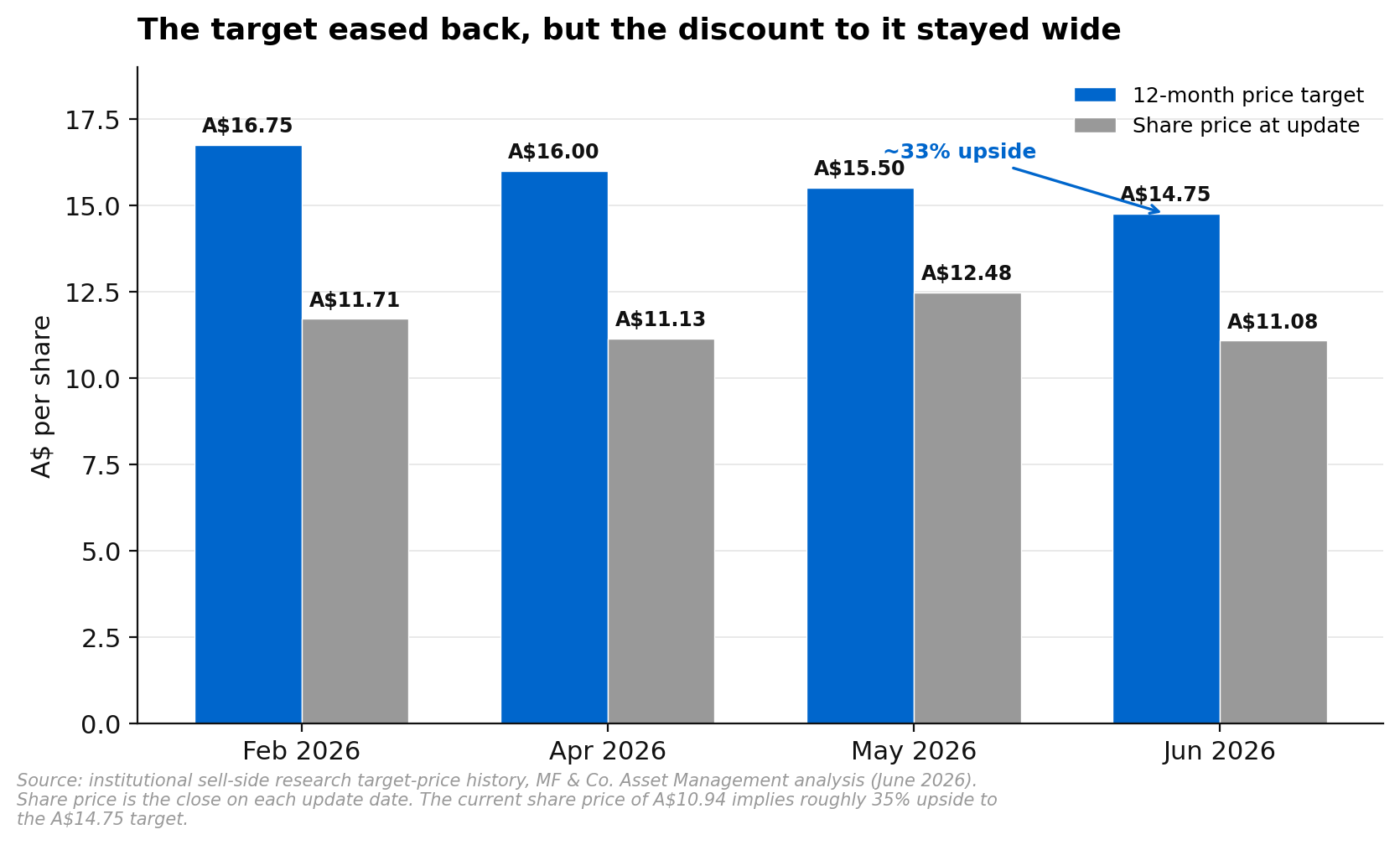

Worley has sold off through June, and we think the market has overreacted to what is a modest revision. The conflict in the Middle East has disrupted project activity in the region and forced a further, shallow trim to the company’s near-term earnings, but the share price has fallen by more than the cut to fair value. We are reiterating our Buy view. Institutional sell-side research has the stock rated Buy with a 12-month price target of A$14.75, implying roughly 35 per cent upside from the recent close of A$10.94. The structural growth case that underpins the stock has not changed, the earnings trim is small in the scheme of the multi-year story, and the fall in the share price has lifted the forecast dividend yield to a level that pays investors to wait.

Research published 30 June 2026. Price target and upside based on prices at time of publication.

About Worley

Worley Limited is an Australian-headquartered global professional services company providing engineering, procurement and construction services to the energy, chemicals and resources sectors. The company employs around 50,000 people across 50 countries, with deep capability in upstream and downstream oil and gas, refining, petrochemicals, mining and minerals processing, and a rapidly growing energy transition footprint covering hydrogen, carbon capture, ammonia, biofuels and grid infrastructure. Worley is listed on the Australian Securities Exchange with a market capitalisation of approximately A$5.8 billion and reports in Australian dollars on a 30 June fiscal year. Most recent results, investor presentations and the May 2026 Investor Day deck are available on the company’s investor relations page.

The Middle East Earnings Trim Is Real But Modest

The latest data update trims Worley’s underlying EBITA by roughly 3 to 4 per cent in each of FY26, FY27 and FY28 to reflect the further adverse impact of the Middle East conflict on project activity in the region. The FY26 underlying EBITA margin, before procurement, is now seen at around 9.1 per cent, the low end of the company’s 9 to 9.5 per cent guidance range. Revenue forecasts come down to roughly A$11.7 billion in FY26, A$12.6 billion in FY27 and A$13.7 billion in FY28, with earnings per share trimming to around A$0.74, A$0.87 and A$1.01 across the three years. None of this changes the shape of the business. It is a near-term timing and disruption effect rather than a structural downgrade.

The key point is the mismatch between the cut to fair value and the fall in the share price. The 12-month target eases to A$14.75 from A$15.50, a reduction of about 5 per cent, while the share price has fallen by close to 10 per cent over the same window. The conflict is also double-edged. The same disruption that is denting one year of regional project earnings is the kind of event that seeds a multi-year reconstruction opportunity once it subsides, given the engineering and construction work that follows damage to refineries, gas facilities and terminals. We would not pay up for that optionality today, but it sits on the other side of the ledger from the near-term trim.

