benchmark closely.

Context for this period

Long-run S&P 500 returns sit somewhere in the 7 to 10 per cent range depending on the period measured, averaging around 10 per cent in nominal terms over the past century. That average is made up of decades that look very different from each other, including the 1929-32 crash, the 1968-82 stagflation decade, the 2000-02 dot-com bust and the 2008 global financial crisis.

The January 2018 to June 2026 window has not looked like those decades. It has instead been one of the strongest stretches the benchmark has ever had, with a 14.9 per cent annualised return driven by uninterrupted tech-led leadership, fast recoveries from the 2020 COVID shock and the 2022 inflation shock, and an artificial-intelligence-driven capex cycle from 2023 onward. The benchmark is running well above its long-run average and sets a high bar.

The strategy outperformed that elevated benchmark by a meaningful margin in almost every year of the window. Historically, the strategy's edge has been largest in years with strong directional moves in either direction, including the 2019 tech-led bull run, the 2021 reopening, the 2024 AI-led extension, and notably 2022, where the trend-short engine and mean-reversion engine kept the strategy's own drawdown well contained through a year that took the S&P 500 down 18 per cent. The tightest year so far is 2026 year to date, where the strategy is ahead 14.0 per cent to 11.2 per cent after trading through the 2025 to 2026 drawdown covered in the drawdown-events section below. The structural edge has historically been most visible against cooler benchmarks closer to the 7 to 10 per cent long-run average than against the far stronger backdrop of the past eight years.

No guarantee is made about future performance. The point is that the strategy has beaten a very hot benchmark. A cooler benchmark is historically where this type of system has had its best relative years.

To step through the mechanics, the paperwork to open the Interactive Brokers account, and whether the strategy is a fit for your portfolio, book a callback with an MFAM adviser. The administrative side of running the strategy, including custody, signal delivery and adviser execution, is set out in How You Access the Strategy at the bottom of this page.

Request a CallbackPrefer to learn the fundamentals first? Access the free trading course.

Alpha vs Beta

The first number most investors look at is return. A 57.2 per cent annualised strategy looks objectively better than a 14.9 per cent benchmark. The raw comparison hides something important though, because not all returns are created equal. A strategy's return number has to be broken down into two very different components before it can be judged honestly.

Beta is market exposure

Beta is the portion of a strategy's return that comes from simply being in the market. If the S&P 500 goes up 10 per cent in a year, a fully invested portfolio that moves in lockstep with it will also go up roughly 10 per cent. Nothing clever happened. The market rose, and the investor was along for the ride. Anyone willing to press a single buy button on an index ETF can collect beta. It requires no analysis, no timing, and no discipline.

Critically, beta is not free. It comes with full participation in market losses. The same passive portfolio that captured the upside will sit through the full drawdown when the market falls. The investor has no defence against a bear market. They accept whatever path the market delivers, peaks and troughs alike.

Alpha is return that does not come from market exposure

Alpha is what is left over after the beta portion has been accounted for. It is the portion of return that reflects a genuine edge, whether from timing, selection, risk management, or all three. Alpha is what separates an active strategy from a passive one. When a strategy delivers return that cannot be explained by market exposure alone, and delivers it with risk characteristics that are measurably different from a passive market allocation, that is alpha.

The distinction matters because alpha and beta are valued very differently. Beta is effectively free, available for a fraction of a per cent in management fees through any index ETF. Alpha is scarce, because it requires a source of edge that most market participants do not have. Decades of academic and industry research confirm that consistent alpha is rare, and strategies that can demonstrate it are treated as materially different from strategies that simply ride the market higher.

How this strategy generates alpha

This strategy's outperformance versus the S&P 500 is not a function of taking more market risk. The opposite is true. Over the January 2018 to June 2026 window it produced a 57.2 per cent annualised return against 14.9 per cent for the S&P 500, while simultaneously containing its maximum drawdown to 24.1 per cent versus 33.7 per cent for the benchmark. Higher return and lower drawdown at the same time. That combination cannot be produced through beta alone. More market exposure would have produced deeper drawdowns, not shallower ones.

The strategy uses rules to pull capital out of the market when conditions no longer support its trading signals, and to deploy capital more aggressively when conditions do. A passive buy-and-hold investor has no mechanism to do either. They are always fully exposed regardless of whether the environment is favourable. The strategy's alpha comes from this selective exposure, applied mechanically by the rules rather than discretionarily by a human. The risk-adjusted metrics in the next section are where this alpha becomes visible, and the regime filter that drives the selective exposure is explained further down the page.

Risk-Adjusted Return Profile

Raw return alone understates the quality of the strategy. The cleanest way to judge a leveraged trading system is to compare its return per unit of worst-case drawdown taken to get there.

The Calmar ratio is the headline metric for this type of system. It divides the annualised return by the worst peak-to-trough drawdown across the period, which captures the question every leveraged-ETF investor should be asking, namely how much return was extracted for each unit of drawdown actually experienced. The strategy's Calmar of 2.38 is roughly five times the S&P 500's 0.44 over the same window. Headline CAGR is 57.2 per cent versus 14.9 per cent, and despite trading two- and three-times leveraged instruments the strategy's worst drawdown was -24.1 per cent against -33.7 per cent for the benchmark. The drawdown containment is what makes the higher CAGR meaningful, because a leveraged strategy that produced the same return through deeper drawdowns would not be the same product.

Sharpe and Sortino ratios are not the load-bearing metrics for this kind of system. Both measure variance around the mean, and a leveraged-ETF strategy is engineered to produce large positive moves on the days the underlying setups fire. Those large moves are exactly what the strategy exists to capture, and ratios that penalise them on a daily basis understate the quality of an outcome that is best judged on a peak-to-trough basis. The strategy's Sharpe ratio over the period was 1.99 and its Sortino was 2.91, both shown alongside Calmar in the chart above, but the headline question for a strategy of this design is whether the return justifies the worst drawdown taken, which is what the Calmar plus the drawdown chart together describe.

The mechanical source of the alpha is an intentional reduction in market exposure during adverse regimes, combined with an opportunistic short-side engine that profits when the long side is in cash. That regime-shifted exposure is what produces a higher return at a shallower drawdown, and is covered in the engine and regime filter sections below.

