ResMed has drifted lower over the past two months even as the operating story has quietly improved. We are reiterating our Buy view on the stock. Institutional sell-side research carries a 12-month price target of A$46.70, against a closing price of A$26.68 on 19 June 2026 and roughly 75 per cent upside to that target. The argument is that the two worries which have weighed on the share price, a slowdown in new patient starts from GLP-1 weight-loss drugs and the return of Philips to the United States market, both look more like sentiment than substance, while a stack of growth levers introduced over the past few years is only now starting to scale. The stock still holds the number one global share position in obstructive sleep apnea devices and trades at a discount to its medtech and ASX healthcare peers.

Research published 23 June 2026. Price target and upside based on prices at time of publication.

About ResMed

ResMed Inc is the world’s largest manufacturer of devices and masks used to treat obstructive sleep apnea, the breathing disorder that affects close to a billion people globally. The company was founded in Sydney in 1989 and is dual-listed on the ASX and the New York Stock Exchange, with its primary operations and reporting in US dollars and a June fiscal year end. The product range is built around the AirSense and AirCurve devices, the AirFit and AirTouch mask families, and a growing software business that helps durable medical equipment providers, sleep clinics and hospitals manage patient compliance and reimbursement. More recent additions include the AirMini travel device, the Noctrix wearable for restless legs syndrome acquired in June 2026, a new range of AirCurve 11 non-invasive ventilators, and a partnership with the wearable maker Oura to widen the funnel of patients screened for sleep apnea. More on the company at resmed.com.

