Collins Foods, the largest KFC franchisee in Australia, heads into its 30 June 2026 full-year result facing a clear two-sided story. On one side, rising minimum and youth wages are set to weigh on KFC Australia margins over the medium term. On the other, the company’s heavy concentration in Queensland and Western Australia leaves it exposed to the two strongest state economies in the country, and a near-complete rollout of self-service kiosks gives management a real lever to offset labour costs. Institutional sell-side research has the stock rated Buy with a 12-month price target of A$10.70, implying approximately 29% upside from the recent close of A$8.27. The thesis rests on a value-led brand trading at a discount to its own history, supported by favourable state demographics and a credible cost-mitigation pathway, against a backdrop of softening same-store sales and wage-driven margin pressure that the market has arguably already priced in.

Research published 10 June 2026. Price target and upside based on prices at time of publication.

About Collins Foods

Collins Foods Limited is an Australian-headquartered quick-service restaurant operator and the country’s largest KFC franchisee. The company runs KFC restaurants across Australia and continental Europe (the Netherlands and Germany), operates the Taco Bell brand in Australia, and reports on an April fiscal year-end. Its network is heavily weighted toward Queensland and Western Australia, where it holds a long-established footprint. Collins is listed on the Australian Securities Exchange with a market capitalisation of approximately A$975 million. Most recent results, investor presentations and ASX announcements are available on the company’s investor relations page. The next scheduled catalyst is the FY26 full-year result on 30 June 2026.

Queensland and WA Exposure Is the Structural Positive

The single most distinctive feature of the Collins investment case is where its restaurants are. More than 80% of the KFC Australia network sits in Queensland and Western Australia, and those two states are running ahead of the national average on the metrics that matter for discretionary fast-food spend. The consumer backdrop nationally remains challenging, with cost-of-living pressure still squeezing household budgets, but the relative position of Collins’ core states cushions the impact.

Three forces support the Queensland and WA consumer. Dwelling prices in Brisbane and Perth have risen approximately 18% and 26% respectively over the past 12 months, and the wealth effect from rising home values typically flows through to discretionary spending, including the value-led restaurant occasions Collins serves. Population growth in Queensland and Western Australia is running at roughly 1.8% and 2.2% per year against 1.3% nationally, which directly expands the customer base for a network already concentrated there. And Queensland is on the cusp of an infrastructure investment cycle as preparations for the 2032 Brisbane Olympics begin, which supports hospitality and out-of-home spending across the state over a multi-year horizon. None of these is a near-term earnings catalyst on its own, but together they tilt the odds in Collins’ favour relative to a peer with a Sydney or Melbourne-weighted footprint.

Wage Costs Are the Real Headwind

The offsetting concern is labour. Employee costs represent roughly 30% of store-level costs for a KFC restaurant, second only to poultry at around 35%, so wage inflation feeds directly into the margin. A recently announced 4.75% minimum wage increase, layered on top of a multi-year phase-in of higher youth wage rates for 18 to 20 year-old workers, raises the cost base across the quick-service industry over the medium term. The result is that KFC Australia’s EBITDA margin is forecast to compress by approximately 35 basis points in FY27, with no margin expansion assumed thereafter.

The mitigating point is that this is an industry-wide pressure, not a Collins-specific problem. The same wage increases hit every major quick-service operator, which makes it more likely that the cost is partly passed through in menu pricing across the category. Historical analysis of California’s US$20 fast-food minimum wage provides a useful template. There, an 8% wage increase led to industry employment declining 2.3% to 3.9% and prices rising 3.3% to 3.6%, largely offsetting the original wage increase at the operator level. The read-through is that Collins can recover a meaningful share of the wage headwind through below-CPI price increases (appropriate for a value-focused customer) and reduced labour hours, even if the net outcome remains uncertain. Top-line growth is also expected to slow, with KFC Australia same-store sales growth forecast to decelerate from around 2.6% in FY26 to roughly 1.5% in FY27 as the consumer environment softens.