Why Maximum Drawdown Is the Number That Actually Matters

Most investors focus on return. Experienced investors focus on drawdown, because the arithmetic of recovery is unforgiving. A loss and a subsequent gain of the same percentage do not cancel out. The deeper the drawdown, the more disproportionate the recovery required.

A 50% drawdown requires a 100% gain to break even, which at historical equity market return rates takes roughly seven years. A 75% drawdown requires a fourfold return and realistically may never be recovered within an investor's remaining time horizon. Drawdown is not just a number on a chart. It is a direct tax on future compounding, and in severe cases it ends the compounding journey entirely.

The gap between the strategy's -24.1% maximum drawdown and the S&P 500's -33.7% is meaningful in its own right, but the relevant comparison is not the headline drawdown number alone. The strategy delivered a 57.2 per cent annualised return for that drawdown, against a 14.9 per cent return for a benchmark that took a deeper drawdown to get there. Per unit of worst-case drawdown experienced, the strategy compounded capital roughly five times faster. The Calmar ratio is the formal expression of that, and it is the metric that matters most for a leveraged-ETF system because it answers the question every drawdown-aware investor is asking, namely how much return was actually extracted for each unit of pain endured.

This is also why any strategy quoting strong headline returns should be scrutinised for the path it took to get there. Large returns achieved through large drawdowns are statistically fragile. The strategy here is engineered to contain the left tail first and let returns compound as a consequence, rather than the other way around.

Plotted continuously, the strategy's drawdown profile sits above the S&P 500's through most of the period. The worst trough was -24.1% versus -33.7% for the benchmark, and recovery back to new highs tends to happen faster. The 2020 COVID shock and the 2022 bear market are both visibly shallower and shorter for the strategy, which is the regime filter cutting exposure during adverse periods, and the trend-short engine taking over when long-side conditions deteriorate.

Historical Drawdown Events in Context

A feature of a leveraged-ETF strategy worth understanding is that its largest drawdowns tend to follow its largest rallies. The two- and three-times leveraged instruments produce outsized spikes during favourable regimes, and any subsequent consolidation is measured against that spike. The headline drawdown number reflects how much of a prior rally was given back, not how much base capital was put at risk.

A second, structural driver of these events is the trend engines' own design. Trend-following systems, on either the long or short side, are built to capture the bulk of a sustained move, not to exit at the top. The exit signal requires confirmation that the trend has weakened, which by construction occurs after the peak rather than at it. That confirmation requirement is precisely what allows the system to ride extended trends without being shaken out by mid-trend pullbacks. The cost of that patience is that a portion of the final leg of every trend is given back before the exit fires. This giving-back is not the strategy failing. It is the engine behaving exactly as designed, accepting a few percentage points of peak-to-exit slippage in exchange for the ability to hold winning positions through long, profitable runs. A trend system optimised to avoid give-back would also exit much earlier in its winners, sacrificing the tail of outlier returns that the long-tail distribution depends on.

Across January 2018 through June 2026 the strategy has experienced five peak-to-trough drawdowns of 15% or more. Three of those exceeded 20%: the 2018 sell-off at -24.1%, which is the all-time maximum, the 2019 growth scare at -20.3%, and the 2025 to 2026 sell-off at -21.5%. The 2020 COVID crash was held to -19% and the 2024 chop to -18%. In account-value terms every trough has formed higher than the one before it, a higher-lows pattern visible as the rising trough levels on the chart, while the depth of each fall has stayed inside a tight -18% to -24% band rather than running away to deeper levels, which is the clearest evidence the risk-control framework has held its ground as the record has grown. Worth noting, the 2022 rate-hike bear market that dominates the S&P 500's own drawdown history over this window only cost the strategy about -14.6%, below the 15% threshold used for this chart, because the regime filter and the trend-short engine were already cutting long exposure and adding short exposure well before the benchmark troughed. It is not marked as a separate event here. Each red band on the chart marks one of the five events, labelled with its peak-to-trough depth and with how much higher that trough sat, in account-value terms, than the one before it.

Each event follows the same pattern. A sustained rally produces a new all-time high, the underlying ETFs reach a regime inflection, and the strategy gives back a portion of the unrealised gain before the regime filter, the volatility-adjusted stops or the trend-short engine cut net exposure. Each drawdown is substantial in peak-to-trough terms, but the magnitudes have clustered inside a tight -18% to -24% band across the whole record rather than running away to deeper levels. That boundedness, not the absence of drawdowns, is the signature of a working risk-control framework.

- 2018 sell-off (-24.1%), the all-time MDD. The February 2018 volatility spike and the Q4 2018 equity drawdown rolled into one extended event lasting roughly thirteen months. Volatility-adjusted stops exited long positions through each leg as realised vol expanded, and this remains the deepest drawdown in the strategy's record.

- 2019 (-20.3%). The second time the strategy breached the 20% mark. The mid-2019 trade-war escalation and the yield-curve-inversion growth scare produced the kind of sharp, sentiment-driven whipsaw the trend engines are most exposed to before a regime shift is confirmed.

- 2020 COVID crash (-19%). An extremely rapid, largely indiscriminate sell-off across global equities in the first quarter of 2020, with the trough reached in a matter of weeks. Despite the speed of the move, the volatility-adjusted stops and the trend-short engine held this episode to -19%.

- 2024 chop (-18%). A persistent rotation between mega-cap leadership and broader-market participation through US election year. The directional engines whipsawed before the trend-short engine and mean-reversion engine stabilised the book, and the trough still sat above every prior trough since 2019.

- 2025 to 2026 sell-off (-21.5%). A two-stage sell-off driven by escalating Iran and Middle East conflict, renewed tariff and policy uncertainty, and a sharp momentum unwind in early 2026. The third event to exceed 20% and the deepest since 2018, though still within the strategy's historical drawdown range. It troughed in May 2026 and the book has since recovered toward new highs.