The GLP-1 Overhang Is the Wrong Worry

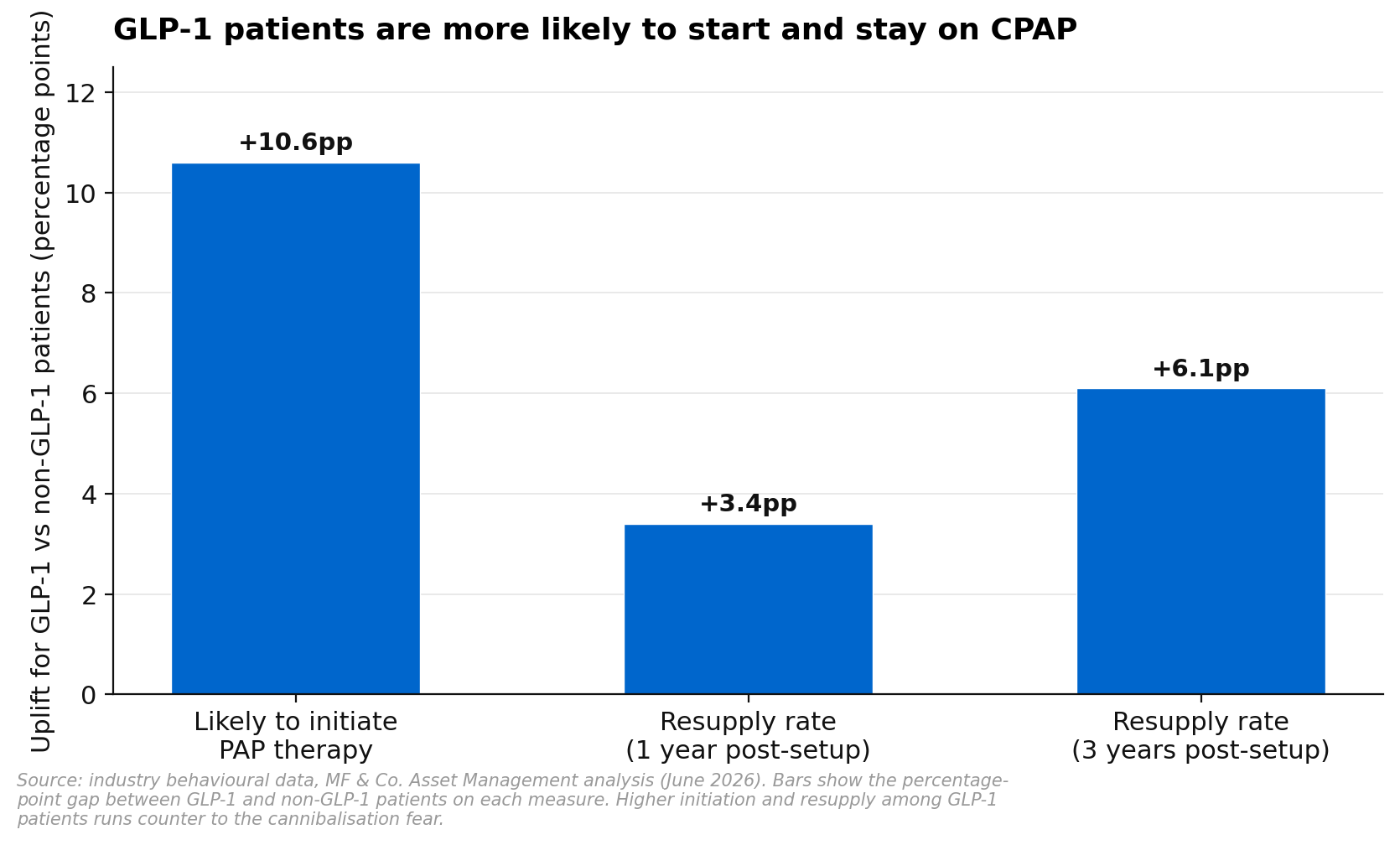

The single biggest cloud over ResMed for the past two years has been the fear that GLP-1 weight-loss drugs would shrink the market for CPAP therapy. The logic runs that as patients lose weight they stop having sleep apnea, so demand for ResMed’s devices and masks falls away. It is a clean story and it has kept a lid on the multiple. The trouble is that the data keeps pointing the other way.

Patients who are on a GLP-1 are actually more likely to start sleep apnea therapy, and more likely to stay on it, than patients who are not. The behavioural data shows GLP-1 patients are around eleven percentage points more likely to begin therapy in the first place, and their resupply rates run several points higher at both the one-year and three-year marks. The most plausible explanation is that being prescribed a GLP-1 puts a patient in front of a doctor and into a health-conscious frame of mind, which is exactly when sleep apnea tends to get diagnosed and treated. Far from cannibalising the funnel, the weight-loss wave appears to be feeding it.

The clinical picture is moving the same way. Eli Lilly reported in June that a late-stage trial of its next-generation drug met its goal of reducing the severity of sleep apnea, with the company planning to file for approval in the second half of 2026. Rather than a threat, the emerging view is that drug therapy and CPAP will be used together, with the device doing the heavy lifting on the breathing disorder while the drug addresses the weight. A major home medical equipment distributor recently pointed to strong resupply growth despite the rapid take-up of oral weight-loss drugs, which is the cleanest real-world read that the installed base is not eroding. Sleep apnea is also not only a weight problem. Anatomy, age and airway shape explain why slim people are diagnosed too, so the addressable market is wider than the obesity overlap on which the bear case rests.