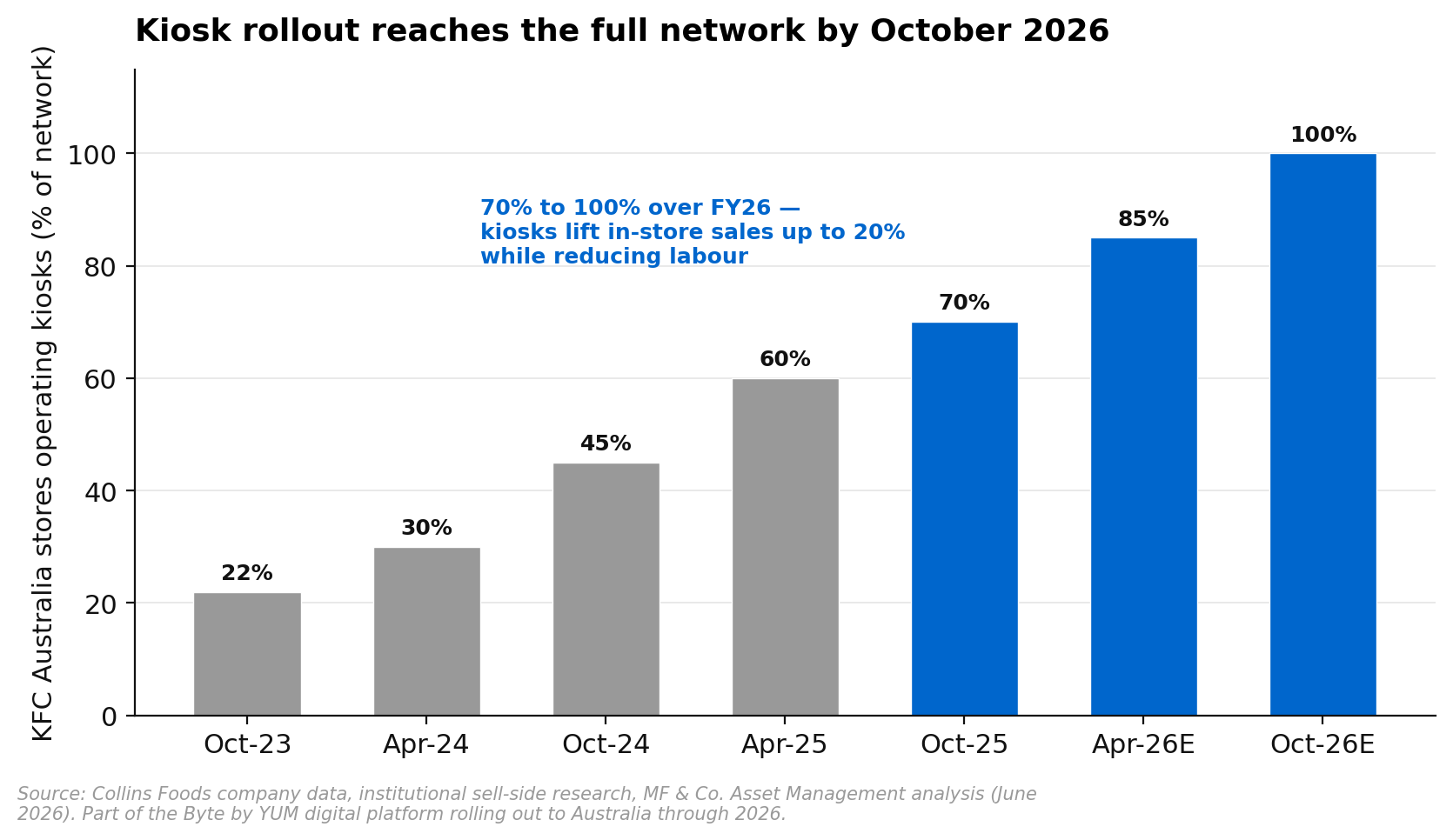

Kiosks and Digital Are the Margin Mitigation Lever

The most tangible offset to the wage squeeze is the kiosk and digital rollout. Collins expects to have 100% of its KFC Australia stores operating self-service kiosks by October 2026, up from 70% in October 2025. Kiosks typically lift in-store sales by up to 20% while simultaneously reducing front-counter labour, which makes them a direct two-way lever on the exact margin pressure the wage increases create.

The kiosk rollout sits inside the broader Byte by YUM digital platform, which is accelerating its expansion into Australia through 2026 with the stated goal of unifying and digitising restaurant operations. Early outcomes from the platform have been encouraging, including a meaningful reduction in aggregator ordering failure rates, a lift in consumer satisfaction, and a sharp reduction in stock-outs, all of which support sales conversion and restaurant efficiency. Digital sales penetration in KFC Australia has been climbing steadily and still sits below the global KFC benchmark, leaving further runway. The investment question is execution: if the kiosk and digital programme delivers the labour savings and sales uplift management expects, it can hold the margin broadly flat against the wage headwind. If it slips, the margin compression narrative dominates and the earnings trajectory flattens.

Valuation: A Quality Value Brand at a Discount

Collins trades at a discount to both its own history and the broader market. The stock sits at roughly a 20% discount to its historical next-twelve-month price-to-earnings multiple, and around 14% below the broader Small Ordinaries on the same basis. For a business with a defensive, value-led brand, a defensible franchise position, and exposure to the strongest state economies in the country, that discount looks more like cyclical caution being priced in than a structural derating.

The 12-month price target of A$10.70 was reduced from A$12.30 in the most recent update, reflecting earnings forecast cuts of approximately 0%, 10% and 12% to FY26, FY27 and FY28 respectively as the wage and consumer headwinds were incorporated. Even after that reduction, the target still implies approximately 29% upside from the recent close of A$8.27. The dividend adds a modest cash return on top, with a forecast yield stepping from roughly 3.1% toward 3.5% over the forecast horizon. The asymmetry looks favourable: the market is paying a discounted multiple for a business whose principal risk, wage inflation, is industry-wide and partially self-correcting through pricing, while the company-specific positives of state exposure and the kiosk rollout are not yet reflected in the multiple.

Key Risks

The primary risk is a sharper-than-expected deterioration in the Australian consumer that pushes same-store sales growth below the forecast trajectory, which would compound the wage pressure rather than offset it. A second risk is execution on the kiosk and digital rollout; if the labour savings and sales uplift fail to materialise at the promised scale, the margin compression narrative dominates. Wage costs themselves are the third risk, further increases beyond the announced schedule, or an inability to pass them through in menu pricing given the value-focused customer, would erode margins more than forecast. Finally, the European business (KFC Netherlands and Germany) carries its own competitive and consumer dynamics that can introduce earnings volatility independent of the Australian story. Fuel-price volatility, which affects both consumer discretionary budgets and delivery economics, is a secondary swing factor on near-term traffic.

If you would like to discuss Collins Foods or how ASX-listed consumer names might fit within your portfolio, request a callback or call us on 1300 889 603. The above is general advice and does not consider your individual circumstances. Past performance is not a reliable indicator of future returns.