The honest caveat

An investor whose capital enters right at a peak experiences the full peak-to-trough drawdown because their starting NLV is that peak. The compounding visible across the eight-year curve is a product of staying invested through multiple cycles, not of how the strategy behaves in any individual event. Anyone deploying capital into the strategy should size their exposure against the ability to tolerate a drawdown of around 25 per cent from the day they enter, which is the range the strategy has historically operated within. As the Monte Carlo stress test further down the page shows, an unluckier ordering of the same trades could fall further, into the high-30s to low-40s per cent, and exposure should be sized to withstand that too.

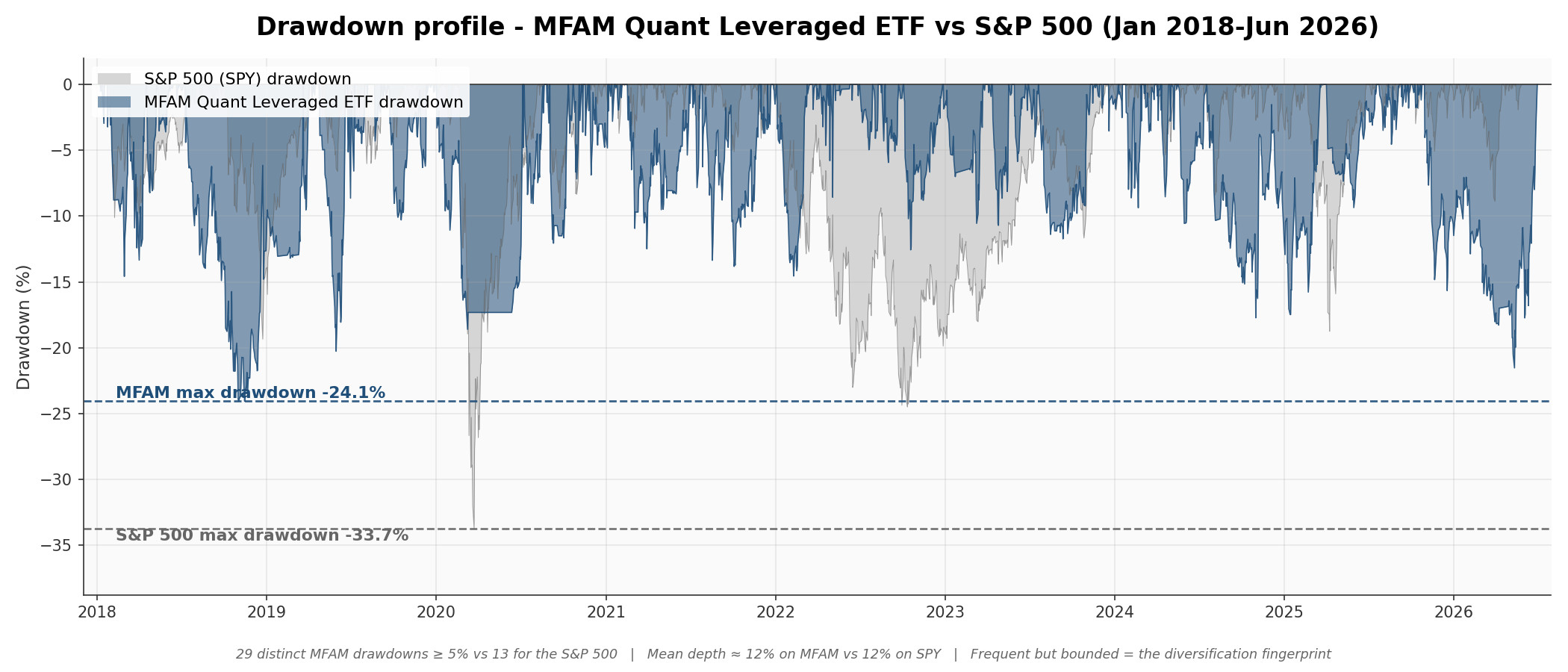

Frequent but Bounded, the Diversification Fingerprint

If the maximum drawdown number tells you how deep the worst event was, the drawdown profile tells you how the strategy actually feels to live with day to day. The picture below plots the strategy's drawdown against the S&P 500 over the same eight-year window.

Two things stand out. First, the strategy is in some kind of drawdown almost nine days out of every ten. There are twenty-nine distinct drawdown events of five per cent or deeper across the window, against thirteen for the S&P 500. Second, despite that frequency, the deepest drawdown is shallower than the S&P's: -24.1 per cent versus -33.7 per cent.

That combination is the diversification fingerprint of the strategy. A diversified basket of leveraged instruments running across three engines means new local peaks are reached constantly, which means small recedes from those peaks happen constantly. The strategy is almost never sitting on an all-time high. But the same diversification means no single engine's bad month has so far dragged the whole book far past its historical -18% to -24% range. The drawdowns are frequent, and have so far stayed bounded, though a deeper fall cannot be ruled out, as the Monte Carlo stress test below makes clear.

This profile has a side-effect on the headline statistics. The strategy's Sharpe ratio of 1.99 is good but not extraordinary, because Sharpe penalises every move equally — including the large up days that drive the compounding. The Calmar ratio of 2.38, which only cares about how deep things ever got, is roughly five times the S&P's. The Calmar gap is the more honest read for a strategy of this design, because it captures the asymmetry: shallow drawdowns paired with hard up moves.

What 10,000 Alternate Histories Say About Risk

The Monte Carlo Test in Plain English

A backtest shows one version of history, the one that actually happened. A Monte Carlo test asks what the same performance would have looked like if events had arrived in a different order. Take the strategy's real trades and real trading days from the 2018 to 2024 build window, reshuffle them, and you get an alternate history the strategy could plausibly have lived through. Do that 10,000 times and you get the full range of outcomes the same underlying performance could have produced. We ran exactly that, starting every reshuffled history from the same $200,000 the backtest starts from, and looked at where the real result sits inside the range.

