Tesla (NASDAQ: TSLA) A Strong Q1 But No Free Cash Flow Until 2028

Tesla just delivered a first quarter result that was stronger than the market expected, with revenue beating the Street, automotive gross margins running well ahead of forecast, and energy storage producing the highest margin in the business. On the surface it looks like a turning point. Look one layer down and a different story emerges. A meaningful share of the margin beat came from one off accounting and tariff related tailwinds that are unlikely to repeat. At the same time the company has lifted its 2026 capex guide to more than US$25 billion, and free cash flow is now expected to be negative across both 2026 and 2027, with the company not returning to positive cash generation until 2028. We initiate coverage of Tesla with a Hold rating and a 12-month price target of US$375, against a share price of US$387.51 at the time of publication, implying 3.2% downside.

Research published 29 April 2026. Price target and upside based on prices at time of publication.

Table of Contents

- 1 About Tesla

- 2 The Q1 Print Was Stronger Than the Market Expected

- 3 The Margin Beat Had Two Real but Temporary Tailwinds

- 4 Capex Has Been Lifted Again and Free Cash Flow is Negative for Two More Years

- 5 Robotaxi is Ramping but Will Not Move the 2026 Result

- 6 The FSD Subscription Story is the Genuine Bull Case

- 7 Valuation and Price Target

- 8 Risks to Consider

- 9 Our View

- 10 Financial Summary

About Tesla

Tesla, Inc. (NASDAQ: TSLA) is a vertically integrated maker of electric vehicles, battery energy storage products, solar generation systems and increasingly artificial intelligence and robotics platforms. The company operates four primary segments. Automotive includes the Model 3, Y, S, X and Cybertruck, with the higher volume Model 3 and Y currently accounting for roughly 95% of vehicle deliveries. Energy generation and storage covers the Powerwall residential battery, Megapack utility scale storage and solar products. Service and other includes used vehicle sales, parts, after sales servicing, supercharging and insurance. The company also runs a research effort spanning the Optimus humanoid robot, the Cybercab autonomous taxi and the Dojo and Cortex AI training infrastructure.

Tesla has a market capitalisation of approximately US$1.4 trillion and an enterprise value of US$1.4 trillion. The company produced more than 408,000 vehicles in the first quarter of 2026 and delivered around 358,000, with the global fleet now exceeding 7 million vehicles. Headquartered in Austin, Texas, Tesla operates production facilities in Fremont, Shanghai, Berlin, Texas and Nevada and is currently expanding battery and Optimus capacity across multiple sites.

The Q1 Print Was Stronger Than the Market Expected

Tesla reported first quarter revenue of US$22.4 billion, up 16% year on year and ahead of consensus estimates that were sitting closer to US$21.2 billion. The headline beat was driven by a stronger automotive line, with auto revenue of US$16.2 billion well above the Street, and a sharply better than expected energy generation and storage segment that delivered 39.5% gross margin against expectations closer to 25%. Earnings per share on a non GAAP basis came in at US$0.41, almost double consensus near US$0.22.

The breakdown across segments was telling. Energy storage was the highest margin business in the quarter, even after stripping out the temporary tailwinds discussed below. Service and other revenue grew 42% year on year as the global supercharger network and the in-house insurance offering continued to scale. Total deliveries of 358,000 vehicles were down 14% sequentially but up 6% year on year, with regulatory credit revenue of about US$380 million, lower than recent quarters but still a meaningful contributor to operating income.