The Growth Levers Are Stacking Up

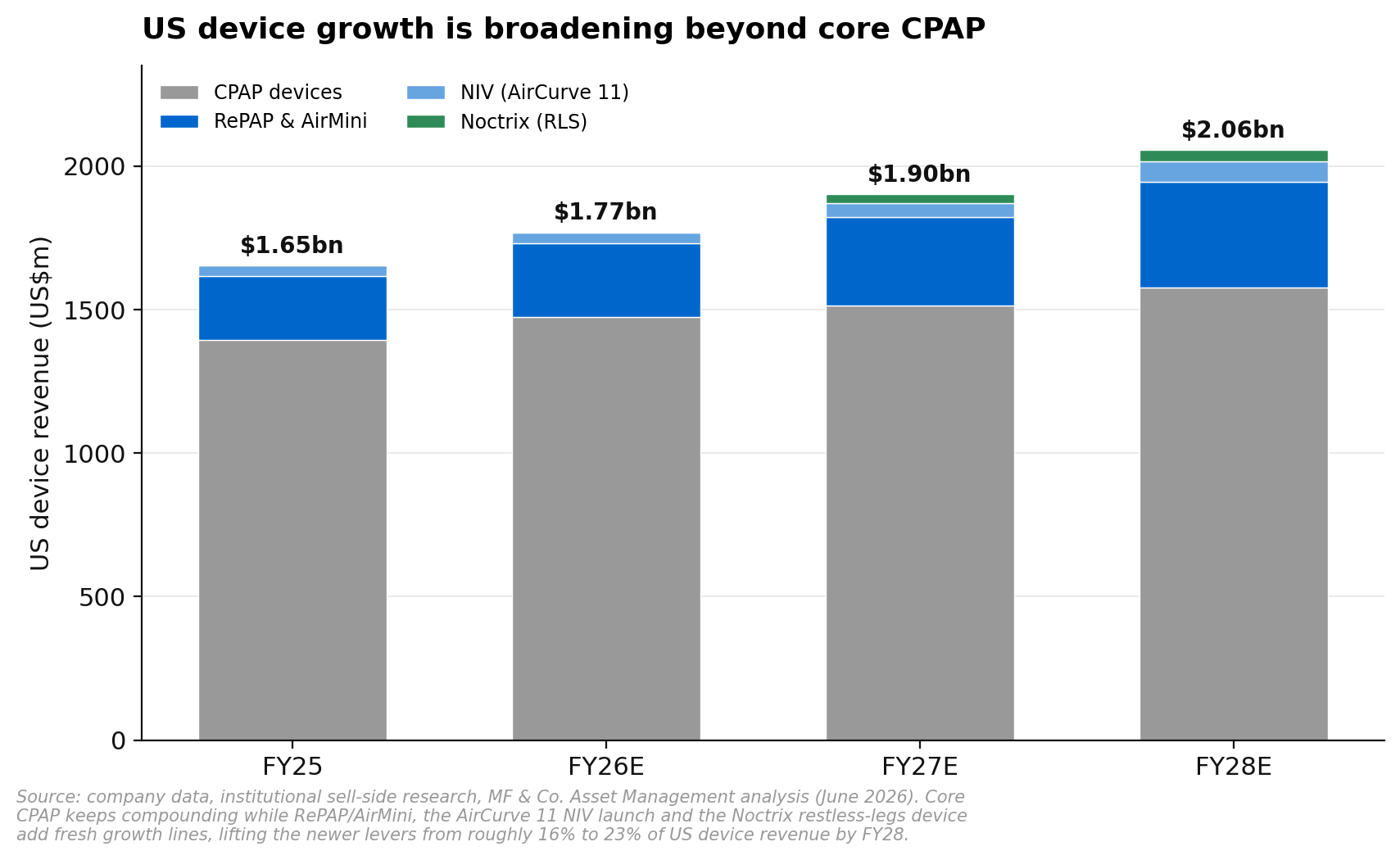

While the market has been preoccupied with the GLP-1 debate, ResMed has been building several new sources of growth that are independent of the core CPAP cycle. Each is small today, but together they broaden the growth base and reduce the company’s reliance on any single product.

The first lever is the upgrade and travel opportunity inside the existing patient base. ResMed’s RePAP programme targets the millions of patients due to replace ageing devices, while the AirMini, a pocket-sized travel CPAP that sells for several times the price of a standard machine, opens up the cash-pay market. Management has pointed to strong growth here after lifting marketing spend, and the partnership with Oura adds a new front door. Oura has more than five million paying members on its ring platform, a large share of whom report living with a chronic condition, and the tie-up routes members who show signs of disturbed breathing toward a sleep assessment and, where appropriate, into ResMed’s diagnostic network.

The second lever is the move into ventilation. ResMed has launched a new range of AirCurve 11 non-invasive ventilators in the United States aimed at patients with chronic obstructive pulmonary disease and related conditions, an initial market it estimates at around five million patients with a far larger long-term opportunity beyond that. A change to United States Medicare reimbursement rules in 2025 made these devices easier to prescribe and fund, which is a direct tailwind to adoption.

The third lever is restless legs syndrome. In June 2026 ResMed completed its acquisition of Noctrix for around US$340 million, a medical device maker whose Nidra system treats moderate-to-severe restless legs with nerve stimulation rather than drugs. Roughly 1.7 million people in the United States have a form of the condition that does not respond well to medication, and the overlap with sleep apnea is high, so ResMed can reach these patients through the sleep specialists and prescription channels it already serves.

