Institutional sell-side rates Nick Scali a Buy with a 12-month price target of around A$20. The stock closed at approximately A$14.47 on 9 May 2026, implying roughly 38 per cent upside before dividends. The thesis is built on three pillars: ANZ gross margins that sit 10 to 15 percentage points above the retail peer set, a fully franked dividend yield approaching 5 per cent on a forward basis, and a UK expansion that has produced its first real proof of concept in the February 2026 half-year result.

Research published 11 May 2026. Price target and upside based on prices at time of publication.

Table of Contents

About Nick Scali

Nick Scali was founded in 1962 by Nick Scali in Mortlake, New South Wales, and listed on the ASX in 2004. The business sells premium imported furniture through its eponymous store network, which has grown to more than 60 locations across Australia and New Zealand. The 2021 acquisition of Plush Sofas for A$103 million added a second brand and roughly 70 further stores, lifting the combined ANZ store count above 90 and significantly expanding the addressable market. The UK business operates roughly 14 stores under the Fabb Furniture brand, with management actively refurbishing locations to the Nick Scali fitout standard and introducing the core Australian product range. Nick Scali has a June financial year end. More on the company at nickscali.com.au.

The 1H26 Result

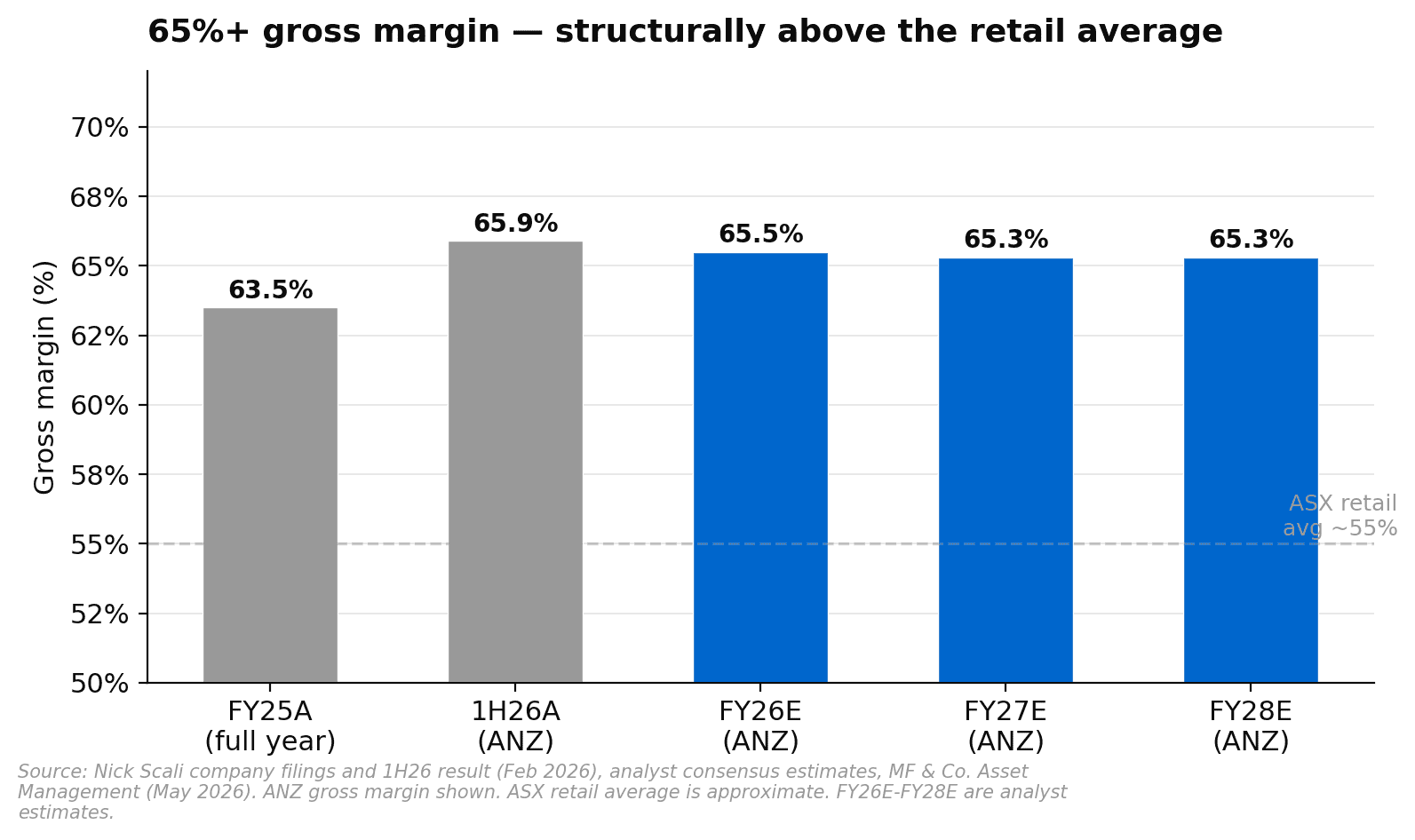

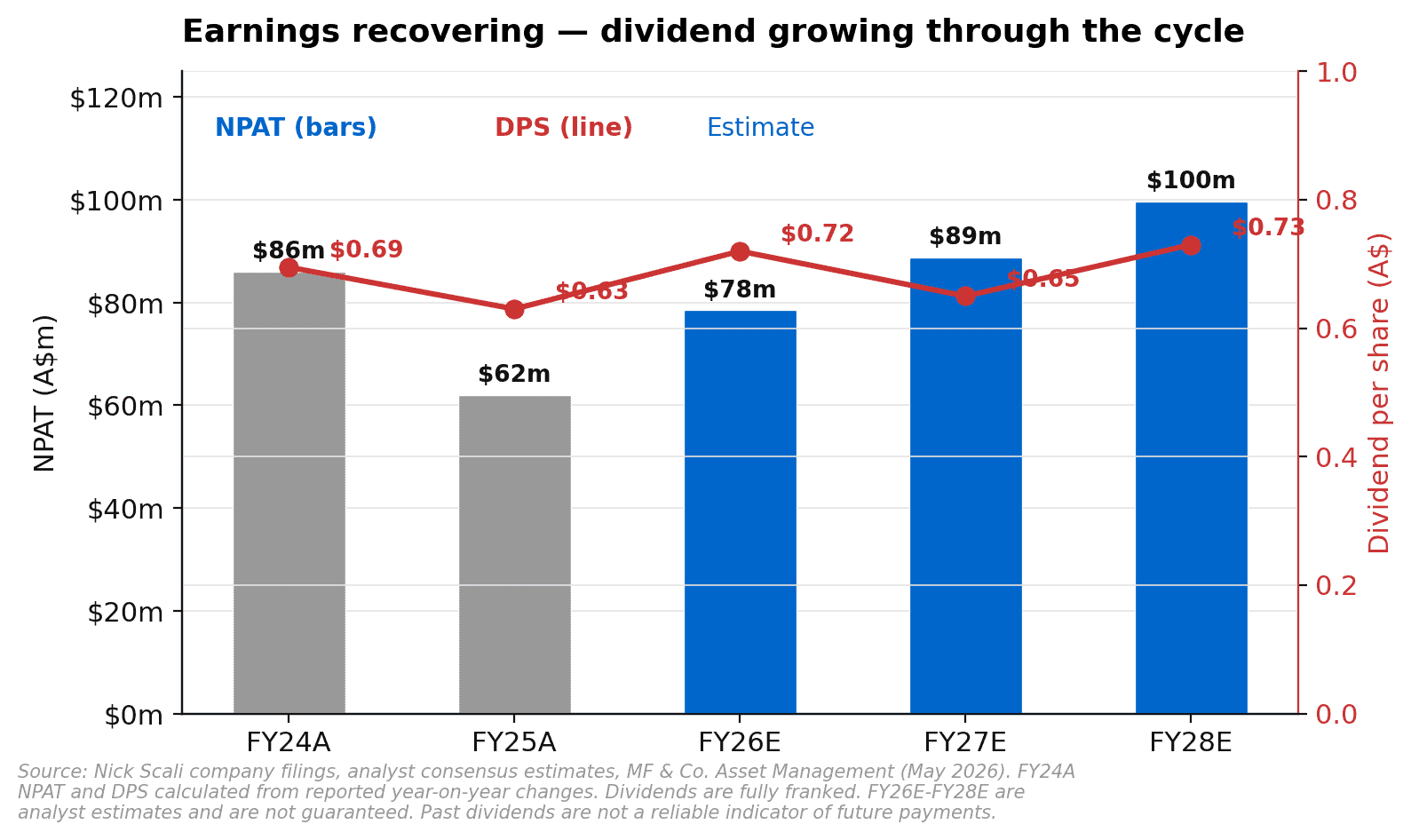

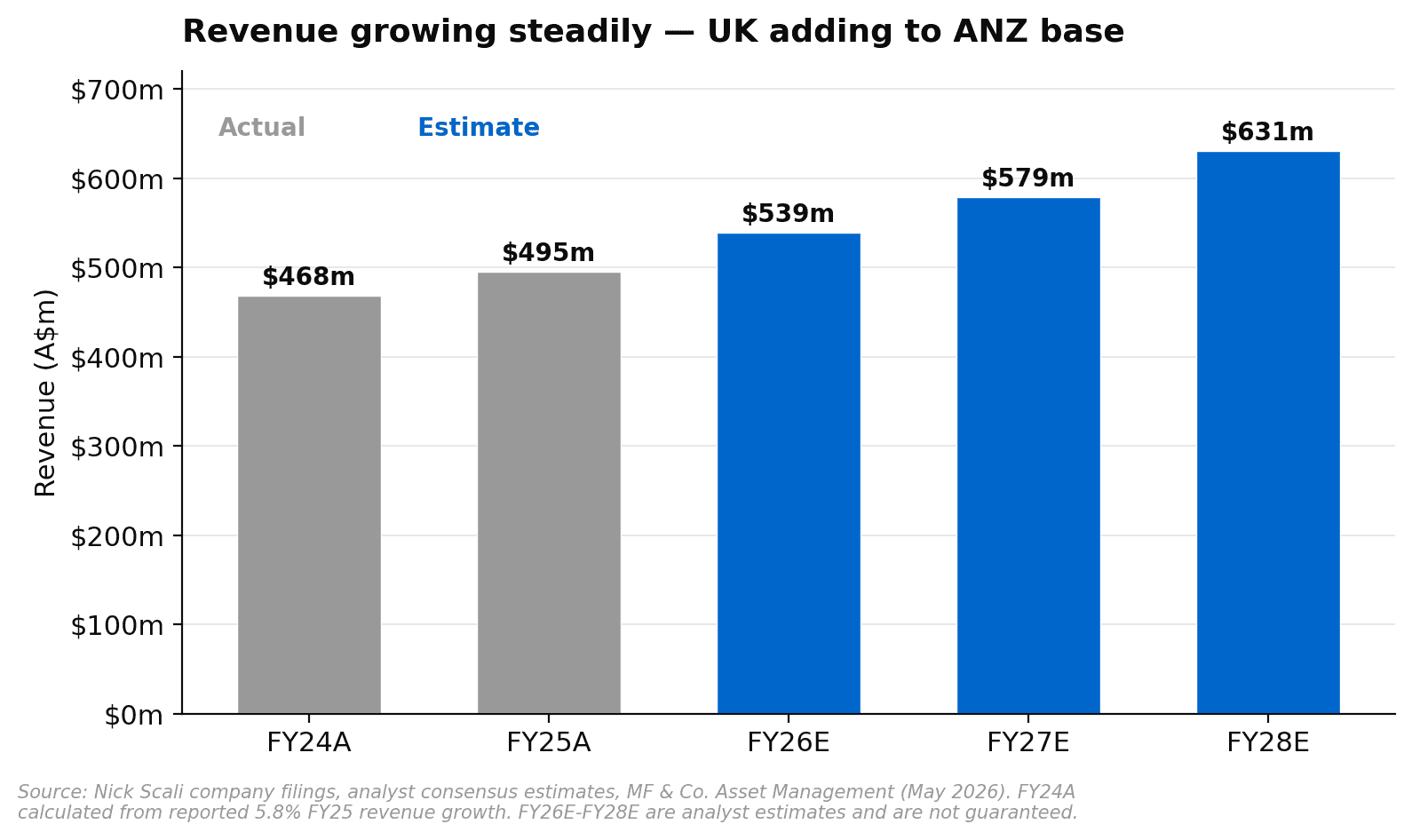

The headline numbers were ahead of expectations. Net profit after tax of A$41 million came in above the guidance range of A$37 to A$39 million that management had provided in late December. Revenue for the half was A$269 million, up 7.2 per cent year on year, with ANZ revenue of A$252 million growing 13.1 per cent as written order growth of 10.5 per cent flowed through. The ANZ gross margin of 65.9 per cent was approximately 60 basis points ahead of expectations and 139 basis points above the prior corresponding period, which is the number that carries the most weight for the long-term thesis.

The interim dividend was 39 cents per share, fully franked, up 30 per cent on the prior year interim. The UK posted a statutory loss of around A$5 million for the half on revenue of A$18 million, which is broadly as expected given the ongoing refurbishment program.