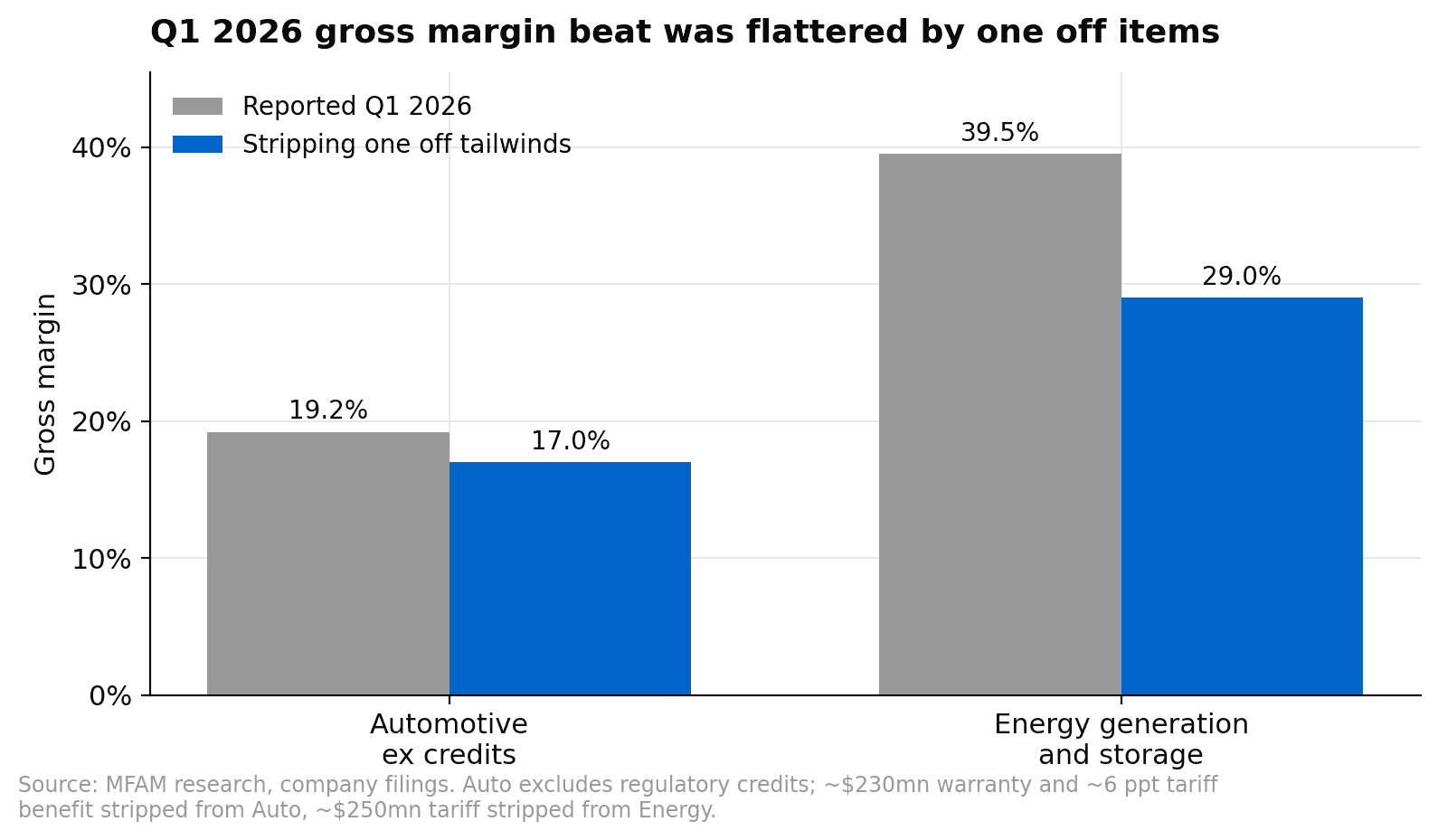

The Margin Beat Had Two Real but Temporary Tailwinds

The reported automotive gross margin excluding regulatory credits printed at 19.2%, well ahead of the 15 to 16% range the market had been modelling. That number is real but it is also flattered. Approximately US$230 million of the beat came from a one off favourable warranty accounting adjustment, and roughly 6% of the margin reflected tariff related benefits that the company itself has not described as recurring. Stripping out both, the underlying automotive gross margin was closer to 17%, still ahead of consensus but a much narrower beat than the headline suggests.

The energy gross margin tells a similar story. Reported at 39.5%, the segment benefited from more than US$250 million of one off tariff related tailwinds. Excluding these, the underlying margin was closer to 29%. Management has also flagged that normalised energy gross margins are expected to compress from here, driven by ongoing competitive pressure, cost inflation and tariff related cost pass through. The first quarter result is unlikely to be the new run rate for either segment.

This matters because the multiple investors are paying for Tesla today already assumes margins step higher from here, not lower. If the underlying numbers are closer to 17% in autos and 29% in energy rather than the headline figures, the case for re-rating from current levels weakens.