Where the Real Result Sits in 10,000 Histories

The first finding is about the destination. Not one of the 10,000 reshuffled histories lost money over the seven years. That is a statement about re-ordering a history that already contains the backtest's positive drift, not a promise about the future, and it says nothing about a market regime the strategy has not traded through. The worst 1 per cent of them still turned $200,000 into roughly $912,000, a 4.6 times multiple that works out to about 24 per cent a year. The middle of the range finished around 28 times the starting capital. Replayed on that same one-trade-at-a-time basis, the real order of trades finished at 28.8 times, which is the 51st percentile of the range: about half the reshuffles did better and half did worse, so the real sequence is an ordinary draw rather than a fortunate one. The actual backtested account over the same period finished at 24.6 times, or $4.92 million, and it is lower than the replayed figure because a real account holds several positions at once and sits partly in cash between signals rather than compounding every trade one after another. The result on this page is not a lucky ordering of events dressed up as a track record.

The second finding is about the path. The real backtest's worst fall was -24.1 per cent. When the reshuffling is done fairly, keeping calm stretches and stormy stretches of the market together rather than scattering individual days at random, that -24.1 per cent lands almost exactly in the middle of the simulated range. Half of the alternate histories fell harder at their worst point, half fell less. The headline drawdown on this page is what the strategy typically produces, not a flattering draw from the good end of the range.

The Bad End of the Range

The same simulations set expectations for the bad end of the range, and this part is worth reading before investing rather than after. In the unluckiest 1 per cent of alternate histories the worst fall reached -37 to -42 per cent, deeper than anything in the strategy's record so far. On losing streaks, the longest run of consecutive losing trades to date is five. The reshuffles say a run of eight or nine losers in a row is an entirely normal eventuality for a system that wins a little over half its trades, with every rule working exactly as designed. Either experience would feel terrible in the moment. Neither would, on its own, be evidence that the system is broken.

The version of this test most people run, and why we show both

Most Monte Carlo tests shuffle individual trading days at random. That sounds rigorous, but markets move in stretches. Calm periods cluster, stormy periods cluster, and this strategy is built to cut exposure when the stormy ones arrive. Scatter the days at random and the risk controls never get a fair look at what is coming, so the test overstates the risk. On this strategy the naive shuffle puts the chance of a fall deeper than the S&P 500's -33.7 per cent at 23 per cent, roughly six times the 3.6 per cent produced by the version that keeps regimes intact. We ran both versions, we show both in the chart above, and we report the fair one. The same instinct sits behind the plateau-centre parameter choice further down the page. A test result is only worth publishing if the test itself is honest.

For the technically minded, the two tests are a trade-level resample with replacement and a 126-day block bootstrap of daily returns, 10,000 runs of each, seed-fixed and reproducible. Every figure in this section is a simulation performed on backtested results. It is hypothetical, and neither past performance nor simulated performance is a reliable indicator or a guarantee of future performance.

To step through the mechanics, the paperwork to open the Interactive Brokers account, and whether the strategy is a fit for your portfolio, book a callback with an MFAM adviser. The administrative side of running the strategy, including custody, signal delivery and adviser execution, is set out in How You Access the Strategy at the bottom of this page.

Request a CallbackPrefer to learn the fundamentals first? Access the free trading course.

How It Works

The strategy runs three engines in parallel, each trading different signals across different instruments. The three engines are designed to work in different market regimes so that the strategy as a whole has exposure to trending up, trending down, and mean-reverting environments. The drawdown containment shown above is not an accident, it is the direct mechanical consequence of how the three engines are designed to switch leadership across regimes.

Trend-Long Engine

Identifies established uptrends using a combination of momentum indicators, moving-average filters, and a regime-detection layer. The engine stays out of the market when broader conditions do not support long-side trend-following. Exits are driven by volatility-adjusted trailing stops that tighten as a trade moves in favour.

Mean-Reversion Engine

Identifies short-term oversold conditions in volatile sectors and takes positions sized to capture rebounds. Exits again use volatility-adjusted stops, with discipline around capturing the first material reversion move rather than holding for extended trends.

Trend-Short Engine

The mirror image of the trend-long engine, applied to the inverse leveraged ETFs of the same underlying indices. It activates when sustained downtrends are confirmed by the regime layer, allowing the strategy to extract return from extended sell-offs rather than sitting in cash through them. Exits use the same volatility-adjusted stop framework as the trend-long engine.

Three Engines, Three Trade Profiles

The three engines produce very different trade shapes. The two trend engines are designed to catch extended directional moves and hold them through a sustained leg, which typically means multi-week to multi-month hold times. The mean-reversion engine is the opposite, entering after a short sharp dislocation and exiting as soon as price snaps back, often within a few days. The performance of the strategy is driven by the distribution of outcomes across hundreds of trades rather than by any single trade being reliable, though within that distribution a small number of large winners contributes most of the profit, as the trade-distribution section below sets out.

How the Three Engines Switch Across Regimes

The three engines have substantially uncorrelated exposure patterns. When long-side trend conditions are poor, the regime filter pulls the trend-long engine into cash. When short-side trend conditions activate, the trend-short engine takes over net exposure. The mean-reversion engine fills in when neither trend regime is dominant. In practice, leadership rotates depending on what the market is doing.

The 2018 Q4 sell-off and the 2022 rate-hike bear are the clearest illustrations. The trend-long engine was held in cash for extended periods through both, while the trend-short engine carried directional exposure on the way down and the mean-reversion engine captured the intervening relief rallies. In strongly trending bull years such as 2019, 2021 and 2024, the trend-long and mean-reversion engines run concurrently at high exposure while the trend-short engine sits in cash.

The mechanical consequence of this rotation is that the strategy is rarely flat across all three engines, and is also rarely fully exposed across all three at the same time. Net market exposure adapts to the current regime rather than running at a fixed level. This is the structural reason the strategy's maximum drawdown over the historical period was -24.1% versus -33.7% for the S&P 500, despite trading two- and three-times leveraged instruments. The regime filter and the trend-short engine together remove or reverse capital exposure when the environment does not support the long-side signal. Drawdown containment, and the alpha that comes with it, follows as a side effect of that discipline.

Why combining the three engines matters

Running only a trend-long strategy exposes an investor to years-long periods of poor performance when markets stop trending up. Running only a mean-reversion strategy leaves alpha on the table during extended bull runs. Running only a short-side strategy is structurally negative-carry against rising long-run equities. Combining all three gives the strategy something to do in every regime, which is why the combined results are meaningfully smoother than any engine alone.