The Structural Growth Case Has Not Changed

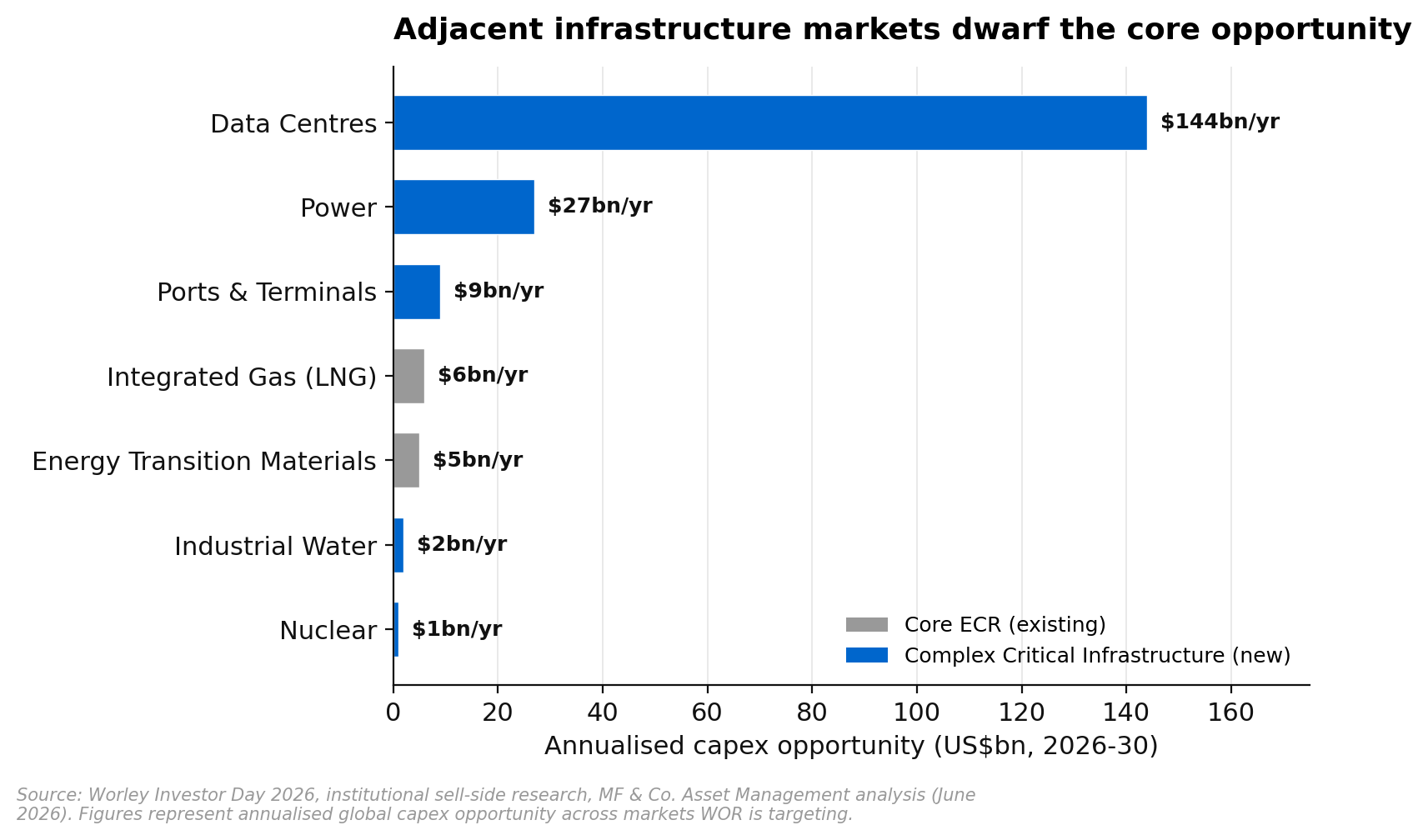

The reason to own Worley was never the next 12 months of regional project work. It is the repositioning of the business into much larger adjacent end-markets, and that opportunity set is untouched by a regional conflict that dents a single year of earnings. Worley is pointing the same engineering and project-delivery capability that built its core energy, chemicals and resources franchise at large-scale power, data centres, nuclear, industrial water, and ports and terminals. These segments share the same complex-delivery characteristics as the existing portfolio, with long lead times, multi-disciplinary engineering, and clients who value execution certainty over price.

Data centres are the standout. Global data centre electricity demand is forecast to grow sharply by 2030 as artificial intelligence workloads make power, rather than chips or floor space, the binding constraint on deployment. That demand pulls through into new generation capacity, grid upgrades, cooling infrastructure and the facilities themselves. United States power demand is forecast to step up to its fastest growth in more than 20 years, and nuclear investment has re-accelerated after years of stagnation. Worley is not pivoting into something it does not know how to do. It is aiming existing capability at far larger pools of capital expenditure.

Margins and the Cost-Out Programme Still Do the Work

Pushing further into construction and procurement expands the revenue pool Worley can compete for on every project, but it dilutes group margin in isolation, because construction and procurement carry lower margins than the engineering-led professional services that dominate the business today. The bridge that closes the gap is the A$125 million cost-out programme, which is sized to neutralise that dilution and hold the group margin broadly flat on a much larger revenue base. The latest guide of around 9.1 per cent for FY26 sits at the low end of the 9 to 9.5 per cent range, which tells you the conflict has nudged the near-term margin without derailing the cost programme.