A fourth lever sits outside the United States. ResMed launched a digital service called AirConnect Dx in the United Kingdom in May 2026 to help the National Health Service clear its sleep-test backlog, which now runs to more than thirty-five thousand patients waiting for a study. The service speeds up diagnosis and charges the health service a fee, so it is a revenue line in its own right as well as a way to pull more patients into therapy. Add in the steady replacement of ageing devices as old 2G and 3G mobile networks are switched off across Europe, and the picture outside the United States is one of durable, unglamorous growth.

Philips and the Second Overhang

The other worry that has held the stock back is the return of Philips to the United States sleep market. After years of recall and remediation, Philips is close to being a credible competitor again, and some normalisation of ResMed’s unusually high market share is a reasonable expectation from FY27. The point is that this is well understood and already in the share price. ResMed’s response has been to keep refreshing its product line, with the AirSense platform, new masks and the AirCurve 11 launch all designed to defend share before any Philips return gathers pace. The recent commentary on share gains suggests the strategy is holding, and a modest give-back of share from a dominant position is a very different thing from the structural loss the multiple seems to imply.

Margins Still Have Room

Underneath the top line, the margin story has further to run. ResMed has guided to a non-GAAP gross margin of 62 to 63 per cent in FY26 and is targeting double-digit basis points of accretion every year through to the end of the decade. The drivers are concrete. Headcount tied to the cost of goods has grown far slower than revenue, the manufacturing footprint in Singapore is being used more intensively rather than expanded, and the newer products, including the fabric masks, the AirMini and the ventilators, carry higher margins than the older equipment they sit alongside. Bolt that margin expansion onto high single-digit revenue growth and a largely fixed cost base, and the result is earnings per share growing in the mid-teens out to FY28. The buy case is less a story about revenue surprising and more about margins and earnings proving more durable than the market expects.