Proprietary Signal Calibration

All three engines use a proprietary approach to signal tuning, allowing faster regime detection than conventional moving-average or crossover methodologies. This responsiveness is a core part of the edge and comes from extensive quantitative research rather than any single technical indicator.

For a plain-language walkthrough of the trend, mean-reversion, regime-filter and volatility-stop concepts this strategy is built on, access the free MFAM trading course.

Instrument Selection

The strategy trades a diversified basket of leveraged exchange-traded funds across the two trend engines and the mean-reversion engine. Instrument selection is deliberate and follows three principles. The first is that each instrument must sit in a market segment whose behaviour matches the engine trading it. Trend legs are placed in markets with a history of long, persistent directional moves. Mean-reversion legs are placed in sectors where sharp dislocations reliably snap back. The second principle is non-overlapping exposure. Each leg tracks a distinct sector or geography, so an adverse event in one does not cascade across the book. The third is liquidity. Every instrument is a top-tier ETF with deep order books, so fills are reliable and position sizing is not constrained.

Leverage is used intentionally. The two- and three-times-leveraged structure amplifies every signal, allowing the system to extract meaningful return from moves that would be uneconomic to trade in unleveraged form. The same leverage is what makes stop-loss discipline and regime filtering non-negotiable, and the strategy is engineered around that requirement.

Trend-Long Engine Instruments

US large-cap technology has produced some of the longest and cleanest trends of any major equity index over the past decade. The constituents are dominated by globally scaled businesses whose earnings trajectories unfold over quarters and years, not days, which gives a trend engine meaningful runway once a move is established.

The semiconductor cycle is one of the most structurally trending sectors in global equities. It combines a multi-year secular growth layer, driven by compute demand, artificial intelligence and industrial electrification, with a cyclical inventory cycle that creates sustained directional moves in both directions. Trend-following captures both.

Chinese equities move on a different set of drivers than US markets, including domestic policy cycles, stimulus rounds and property-sector dynamics. This non-US exposure gives the trend-long engine an independent opportunity set. When US markets stall, Chinese markets may be trending separately, and the system can capture that without taking additional US risk.

The artificial-intelligence and infrastructure build-out is the dominant multi-year capex theme in US equities, and the basket sitting underneath AIBU captures that flow at the index level rather than at any single name. Earnings revisions across the cohort move in the same direction for quarters at a time when capex rolls forward, which is exactly the kind of persistent direction the trend-long engine is designed to ride.

Biotech is one of the most idiosyncratic and headline-driven sectors in US equities, with binary clinical-trial outcomes, FDA decisions and acquisition flow producing sharp and sustained moves. The same drivers that pin the sector to multi-month sideways action also produce extended trending runs once a cycle establishes, whether through sustained M&A activity, pipeline progress across the cohort, or capital rotating back into small-cap biotech after a long drought. The trend-long engine is built to ride those phases when they fire.

Mean-Reversion Engine Instruments

Defense names move sharply on geopolitical headlines, defense-budget cycles and programme-specific news. The underlying thesis, sustained government spending, is structurally stable, so short-term dislocations caused by headlines tend to reverse quickly. That pattern is a textbook setup for a mean-reversion engine.

Energy is one of the most volatile sectors in US equities, with sharp moves driven by oil-price shifts, OPEC decisions and geopolitical events. The sector's underlying earnings power is anchored by large integrated producers whose long-term economics do not turn on a single headline, so the short-term overreactions reliably fade. That gives the mean-reversion engine a high-quality flow of dislocation-and-snapback setups.

Junior gold miners run on operating leverage to the gold price. A small move in the underlying commodity produces an outsized move in the equity, and those moves frequently overshoot in both directions on macro headlines, real-yield prints and dollar swings. The fade back to fair value is reliable enough to be a textbook reversion setup, and JNUG carries the additional property of being structurally uncorrelated with the rest of the book, since gold-miner pricing is driven by real rates and the dollar rather than by US earnings or Chinese policy.

Healthcare sells off hard on drug-pricing headlines, policy proposals and single-name trial failures, but the sector's earnings base sits with large, diversified pharmaceutical and managed-care businesses whose cash flows are not actually changed by most of those headlines. The gap between the headline reaction and the earnings reality is what the mean-reversion engine trades, and healthcare's defensive demand profile means its dislocations tend to be driven by different events than the energy, defense and gold-miner legs alongside it.

Trend-Short Engine Instruments

The inverse counterpart to TQQQ. When the regime filter confirms a sustained downtrend in US large-cap technology, the trend-short engine takes a position in SQQQ to capture the move. The same momentum and volatility-stop framework applies, mirrored to the short side of the same underlying index.

The inverse counterpart to SOXL. Semiconductor sell-offs are typically as sharp and persistent as semiconductor rallies, driven by the same cyclical inventory dynamics in reverse. The trend-short engine captures these legs when the regime filter confirms the downtrend.

The inverse counterpart to YINN. Chinese equity sell-offs driven by policy tightening, property-sector stress or geopolitical events tend to be sustained and offer extended trend-short opportunities that are largely uncorrelated with US-side directional moves.

The inverse counterpart to AIBU. AI-thematic drawdowns in 2022 and the mid-2024 chop both ran for months once they were established, driven by the same capex-cycle dynamics in reverse. The trend-short engine takes AIBD when the regime filter confirms the downtrend, applying the same volatility-stop framework as the long-side engine.

The inverse counterpart to LABU. Biotech sell-offs run for the same reasons biotech rallies do, often in extended drawdowns when capital rotates out of small-cap risk. The trend-short engine takes LABD when the regime filter confirms the downtrend, applying the same volatility-stop framework as the long-side engine.

Where the other trend-short legs are sector or country bets, SPXU is the broad-market one. Its role is the sell-off that is not confined to technology, semiconductors or China but is instead a general de-rating of US equities, the kind seen through 2022. When the regime filter confirms a sustained downtrend in the broad index, the trend-short engine takes SPXU under the same volatility-stop framework as every other leg.

Every Trade Matters

Quantitative strategies rely on statistical discipline. The distribution of individual trade outcomes over the backtest period demonstrates why taking every signal, without filtering, is a structural requirement.