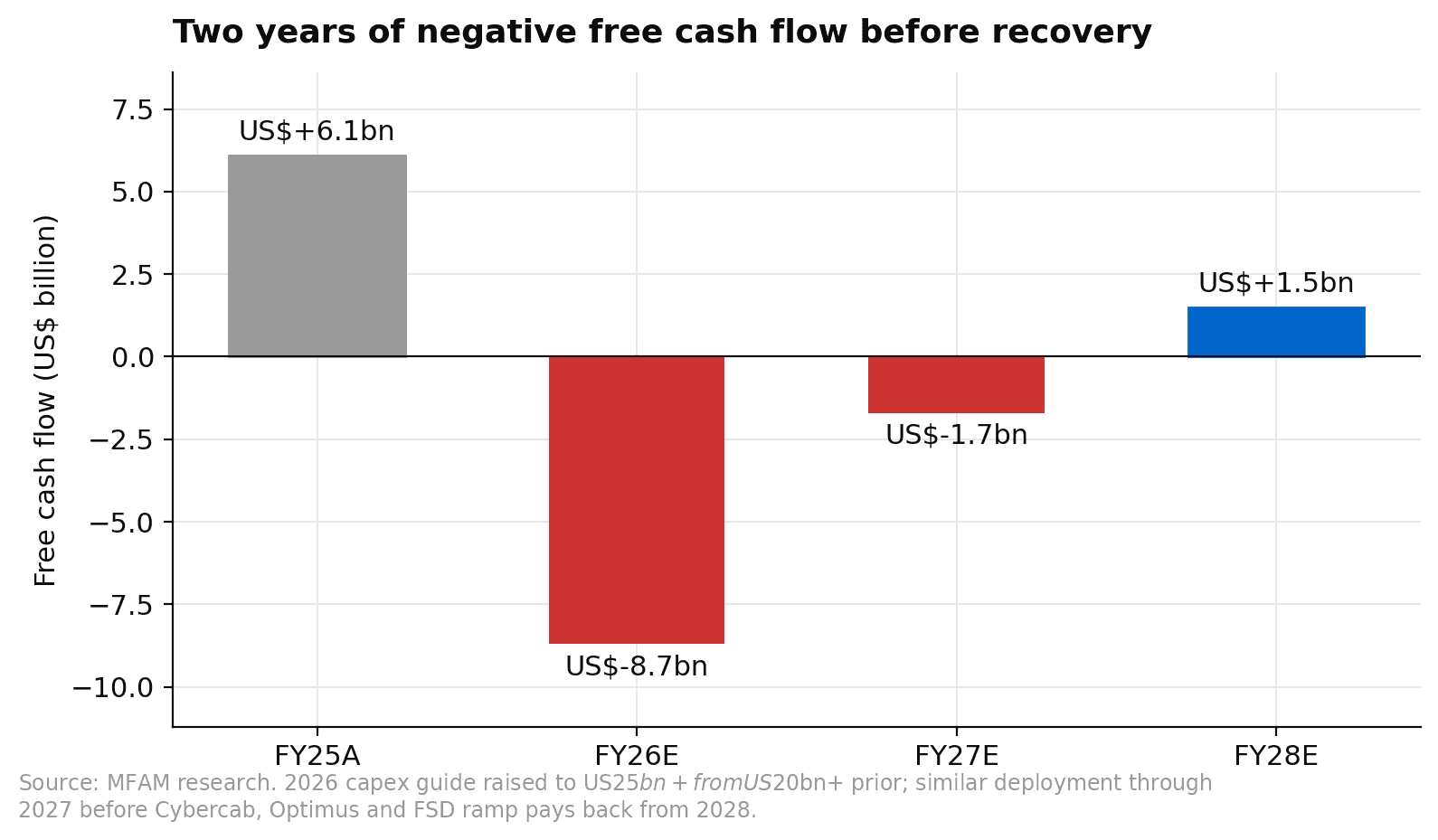

Capex Has Been Lifted Again and Free Cash Flow is Negative for Two More Years

The most consequential update from the quarter was a fresh capex revision. Tesla now expects to spend more than US$25 billion on capital expenditure in 2026, up from prior guidance of more than US$20 billion. The increase is being directed into Cybercab and Semi production capacity, the Texas Megafactory ramp, additional capacity at existing factories ahead of the Model Y L launch in China, an Optimus production line, and a new internal research fabrication facility expected to cost around US$3 billion.

The cash flow consequences are significant. Free cash flow is now expected to be negative for the remainder of 2026 and across the whole of 2027, with the company not expected to return to positive free cash flow generation until 2028. That is a two year window in which Tesla is consuming cash to build out next generation products before any of those products are contributing meaningfully to earnings. For shareholders the question is straightforward. Are you comfortable underwriting two years of negative cash generation in exchange for the optionality on Cybercab, Optimus and FSD landing on time and at scale?