Valuation and the Case for a Re-Rate

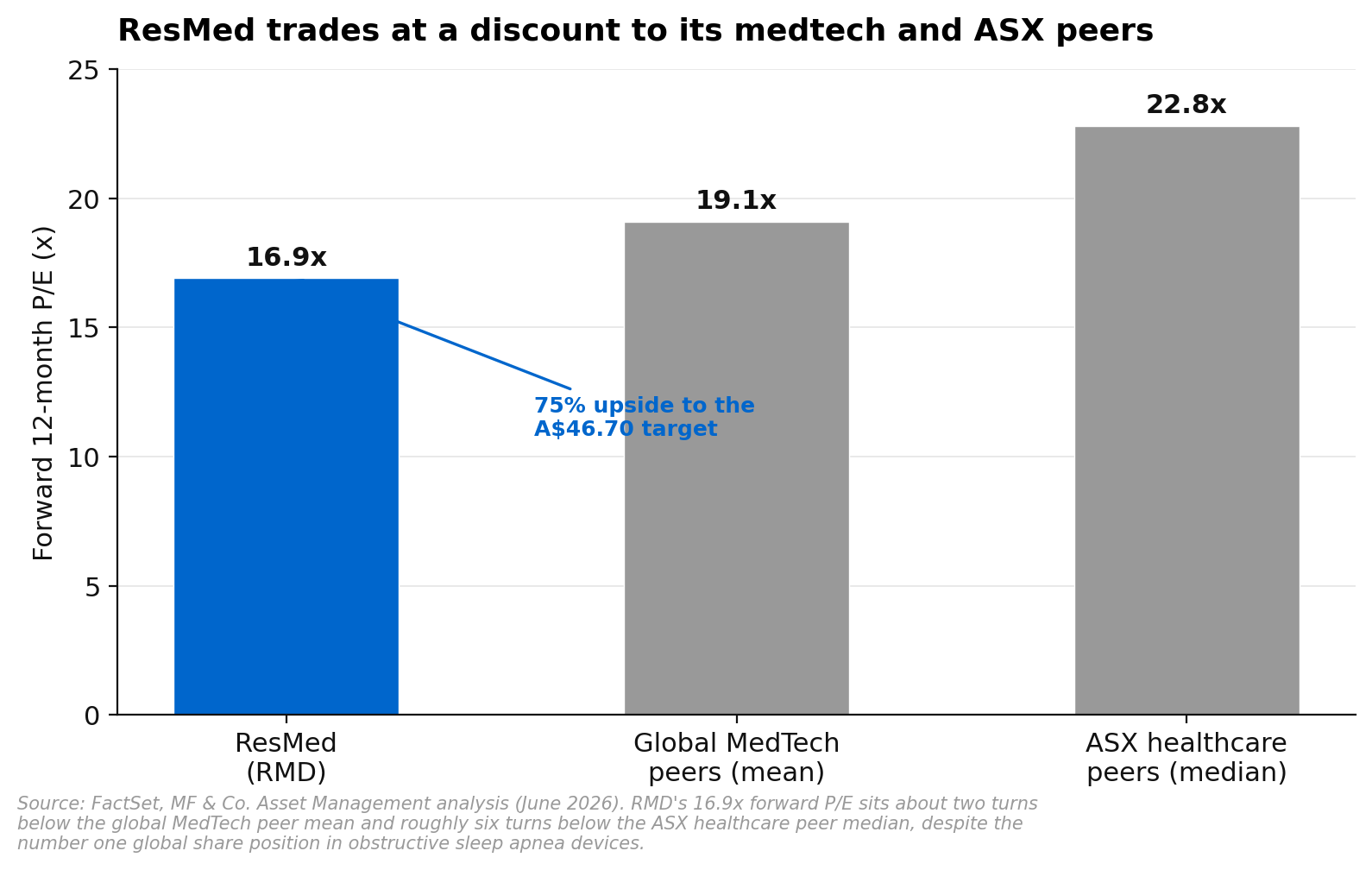

ResMed trades on a forward 12-month price-to-earnings multiple of around 16.9 times. That sits roughly two turns below the average of its global medtech peers and around six turns below the median of its ASX-listed healthcare peers. For a business with the number one global share in its core market, mid-teens earnings growth, a net cash balance sheet and a return on capital in the mid-twenties, that discount is hard to justify on the fundamentals.

The discount looks like the GLP-1 and Philips worries being double-counted into the multiple. As the patient-flow data continues to hold and the new levers scale, the gap between ResMed’s rating and its peers is the part of the story most likely to close. The 12-month target of A$46.70 is built on a blend of a ten-year discounted cash flow valuation, using an 8.1 per cent discount rate and a 3.0 per cent terminal growth rate, and a forward earnings multiple in line with where the business should trade given its growth. That blend implies roughly 75 per cent upside from the current price. ResMed pays only a small dividend, with a yield near 1.3 per cent and a payout ratio around a fifth of earnings, so this is a capital-growth case rather than an income one, with most of the spare cash returned through a share buyback.

Key Risks

Three risks bear watching. The first is United States trade policy, where new tariffs on imported devices could raise costs, although ResMed has been diversifying its manufacturing base for several years. The second is United States reimbursement, where any tightening of the rules around sleep tests or initial therapy approval could slow new patient starts, even though most policy changes over the past 18 months have gone the other way. The third is therapy compliance, which is the channel through which a genuine GLP-1 effect would eventually show up. The data is not showing it yet, but the next few quarterly updates are the most important compliance reads of the cycle.

Our View

ResMed is one of the cleanest defensive growth franchises on the ASX. The patient-flow data continues to undercut the GLP-1 fear, the Philips re-entry is well understood and already priced, and the new growth levers across ventilation, restless legs, travel devices and overseas diagnostics are only now beginning to contribute. At a discount to its medtech and ASX healthcare peers, with a net cash balance sheet and mid-teens earnings growth, the risk and reward is skewed upward. We are comfortable with the Buy view and the A$46.70 price target.

If you would like to discuss ResMed or how healthcare and medtech stocks fit within your portfolio, request a callback or call us on 1300 889 603. The above is general advice and does not consider your individual circumstances. Past performance is not a reliable indicator of future returns.