Trade outcomes follow a long-tailed distribution. Most trades produce small positive or small negative returns, clustered near the mean, with a long right tail of outsized winners. The win rate across the period was approximately 54 per cent.

That right tail does the heavy lifting. The ten largest winning trades produced roughly 73 per cent of total profit over the period, and the fourteen trades that returned more than 40 per cent are only 5.8 per cent of the trade count. This concentration is normal for trend-following, where a minority of positions catch the sustained moves that pay for everything else, but it is worth stating plainly rather than leaving in the footnotes. It is also the practical reason every signal has to be taken: the outsized winners cannot be identified in advance, and a version of this record that skipped a handful of them would look very different. An investor should expect long stretches where the book grinds sideways between those trades.

Equally important is what happens on the left-hand side of the distribution. Most losing trades sit between zero and minus ten per cent, and the ten worst losses all sat between -26 and -42 per cent on the underlying leveraged ETF. The volatility-stop and per-leg risk-cap framework is designed to keep single-trade losses within that kind of range, though it cannot guarantee a maximum, since an overnight gap or a fast move can fill worse than any stop. There is no single catastrophic blow-up trade that unwound prior gains. The left side of the distribution is bounded by the risk-control framework rather than by chance.

Two risk controls produce this shape. The first is stop-loss discipline. Every position carries a volatility-adjusted stop that tightens as a trade moves in favour, so losing trades are exited mechanically at a pre-defined loss rather than allowed to deteriorate. The second is per-leg risk sizing, which targets a fixed dollar-risk budget per trade based on each instrument's recent realised volatility. High-volatility instruments receive smaller position sizes so that the dollar loss at the stop is consistent across the book. Combined, these two controls are what allow the strategy to run leveraged instruments without carrying catastrophic single-trade risk, and are the reason the left tail of the distribution stays bounded.

Why every signal is taken

The strategy takes every signal as it fires, without discretionary filtering. Long-tailed distributions reward consistency, because the largest winners cannot be reliably identified in advance. Skipping setups that look low-conviction would risk passing on the very tail trades that compound the curve, so the rules-based discipline is to act on every signal and let the distribution do the work. Hold-time profile reinforces this. The trend engines hold winners for weeks to months, the mean-reversion engine cycles within days, and the diversity of trade shapes is what makes the combined return path smoother than any single engine alone.

To step through the mechanics, the paperwork to open the Interactive Brokers account, and whether the strategy is a fit for your portfolio, book a callback with an MFAM adviser. The administrative side of running the strategy, including custody, signal delivery and adviser execution, is set out in How You Access the Strategy at the bottom of this page.

Request a CallbackPrefer to learn the fundamentals first? Access the free trading course.

Is This Just Curve Fitting?

A fair question to ask of any backtested strategy is whether the performance is real or whether the rules have been retro-fitted to the data until the equity curve looks good. This is called curve fitting, and it is the single most common failure mode of quantitative research. A curve-fit strategy will show a beautiful historical track record and then fall apart the moment it is asked to trade on data it has not seen. The numbers on the chart were engineered into existence, not discovered.

Curve fitting is easy to do accidentally. Any strategy has parameters, and any parameter can be tuned until the historical result is maximised. If you try enough combinations on the same dataset, something will fit that dataset almost perfectly by coincidence alone. The fit says nothing about the future because the rules were selected for that specific history, not for any underlying market behaviour. A properly engineered quantitative strategy has to be built in a way that makes this kind of overfitting structurally difficult.

How to tell curve fitting from a real edge

The cleanest test is a parameter sweep. Take the finished strategy, vary its core parameters over a wide range, and plot every resulting equity curve. If the strategy's performance collapses when the parameters move even slightly, the historical result was a lucky coincidence at one specific parameter setting. If the curves instead form a tight cluster, with every variant producing similar shape and similar ending value, the edge lives in the underlying rules, not in the specific numbers chosen. The parameter sweeps shown below were generated on the original six-leg development build of the strategy, which contains the trend-long and mean-reversion engines tested in isolation before the trend-short engine and the additional leveraged ETFs were folded into the deployed configuration. They were also run over a different window, January 2016 to the end of 2025, rather than the January 2018 to June 2026 window used everywhere else on this page, which is why their starting point and ending values do not line up with the equity curve at the top. They are shown to demonstrate parameter-stability methodology and are not intended to reproduce the headline performance figures above, which are calculated on the full deployed configuration across all three engines.

A well-built strategy has to be robust on both sides of every trade, the entry and the exit. Sweeping only one side leaves the other side unexamined. Both sides are tested independently below.

Exit-side robustness, the volatility-stop sweep

The exit side of the strategy is governed by volatility-adjusted stops. Each position is given a stop whose distance scales with how noisy the underlying instrument currently is, so a calm market produces tight stops and a noisy market produces wider ones. The question is whether the edge depends on the specific stop multiples chosen, or whether it holds across a range of reasonable values.

Every one of the twenty-five exit-parameter combinations beats the S&P 500 by a meaningful margin, and every curve follows the same overall shape through every drawdown and recovery. The cluster is tight, with ending values sitting in a narrow band relative to the total compounded return. There is no single knife-edge volatility-stop setting propping up the result. The exit logic works across the full plausible parameter space.

Entry-side robustness, the signal-length sweep

The entry side of the strategy is governed by lookback-window signals on each engine. Each signal has a lookback window that controls how sensitive it is. A shorter window produces more entries and more noise. A longer window produces fewer entries but waits for more confirmation. The second sweep varies the trend and mean-reversion lookbacks independently to test whether the edge survives different signal sensitivities.

Again, every combination beats the benchmark by a meaningful margin and every curve retains the same overall path. The entry logic is not hanging on one specific lookback value. Whether the lookback windows are shorter or longer than the deployed configuration, the strategy still produces a similarly shaped equity curve ending materially above the S&P 500. Entry and exit are independently robust, which is the stronger test because it rules out the possibility that one side of the system is carrying the other.

Plateau selection, why the deployed setting is not the peak

The plain-English takeaway first. When testing was finished, we did not deploy the single best-looking settings. We deliberately chose settings from the middle of a whole neighbourhood of similar settings that all perform well, so that if the market shifts a little, or our calibration is slightly off, the strategy does not change character. The rest of this section shows the evidence for that choice.

