Earn Income Using Options

Model Strategy

Options Income Strategy

The goal of the options income strategy is to generate a stream of income by selling options on the ASX 200 (XJO).

The MFAM Options Income Strategy is a model portfolio that is designed to sell medium-term options spreads to generate an income stream from an investment.

The strategy achieves this by:

- Using statistical analysis to understand the structure of the ASX 200 and tailoring a strategy to fit the structure of the market

- Exploiting a number of inefficiencies in the options market (the statistical edge)

- Using high probability options combinations along with good risk management and control to achieve a steady income

- Scale-in and scale-out methods to increase the probability of the trade and reduce the reliability of having to pick exact tops and bottoms

Not sure what a Options are? Check out this basic explanation from The Options Guide. For a more in-depth guide, check out the ASX Understanding Options booklet.

Table of Contents

- 1 Reduced unsystematic risk

- 2 Scalability

- 3 Liquidity

- 4 Statistically Researched

- 5 Market timing to increase edge on Bull Put spreads

- 6 Market timing to increase edge on Butterfly spreads

- 7 Scale-in increase the probability of profit

- 8 Frequently Asked Questions

- 9 Are my investment safe?

- 10 How will I receive the advice and how are the trades executed?

- 11 How much do I need to invest?

- 12 MF & Co. Asset Management

- 13 Get In Touch

- 14 Products & Services

What are the benefits of this strategy?

As this is a strategy run on the ASX 200, there are a number of benefits compared to single stock investing or even single stock options.

Reduced unsystematic risk

Unsystematic risk is a type of risk that is unique to a specific company or industry.

For example, if you were to invest in a gold stock – the unsystematic risk would be the collapse in the gold price. Another example would be the company running up too much debt and collapsing due to poor liquidity.

When you trade an XJO option, you are trading an option on the entire market. A similar analogy would be investing in an Exchange Traded Fund (ETF) versus investing in a single stock.

Even if there was a collapse in any one industry, a major shock would only be relatively minor across the entire ASX200.

Scalability

One of the great things about options is the ability to scale the trading from small to large, depending on your own risk appetite.

In single stock trading, we often see clients move to small-cap high-risk stocks, specifically to increase the volatility exposure on smaller positions.

Since XJO options are leveraged, we are able to generate relatively significant volatility with smaller position sizes, without taking on additional unsystematic risk by moving into the small-cap space.

It is possible to start with an account as small as $10,000 and still be adequately diversified.

Liquidity

Liquidity should always be a top of mind concern, especially if markets are experiencing higher than normal volatility.

Going back to our small-cap example, small-cap stocks tend to have really poor liquidity as well as a high spread between the bid and the offer price.

This means that entering and exiting trades can either be expensive, or potentially impossible if there is no buyer or seller on the other side of the trade.

With XJO options, market makers are mandated by the ASX to provide a market. This means that during normal market operations, the liquidity of XJO options is very high.

XJO options are the most traded options series and have the highest liquidity of all options listed in Australia.

Statistically Researched

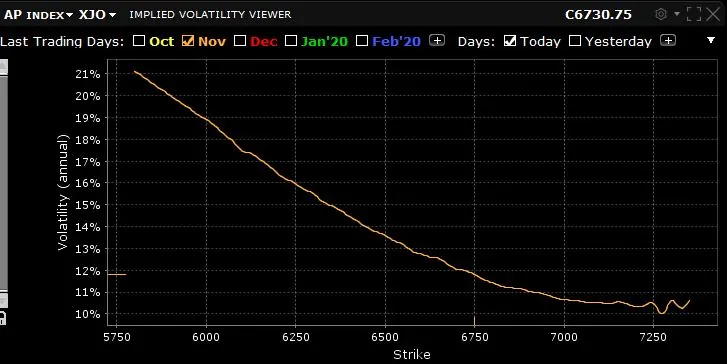

The XJO Options Strategy was designed through statistical research of the structure of the ASX200 and exploits the implied volatility skew of XJO options.

Rather than anecdotal evidence, thorough backtesting has being done to build a system which fits our unique Australian market.