The investor question is execution. If Worley delivers the cost-out as promised, it runs a roughly flat margin on a growing revenue base, which is absolute earnings growth. If the cost-out slips or the mix-shift runs ahead of what the programme can absorb, the growth narrative becomes a revenue story rather than an earnings one. Execution is the swing factor, and the track record on the cost programme is the thing to watch over the next few results.

A Rising Yield Now Pays You to Wait

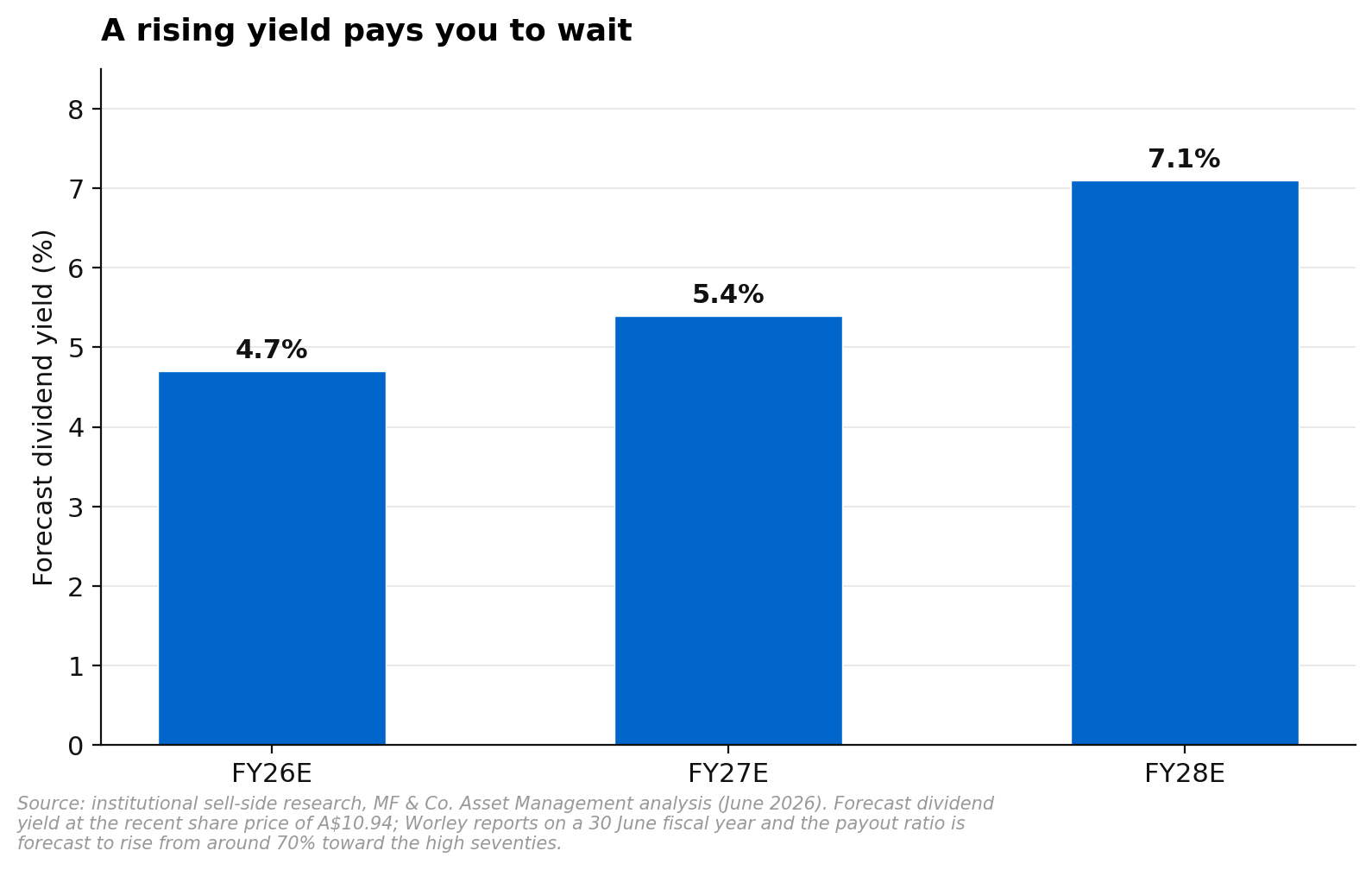

One consequence of the lower share price is that the forecast dividend yield steps up to an unusually high level for a company that still has a credible multi-year growth story in front of it. The institutional model has the yield rising from about 4.7 per cent in FY26 to 5.4 per cent in FY27 and 7.1 per cent in FY28, as earnings grow and the payout ratio rises from around 70 per cent toward the high seventies. That is a meaningful cash return paid while the wider-and-deeper strategy plays out, and it lowers the cost of being patient through the current soft patch.

Valuation and Why the Selloff Overshot

Worley now trades at around 10 times next-twelve-months EV/EBIT, a wider discount to both its own multi-year history and its global engineering and construction peers than before the June selloff. On forecast earnings the stock is on about 14.9 times FY26, falling to 12.7 times FY27 and 10.9 times FY28 as earnings grow, so the multiple de-rates toward 11 times simply by holding the price still and letting earnings build. The 12-month target of A$14.75 is built on a blend, half from a discounted cash flow valuation using a 9.6 per cent discount rate and a 2.5 per cent terminal growth rate, and half from an EV/EBIT framework applied at 11.8 times next-twelve-months EBIT. That target does not require the multiple to expand to a heroic level to be reached.

The clearest way to see the overshoot is to track the target against the price. Over the past four updates the institutional target has come down gently, from A$16.75 in February to A$16.00 in April, A$15.50 in May and A$14.75 now, as the macro and conflict backdrop has bitten. The share price, though, has stayed depressed throughout, so the gap between price and target has stayed wide rather than closing. At the recent close that gap is worth roughly 35 per cent.