A common and valid question when looking at a parameter grid is whether the deployed configuration was simply picked as the highest-performing cell. If the development process had done that, the deployed setting would be sitting at the top of a narrow spike, and any small move away from it would collapse performance. That is the curve-fitting failure mode a sweep is designed to detect.

The selection method used here was different. The grid was inspected across multiple planes, with return stability and drawdown stability both weighing equally into the decision. The goal was not to find the single best cell on any one metric. It was to find a cell whose neighbours produced similar returns and similar drawdowns, so that a small parameter miscalibration in deployed trading would not change the character of the results. Both planes were considered together, and the deployed setting was chosen from the region where the neighbourhood was consistent on both.

The heatmap below shows the same 25 nearby combinations tested in the entry sweep above, five values of one entry setting crossed with five values of the other, with the actual values anonymised as x and y. Each square is coloured by its profit factor, which is simply total dollars won divided by total dollars lost, so any square above 1.0 is net profitable. It is the cleanest way to see whether the edge survives away from the deployed configuration.

The key feature is that every cell in the neighbourhood is green. Profit factor ranges from roughly 1.45 to 1.59 across the entire grid. A curve-fit strategy would show one green cell surrounded by red, with profitability collapsing as soon as any parameter moved. Instead, the whole neighbourhood is comfortably profitable. The edge is not sitting on a knife-edge parameter choice, it is being generated by the underlying rules and survives in every direction around the deployed setting.

The same broad stability shows up on the max-drawdown plane when it is inspected alongside this one. Drawdown is not uniform across the whole grid, but it clusters tightly in the region the deployed configuration was picked from, which is why both planes were weighed together at selection time rather than either one in isolation.

How the strategy was developed

The development process itself was designed to resist curve fitting, in three deliberate stages.

Stage one was building the base logic on unleveraged instruments. The trend and mean-reversion engines were designed and tested against one-times ETFs tracking the same underlying exposures, where signal behaviour is cleaner and leverage-related decay does not distort the data. The goal in this stage was to establish whether the underlying trading rules captured real market behaviour, independent of any amplification. If the rules did not work on the unleveraged instruments, they were not going to work anywhere.

Stage two was validation on data the rules had never seen, using both a backward and a forward out-of-sample test. The engines were built and their parameters chosen on the 2019 to 2022 window. Once the base logic performed on that development set, it was tested in two directions. Going backwards, the rules were run against the January 2018 to end-2018 window, which predates the build window and had never been seen during development. Going forwards, the rules were run against the 2023 to 2024 window, which had been deliberately held out of the build. If the rules had been curve-fit to the development data, performance on either out-of-sample window would have fallen apart. It did not, which is what gave confidence that the edge was structural rather than accidental.

Stage three was calibrating for the two- and three-times leveraged instruments actually deployed. Leverage changes the risk profile materially. During the 2023 to 2024 forward out-of-sample window, the volatility-stop multiples and regime-filter thresholds were re-tuned to accommodate the faster, larger moves that leveraged ETFs produce. This calibration did not change the underlying logic. It adjusted the risk-taking envelope so the same rules would operate safely on instruments that amplify every move by a factor of two or three. The rules themselves were not refit to the 2023 to 2024 data, only the risk-sizing parameters were recalibrated for leverage.

To connect this development history to the in-sample and out-of-sample labels used in the Historical Performance section at the top of the page, every stage described here, the building, the validating and the leverage recalibration, took place inside the 2018 to 2024 window. That is why the whole of 2018 to 2024 is treated as in-sample. The 2025 to June 2026 record is reported as out-of-sample because the deployed rules and parameters were fixed at the end of that development work and then run forward on data that arrived after the build, which makes it the strictest test on this page.

This staged process is why both parameter sweeps fan out tightly rather than collapsing when the parameters are varied. The underlying logic was validated before leverage-specific tuning was applied, so the strategy is not reliant on any specific choice of entry length or stop multiplier for its edge.

What this does not prove

A clean parameter sweep and a disciplined development process do not guarantee future performance. What they do is rule out the most common reason backtested strategies fail when deployed forward, which is that the rules were fit to the history rather than discovered from it. The edge here rests on the behaviour of the instruments and the market regimes traded. If those behaviours change materially, the strategy will change with them. What the sweep shows is that within the historical window, the edge was not an artefact of parameter choice.

Current Status

Performance figures on this page are a combination of two periods. The January 2018 to end-2024 portion is historical simulation constructed from actual market data using the strategy's current rules. The 2025 portion onward is the strategy running forward out-of-sample, with results accumulating on the same rules and all parameters frozen. Both segments are shown continuously on the same equity curve, with a marker indicating the boundary between the historical-simulation and forward-out-of-sample periods.

To step through the mechanics, the paperwork to open the Interactive Brokers account, and whether the strategy is a fit for your portfolio, book a callback with an MFAM adviser. The administrative side of running the strategy, including custody, signal delivery and adviser execution, is set out in How You Access the Strategy at the bottom of this page.

Request a CallbackPrefer to learn the fundamentals first? Access the free trading course.

How You Access the Strategy

The strategy is delivered as non-discretionary general advice. MFAM generates the signals and, once the investor authorises each one, the MFAM adviser places the order on the investor's behalf. The mechanics below are how that works in practice.

Your account, your custody

The investor opens their own account at Interactive Brokers. The account and all cash deposits are legally held by the investor, with client cash sitting in Interactive Brokers' segregated trust account under Australian and United States client-money rules. MFAM does not hold, pool, or control investor funds at any point. The account is yours, the money is yours, and you can close the account or withdraw at any time without MFAM's involvement. The MFAM adviser is added to the account as an authorised adviser with trading authority only, so orders can be placed on the investor's behalf once authorised, but cash cannot be moved out of the account by MFAM.

Signal delivery

General advice trade signals are issued to the investor by email and SMS during the trading day as the rules fire. Each signal is a specific instruction, the instrument, the side, and the size expressed as a percentage of portfolio. The investor only needs to reply yes to authorise. No action from the investor means no trade.