Statistical analysis of the XJO / ASX 200

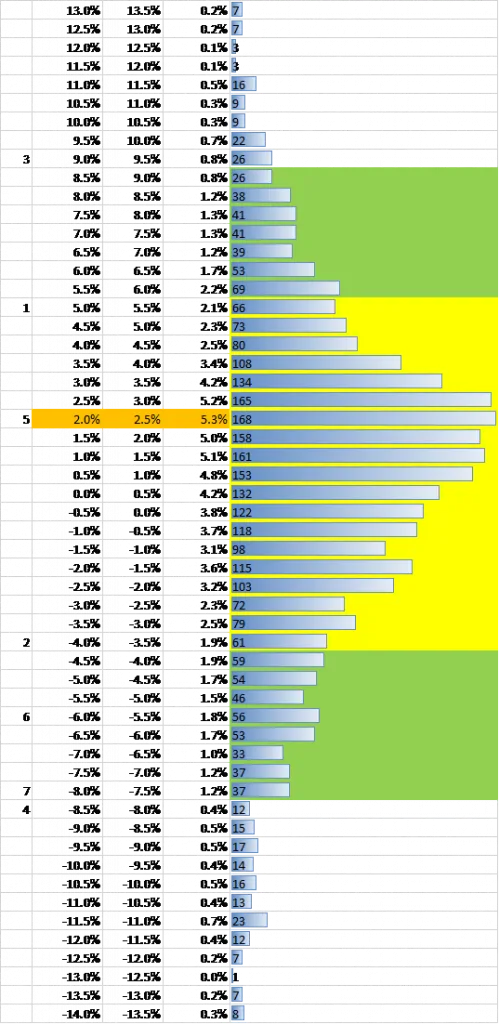

Based on backtesting of 35 trading days (59 calendar days) periods (3,171 data points) from 1 January 2007 to 30 August 2019, the Australian stock market has several distinct features of which we can use options to take advantage of (an edge).

The market has an up bias of 0.30% per 35 trading days

On a Compound Annual Growth Rate basis, on average, we can expect the Australian market to be up 1.82% CAGR.

This does not include dividends of around 4-5% per annum, which will mean the long term market return is around 6-7% CAGR.

1 Sigma (68%) of moves is between -4.0% to +5.0%

When looking at 1 sigma of moves over 35 trading days (yellow area, or between [1] and [2]), the market has a strong positive skew towards the upside with the peak [5] at 2.0% to 2.5%.

However, the distribution is fatter to the downside compared to the upside. This indicates the market on average grinds up in a small range but corrects down in a wide range.

2 Sigma (90%) moves show a fat tail and a downside skew

4% of rallies are above 2 sigma however [3], 6% of corrections are below 2 sigma [4] and the tail is long due to black swan events. This indicates that markets crash down, but not up.

The bell curve is a bimodal distribution, with corrections creating a second peak

The market’s main peak is at +2.0% to +2.5% [5] but there is a second peak at -5.5% to -6.0% [6]. There is also a steep drop off at -8.0% or less [7].

This peak is created from market corrections and the drop off is created from bounces. A correction of -5.5% or worse has a 13.0% chance of occurring – or once every 1.2 years.

Volatility skew of the options market

The volatility smile is the implied volatility (risk premium, or IV) of options at different moneyness.

Risk Premium is a function of both time and implied risk – like how insurance is priced.

The higher the implied volatility, the more expensive the insurance.

As an example, the insurance premium for an erratic driver would generally be higher than someone who has a clean driving record.

Additionally, a longer insurance contract will cost more. The cost of the premium also increases with time, as the probability of an adverse event happening also increases with time.

Taking this example, options can be used to hedge both upside moves (call options) and downside moves (put options).

However, the volatility smile is not even, as the cost of hedging the upside is cheaper than hedging the downside.

Hence, the volatility smile is skewed to the downside, or in other words, it cost more to buy insurance for the downside than it does to buy insurance for the upside.

In fact, the curve indicates that it can cost twice as much to insure the downside risk than to insure the upside risk.

There are several factors to this (which were shown earlier with the statistical analysis of the ASX).

Markets don’t crash up

Hence, the risk premium available for calls above 2-sigma is very limited when trading longer than 30-50 days.

The risk premium has a fat tail

This can be explained by investors buying insurance to hedge potential downside crashes. In fact, premium cost twice as much in the downside tail than the upside tail.

This risk premium fat tail is long

This can be explained by investors buying insurance to hedge 3 sigmas or more events, like the crash in 2008 and correction in 2020.

How to take advantage of these factors

We should positively skew our bets

Considering the market is generally grinding up, we should look to make bets which have a positive delta. In other words, trading with the general uptrend of the market.

Options are overpriced on the downside

The risk premium to the downside (put options) is overpriced because there is a demand imbalance where investors are buying correction/crash insurance. Hence, selling downside risk premium gives us an edge as downside premium is generally overpriced.

Options are underpriced on the upside

Since markets don’t crash up, there is a supply imbalance for the risk premium to the upside (call options). Hence, selling upside risk premium is generally not as profitable.

Using options to profit from the market

Based on statistical analysis and understanding of the volatility skew of the options market, we can then construct an options strategy which can take advantage of the structure and inefficiencies in the market.