Risks to the Buy Call

The institutional risk framework identifies three primary risks. Project delays in client work can push revenue recognition into later periods and create lumpy quarterly outcomes, and the Middle East disruption behind this trim is a live example of exactly that. Lower-than-expected bookings or aggregated revenue would compress the growth trajectory the strategy depends on. And changes in the margin profile, particularly any sign that the cost-out programme is not delivering at the promised quantum, would re-open the question of whether the mix-shift erodes group margins over a multi-year view. We would add a fourth, which is execution capability. Moving from engineering-led to full lifecycle delivery means competing for construction and procurement mandates against incumbents who have done it for decades, and the early wins in the new addressable markets are the leading indicator the market is watching.

Our View

The June selloff has taken Worley down by more than the cut to its fair value, and that mismatch is the kind of thing that creates an entry point. The earnings trim is a near-term disruption effect from the Middle East, not a structural downgrade, and the wider-and-deeper growth strategy that is the actual reason to own the stock is untouched by it. With the shares at around 10 times forward EV/EBIT, a forecast dividend yield rising toward the high single digits, and roughly 35 per cent upside to a target that has only eased modestly, we are comfortable reiterating the Buy view. The downside case is that the cost-out slips and the margin story turns into a multi-year compression, in which case the yield becomes the principal support for the price. On balance we think the risk and reward has improved, not worsened, after the selloff.

If you would like to discuss Worley or how ASX-listed industrials might fit within your portfolio, request a callback or call us on 1300 889 603. The above is general advice and does not consider your individual circumstances. Past performance is not a reliable indicator of future returns.