Execution

Once the investor has authorised a signal, the MFAM adviser places the order on the Interactive Brokers account. Orders are typically placed as market-on-open for the next United States session, which executes overnight Australian time. This matches how the strategy has been modelled, so executed orders track the backtest assumptions rather than drifting away from them.

Non-discretionary by design

Every trade requires explicit authorisation from the investor before it is placed. The MFAM adviser does not have discretion to enter or exit positions without a yes from the investor. This is general advice with client-authorised execution, not a managed account and not a managed fund. The investor decides whether any given signal is actioned, and can decline a signal or exit a position at any time.

Risk level is fixed, exposure scales with investment amount

The instruments used are a mix of two- and three-times leveraged ETFs, and the strategy's risk profile is fixed by its design rather than chosen by the investor. A rules-based position-sizing framework, with built-in per-position and portfolio-level risk limits, defines one risk profile that every investor receives, and that is the configuration the performance figures on this page are based on. The only dial the investor controls is how much capital to allocate to the strategy. A larger allocation produces a larger absolute swing in dollar terms, while the percentage return profile, drawdown profile, and per-leg risk budget remain the same regardless of investment size.

Cash-account structure, no broker margin

The strategy is engineered to run on an unmargined cash account. The investor's broker account holds the cash and the long ETF positions outright. There is no broker margin in use, no overnight financing or borrow cost, and no margin-call mechanic. The maximum loss on any individual trade is bounded by the position size and the volatility-stop, not by a forced-liquidation cascade triggered by a margin requirement.

The leverage that appears in the return profile comes from inside the underlying ETFs themselves. Direxion and similar issuers manage the daily rebalancing within each fund, and the investor pays for that operational service through the fund's expense ratio rather than through any borrow charge on their own account. This structure removes a class of failure mode — the gap-down forced-liquidation that ends careers in conventional margin-leveraged trading — and is the reason a strategy of this return profile can be run on a standard SMSF or retail brokerage cash account without margin-derived blow-up risk. Position-level losses on the underlying leveraged ETFs themselves remain real and material, and are managed by the strategy's volatility-stop and per-leg risk-cap framework.

Minimum investment

The strategy is offered from a minimum investment of AUD 20,000. There is no per-trade dollar minimum and no fixed monthly or platform fee. The all-in 30 basis-point per-fill charge applies on every entry and exit regardless of trade size, which works out to roughly 5 per cent per annum at the strategy's natural turnover. On a AUD 20,000 account that is approximately AUD 1,000 in annual fees, which the historical return profile is engineered to absorb. Fee specifics are discussed during the onboarding conversation with an MFAM adviser.

You have seen the full mechanics, the historical performance, the risk profile, and exactly how the account, signals and execution work in practice. The next step is a short conversation with an MFAM adviser to walk through the Interactive Brokers paperwork, sizing for your portfolio, and any questions on the system before you start.

Request a CallbackWant the fundamentals first? Take the free 5-day trading course.

General Advice Warning

The information on this page is general advice only. It is general in nature and does not take into account your individual objectives, financial situation, or needs, and it is not personal financial advice. Before acting on any information presented here, you should consider its appropriateness having regard to your own circumstances, read our Financial Services Guide, and where relevant consider the Product Disclosure Statement for any financial product referred to. If you are unsure whether the strategy is right for you, seek personal advice.

Hypothetical and Out-of-Sample Performance Disclosure

Performance data presented on this page combines two segments, both of which are hypothetical. The January 2018 to end-2024 segment is backtested, constructed with the benefit of hindsight using historical market data. The 2025 onward segment is forward out-of-sample, where the same frozen rules are applied to data that arrived after the development period closed, with execution simulated at the same market-on-open fills the backtest assumes. An all-in 30 basis-point per-fill charge is applied to every fill as a proxy for real trading costs, including an allowance for execution slippage, but neither segment otherwise reflects the full friction of actual real-money trading. Actual slippage, capacity constraints, fills timing, adverse selection, changes in market structure, or changes in the behaviour of underlying instruments over time may differ from that modelled allowance. Hypothetical performance, whether backtested or forward out-of-sample, is not an indicator of what actual trading would have produced, and should not be interpreted as a forecast of future performance.

Portfolio Construction

The backtest is run as a single shared pool across all three engines. Each leg is sized by a rules-based risk-budgeting method that scales position size to the instrument's recent volatility, with per-position and portfolio-level limits that cap total exposure when several signals fire at once. In deployed operation the engines run on a single Interactive Brokers account so that the position-sizing base across the deployed legs is the live portfolio NLV.

Commissions and Fees

Returns shown on this page are calculated net of an all-in 30 basis-point per-fill charge applied to the notional traded on every entry and every exit. The 30 bps is the actual per-fill figure used in the calculation, not a conservative stand-in. It bundles the MFAM management commission, broker commissions, bid-ask spread, and the realistic execution slippage of trading the underlying leveraged ETFs into a single number. There is no separate management fee, performance fee, or platform fee charged on top of the displayed returns. Exchange and regulatory pass-through fees, which a broker always passes through on top of commissions, sit outside this 30 bps figure. The strategy runs on an unmargined cash account so there are no financing or borrow costs to apply. Tax depends on the individual investor's circumstances and is not modelled in the figures shown.

Past Performance

Past performance, whether actual or hypothetical, is not a reliable indicator of future performance. Future results, including any forward out-of-sample period, may differ materially from the backtested track shown on this page.

Leveraged Instruments

The strategy trades leveraged exchange-traded funds. Leveraged ETFs carry materially higher risk than their unleveraged counterparts and can experience significant decay in volatile or sideways markets. They are not suitable for all investors and are generally inappropriate as long-term buy-and-hold investments. The strategy's rules-based approach seeks to manage this risk, but cannot eliminate it.

No Guarantee

MF & Co. Asset Management makes no representation or guarantee regarding the future performance of the strategy. Returns may be negative. You may lose capital.

About MFAM

MF & Co. Asset Management Pty Ltd (ABN 99 622 929 597) holds Australian Financial Services Licence (AFSL) 520442. This page has been prepared for general information purposes. To discuss whether the strategy may be appropriate for your circumstances, speak with an MFAM adviser.