Positively skewed bet by selling overpriced downside premium

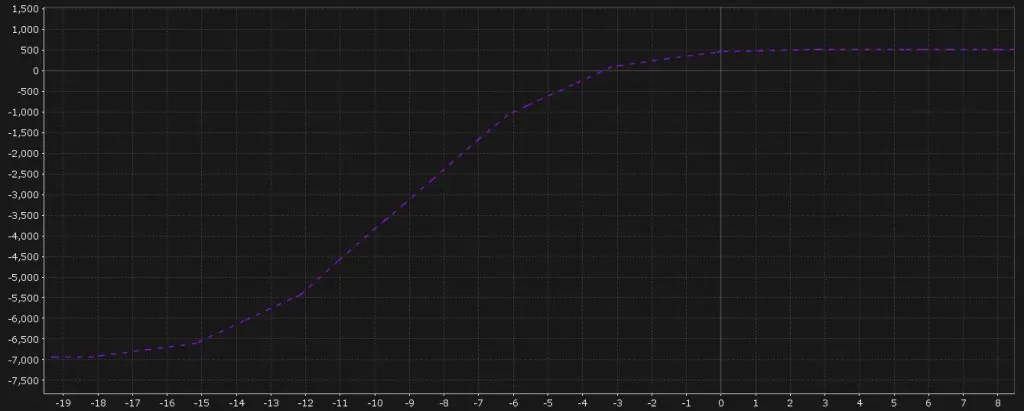

To take advantage of the overpriced risk premium, we initiate a Bull Put position that is approximately 7-10% out of the money (OTM) and 60-90 days to expiry. We plan to close the position with 2-3 weeks before expiry.

Not sure what a Bull Put is? Check out this explanation from The Options Guide.

This is to avoid gamma risk and gives us approximately 50~ days of exposure to match the statistical analysis.

A Bull Put spread is a high probability (85%+ win rate) low return strategy and is like selling insurance. By using a high probability trade, we can create a monthly income stream by selling insurance every month.

By initiating a position -7% or more OTM, we can avoid most of the minor corrections down to -5.5% and give us ample time to manage the position by rolling or closing the position when the market moves past the -5.5% to -6.0% correction level.

In addition, the premium below the 7% point is generally overpriced, as investors are now buying insurance for 3 Sigma or more events, such as the GFC in 2008. This is also illustrated in the volatility smile.

Example: The expected pay off diagram after holding the position after 45 days (purple line):

The breakeven point for this position is -3.4%. This means that if the market doesn’t fall more than 3.4% in the next 45 days, the position will be profitable. This position produces a profitability range from -3.4% to infinity.

The main thing to take away from this graph is that the profit is pretty much flat if the market moves up in the next 45 days – even if the market is up more than 5% or even 100%.

However, we know from our statistical analysis 1 sigma for the market is at +5.5%, with 2-sigma at +9.0% and 96% of all returns below the 2 sigma line.

This means that we can start sacrificing the upside from +5% onwards to increase returns which better resembles the shape of the bimodal distribution.

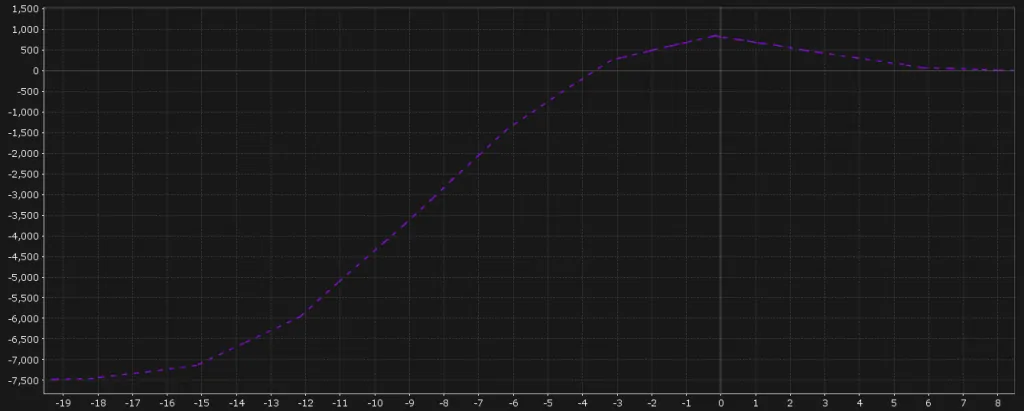

Reduce the upside potential to increase multimodal distribution peak profit

Since markets rally less than +9%, 96% of the time, by adding butterfly spreads, we can increase the profit potential of the position.

By sacrificing upside (and adding minimal downside risk), we can increase the upside potential within the 1 sigma range (-4.0% to +5.5%).