For long term holders with a high conviction view on autonomy and humanoid robotics, the answer may be yes. For investors looking at the next twelve to eighteen months on a fundamentals basis, the cash flow gap removes one of the supports that has historically helped the stock through periods of slower growth. Cash on the balance sheet is healthy at around US$45 billion, so funding is not the issue. The issue is that the period over which capital is being deployed without earnings to match has just been extended.

Robotaxi is Ramping but Will Not Move the 2026 Result

Tesla has begun running unsupervised robotaxi operations in Dallas and Houston, expanded the Austin service area, and is operating with a safety driver in the San Francisco Bay Area. Total paid robotaxi miles reached approximately 1.7 million as of March 2026, up from around 650,000 at the end of December 2025. The pace of expansion is genuinely impressive on a percentage basis, and there have been no reported safety incidents from robotaxi operations in February or March, which is a meaningful operational improvement.

The challenge is timing. Tesla has indicated that the broader rollout of unsupervised FSD to consumers could now stretch into late 2026, with regulatory approval, capability finalisation and operational readiness all working in parallel. The company has explicitly said robotaxi and unsupervised FSD revenue will not be material to 2026 results. The implication is that the autonomy ramp is real, the data is improving, but it does not reset 2026 earnings expectations and the bull case for the stock requires the next two years to validate the trajectory rather than monetise it.