The one soft note in the result was the January trading update. ANZ same-store sales grew 3.2 per cent in January against a negative 8.5 per cent comparison period from the prior year, which implied underlying demand moderated more sharply than expected into the summer. Management attributed the deceleration to pull-forward of demand into the strong November promotional period, lower foot traffic, and broader consumer caution. The stock re-rated sharply lower on the day, and has continued to drift from the pre-result level of around A$24 to the current level near A$14.47.

The Margin Story Is the Structural Advantage

Most Australian retailers operate on gross margins in the low to mid 50s per cent. Nick Scali operates at 65 per cent. That gap reflects a buying model that sources premium product directly from manufacturers in Asia, avoids the mid-market discount bracket where margins compress, and sells through a store environment designed to feel aspirational rather than promotional. The 1H26 result confirmed the margin is holding even through active promotional periods, which matters given how aggressively Nick Scali leaned into November trading to drive the written order growth that flattered the first half.

The UK segment also surprised on margin, printing 59.2 per cent gross margin in 1H26, well ahead of expectations and approaching the ANZ level faster than the market had anticipated.

A Dividend That Has Grown Through Economic Cycles

Nick Scali paid a full-year FY25 dividend of 63 cents per share, fully franked. The FY26 full-year dividend is estimated at around 72 cents per share, which at a price of A$14.47 implies a forward fully franked yield approaching 5 per cent. On a gross basis for an investor on a 30 per cent marginal tax rate, that is roughly 7.1 per cent. The dividend is supported by genuine free cash flow generation. Nick Scali produced A$101 million in free cash flow in FY25. The payout ratio ran at approximately 86 per cent in FY25 and is expected to ease toward 63 to 79 per cent across FY26 to FY28 as earnings recover, which provides a buffer for the dividend without requiring a cut.

UK Expansion: Early Proof the Format Travels

The UK business has been loss-making since acquisition and will remain so for another 12 to 18 months. What changed in the February 2026 result is that the refurbished store format started producing verifiable numbers. The four UK stores that have been trading under the updated fitout for at least 12 months posted like-for-like sales growth of 32 per cent in January 2026. Management lowered the UK EBIT breakeven revenue threshold from A$53 million to A$51 million, signalling that the cost structure is improving as the network matures, and is actively negotiating further store locations.

The UK is not the primary reason to own Nick Scali today. But at a market capitalisation near A$1.25 billion, the UK growth option is effectively priced at zero on top of the ANZ core. If the refurbished format continues to track, the UK becomes a meaningful additional earnings leg within three to four years.

Where We Land on Valuation

At A$14.47, Nick Scali trades at approximately 14 times FY27 estimated earnings per share of around A$1.04. That is in line with the long-term historical average for this business. The stock was trading at 18 times forward earnings above A$18 as recently as February 2026, a premium that has now unwound as the market repriced for the softer January trading data and broader consumer discretionary weakness.

Revenue across both segments continues to grow, and the earnings recovery through FY26 and FY27 is not contingent on unusual assumptions. It reflects written order growth flowing through to revenue, gross margins holding at current levels, and UK losses gradually shrinking.

Risks to the Buy Call

The core risk is the ANZ consumer. Nick Scali’s revenue correlates with housing activity, renovation spending and consumer confidence. The January 2026 same-store sales read of 3.2 per cent against a weak comparison suggests underlying demand moderated through the summer, and a prolonged period of elevated rates or weak housing transaction volumes would put pressure on near-term estimates.

The UK expansion is a second risk. Each new store requires upfront fitout capital and runs at a loss for one to two years. If the UK rollout accelerates while ANZ is soft, the combined cash drag could weigh on dividends or stretch the balance sheet beyond current expectations.

Finally, Nick Scali has a relatively small market capitalisation and a concentrated ownership structure. Liquidity can be thin in risk-off periods, and the stock can move materially on limited volume when institutional positioning shifts.

Our View

Institutional sell-side has the stock at a Buy with around A$20 of fair value. At 14 times FY27 earnings and a forward fully franked yield approaching 5 per cent, the risk-reward looks attractive after the significant re-rating from A$24 to A$14.47 over the past three months. The margin structure is genuinely differentiated, the dividend is growing, and the UK expansion has moved from drag to early-stage proof of concept. The combination of earnings recovery through FY26 and FY27, UK optionality priced at near-zero, and a valuation back at the long-run average is why we think NCK is worth a close look at current prices.

If you would like to discuss Nick Scali or how it might fit within your portfolio, request a callback or call us on 1300 889 603. The above is general advice and does not consider your individual circumstances. Past performance is not a reliable indicator of future returns.