A Butterfly spread is a position that bets the market will stay between two strikes. This is done by reducing profitability in the tails to increase profitability in the centre of the distribution.

Not sure what a Butterfly spread is? Check out this explanation from The Options Guide.

Essentially, this squeezes up the profit distribution graph by decreasing profitability on the wings:

By placing a Butterfly spread, we have achieved several things:

Profit range reduced from -3.4% to infinity, to -3.6% to +9.0%.

Even though we have reduced the profit range from infinity to 9.0%, markets do not move more than +9.0%, 96% of the time.

There is a large edge here, as by reducing this range we were able to increase profit potential by 60% at the peak closer to the middle of the distribution.

We were also able to increase the range of profit on the downside by 0.2%, from -3.4% to -3.6%.

In addition, we are able to roll the butterfly spread further down to widen the lower end of the profit range from -3.6% to -4.0% and more.

Increased profit potential by 60%.

The top of the peak now has a profit potential that is 60% higher than without a Butterfly spread in place. There is a large edge here, as we know from the statistical analysis the market generally moves between -4.0% and +5.5%, well within our profit zone.

There is also a small increase in potential downside risk by 8%. However, this is minor as a position such as this would be rolled, or it would hit stop loss well before it gets to this range.

Market timing to increase edge on Bull Put spreads

Since Bull Put spreads depend on the market to grind up, we have several rules in place to increase the probability of the trade.

We aim to open such a position when the market experiences a temporary pullback and we experience a spike in implied volatility.

This further increases our win probability and our edge.

Market timing to increase edge on Butterfly spreads

Since the Butterfly spreads create a tighter profit band, profit is reduced from +2.5% onwards compared to just a Bull Put spread.

By timing our entry and only opening a butterfly spread when markets are technically overbought, we can once again increase our profit potential.

Scale-in increase the probability of profit

Picking the tops and bottoms of markets is exceptionally hard.

By using a scale-in method when entering trades, we increase the probability of profit by taking multiple positions as the market moves against us and the probability of the market moving in the right direction increases.

High Probability, Statistically Researched Trading Strategy

By initiating positions with an up bias and adjusting our potential payoff to fit the Australian market structure, we are able to profit from the options market with a statistical edge.

In summary, these are the combined edges that we take advantage of when trading the options on the Australian market (35 trading days or 59 calendar days).

- Statistically, the market has an upside bias of +2.0% to +2.5%. We exploit this edge by having a positive delta within our portfolio.

- Statistically, at 2-sigma, 96% of all up trends are less than 9%. We exploit this edge by sacrificing upside beyond 9% to increase upside inside 1 sigma (-4.0% to +5.5%) where the probability is much higher.

- In general, downside risk premium is overpriced due to portfolio managers buying put options to hedge downside risk. We exploit this edge by selling that risk premium when the risk premium is overpriced.

- We use technical analysis to determine when the market is overbought and oversold, to increase our edge when opening our positions.

By using a number of statistical edges and a high probability options strategy, our aim is to generate a consistent income with options.

Frequently Asked Questions

Are my investment safe?

MF & Co. acts as a broker and does not hold any of your investments or cash.

For US and international investments, we use Interactive Brokers (IB), a NASDAQ listed US$25b broker and one of the largest brokers in the world.

For international investments, a custodial solution is required as the ownership structures across global borders is more complex.

However, your assets are held beneficially under your name.

IB is stringently regulated by the SEC and all client funds are segregated and never used for working capital.

How will I receive the advice and how are the trades executed?

We provide non-discretionary general advice, which means we will never place a trade without your explicit permission.

When we identify an opportunity, we will contact you by email or phone depending on your preference. You will receive the full details of the trade, including why we are recommending it and the risk parameters involved, so you can make an informed decision before anything is executed.

To approve a trade, simply reply to the email or call us to confirm. You are always welcome to discuss the details with us before giving the go-ahead.

Because every trade requires your approval, if you are not comfortable with a recommendation you can simply pass on it and nothing will be placed.

How much do I need to invest?

The minimum investment will depend on the strategy that you are looking for, to ensure that the brokerage fees and leverage if used on the account are reasonable. Speak to one of our advisers for more information.

got more questions?

Contact

Get In Touch

Get into contact with us now for more information or to get started with this strategy.

MF & Co. Asset Management

MF & Co. Asset Management is a boutique investment firm offering Equity Capital Markets and derivative general advice & trade execution services.

We are specialists in advising and trading in Australian and US Equities, Index & Equity Options and Options on Futures.

Contact

Get In Touch

Australia

1300 889 603

International

+61 2 8378 7199

M-F: 8am-5pm

Suite 803, Level 8

70 Pitt St, Sydney, NSW 2000