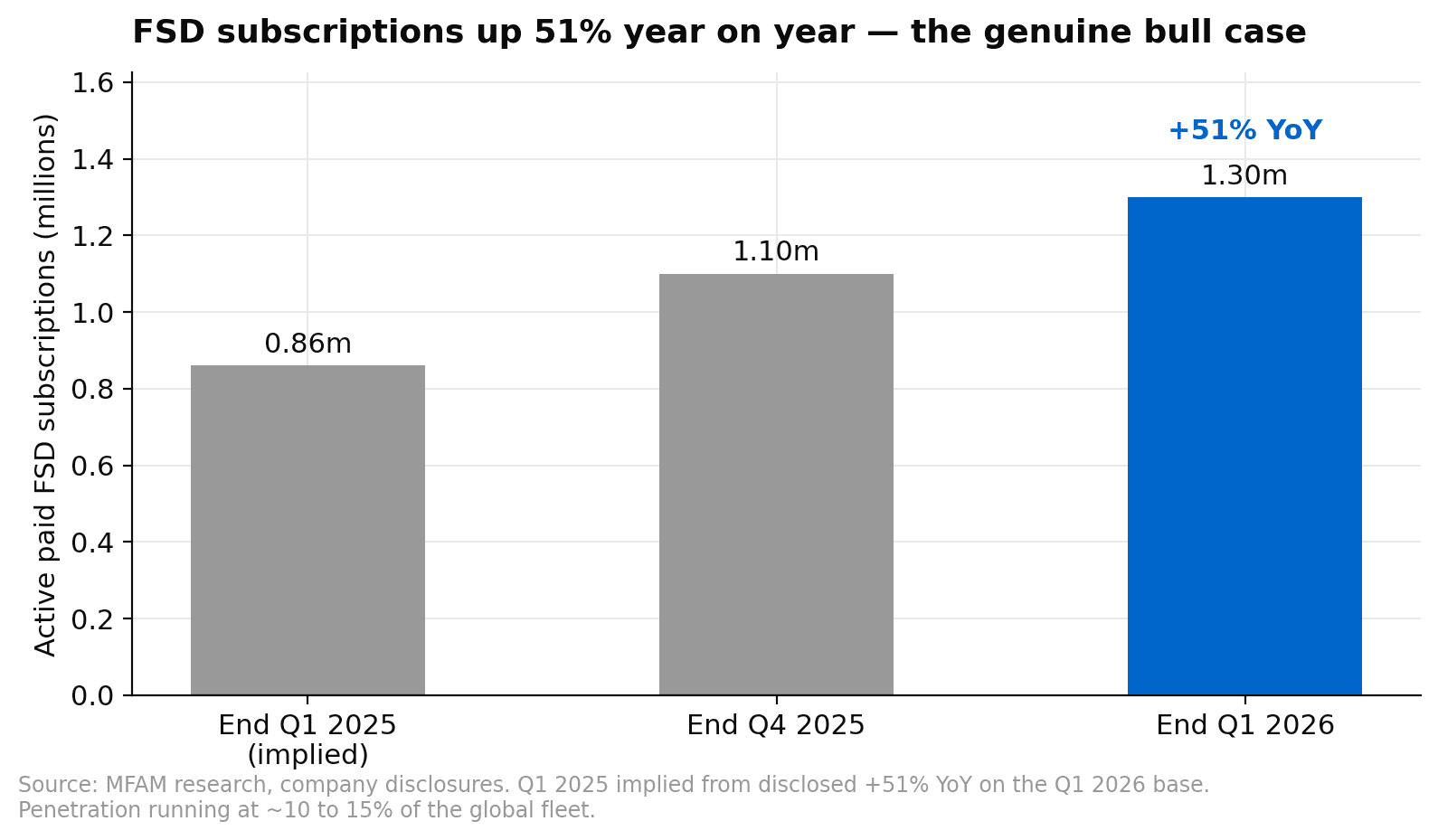

The FSD Subscription Story is the Genuine Bull Case

The most underappreciated data point in the quarter was the progress on supervised FSD subscriptions. Total active paid FSD subscriptions reached approximately 1.3 million at the end of the first quarter, up from 1.1 million at the end of the previous quarter and up more than 50% year on year. Penetration is now running at roughly 10 to 15% of the global fleet, with strong attachment rates on new vehicle purchases and an upfront purchase share that has continued to grow through the period.

This matters for two reasons. First, FSD subscription revenue is high gross margin software revenue layered onto an existing vehicle fleet, with limited incremental cost to serve. Second, it is the leading indicator of whether the autonomy investment is translating into willingness to pay. A subscriber base growing at 50% plus on a fleet of more than seven million vehicles is the data point that supports the long term bull thesis better than any of the robotaxi mileage numbers. If FSD penetration continues to trend higher, the multiple the market pays for Tesla will likely follow.

Valuation and Price Target

Our 12-month price target is US$375, against a current share price of US$387.51, implying 3.2% downside. The price target is derived by applying a multiple well above the long run market average to out year earnings per share, reflecting the optionality value of FSD, robotaxi and Optimus combined with the strength of the core automotive franchise and the energy storage business. Even on these generous valuation assumptions, the stock is currently trading slightly ahead of where the math takes us.

It is worth putting the share price action in context. Tesla is up roughly 63% over the past twelve months but down close to 14% over the past three months, with the broader S&P 500 up around 21% and 2% over the same windows respectively. The recent weakness reflects exactly the issues outlined above. The stock has front run the autonomy thesis, the cash flow profile has deteriorated, and even after the Q1 beat the market is still grappling with what to pay for a business that is asking for two more years of patience.

Our non GAAP earnings estimates excluding stock based compensation now sit at US$2.10 for 2026, US$3.11 for 2027 and US$3.50 for 2028, reflecting higher revenue assumptions, better automotive gross margins and a reduction in stock based compensation expense. Importantly, the 2026 number remains well below where the multiple is pointed, meaning the bulk of the value the market is pricing in lives in the 2027 and 2028 years and beyond.

Risks to Consider

The downside risks to our view are larger vehicle price reductions than we currently expect, a step up in EV competition particularly from China and US incumbents, delays to FSD and robotaxi capability or rollout, key person and governance risks, internal control concerns, further margin compression in either autos or energy storage, and operational risks associated with the high degree of vertical integration.

The upside risks include faster than expected EV adoption or share gain by Tesla, a stronger global macroeconomic environment for new vehicle sales, earlier or larger than anticipated launches of new vehicle products, a stronger contribution from AI enabled products including FSD, Optimus and robotaxis, and a smaller than expected tariff impact on costs.

Our View

Tesla is a high quality business with genuine optionality on FSD, robotaxi and Optimus, and the Q1 print confirmed that the core automotive and energy storage franchises are operationally in good shape. But the headline margin beat was flattered by one off accounting and tariff tailwinds, the capex bill has just been lifted by another US$5 billion, and shareholders are now being asked to underwrite two full years of negative free cash flow before the autonomy and Optimus investments begin to pay back. With the stock already trading above where the out year earnings math supports it, and with the recent three month price action suggesting the market is starting to grapple with the same issues, we think the right call is patience. We initiate coverage of Tesla with a Hold rating and a 12-month price target of US$375.

If you would like to discuss whether Tesla fits in your portfolio, or how the broader AI and autonomy thematic might be positioned alongside your existing Australian holdings, request a callback or call us on 1300 889 603.