Last updated: 1 May 2026. Region outlook refreshed when new sell-side notes or material market moves warrant, not on a fixed cadence.

Table of Contents

- 1 About the Chinese Economy

- 2 The Stability Premium

- 3 Growth Is Holding Above the Floor

- 4 Inflation Is Reflating Off the Floor

- 5 The Currency Has Turned

- 6 Tech, AI, and the Self-Reliance Dividend

- 7 Property and the Local Government Backstop

- 8 Tools for China Exposure

- 9 Catalysts to Watch

- 10 Key Risks

- 11 Where We Land

- 12 ETF Universe

- 13 References

China has spent the last three years as the asset that everyone sized down. The property bust was deep, deflation lingered, the renminbi weakened, and the official growth target started to look like a stretch goal rather than a floor. Through the first half of 2026, that picture has quietly inverted. Growth is holding above the 4.5% line, factory-gate prices have crossed back above zero, the currency has rolled lower in dollar terms, and the equity wrappers have led the rally off the 2024 lows. The shorthand for what is going on is a stability premium. After years of being priced for a slow-motion accident, China is now being priced for a country that is muddling through and, in places, growing again.

This piece walks through the macro setup, the policy mix that is doing the work, where the cycle is in inflation and the currency, what is happening underneath the headline indices, and how a retail investor in Australia or the United States can take exposure if the through-line resonates.

About the Chinese Economy

China is the second-largest economy in the world, with nominal GDP around USD 18.5 trillion and a population of 1.4 billion. The economy runs on three big legs. The first is industrial production and manufacturing, where China remains the workshop of the world and is the dominant exporter of steel, machinery, electronics, EVs, batteries, and solar panels. The second is fixed-asset investment, traditionally led by residential property and infrastructure, with the property leg now in structural decline and infrastructure being substituted in. The third is consumption, which has been the policy target for a decade and is finally starting to pull more weight as services and durable goods recover.

The official growth target sits around 5%. The currency is the renminbi, managed within a band against a basket but in practice highly sensitive to the USD/CNY cross. Monetary policy is run by the People’s Bank of China, fiscal policy is run through a combination of central government issuance and local government financing vehicles, and the regulatory environment is shaped by a five-year planning cycle anchored around self-reliance in technology, energy, and food.

The cleanest way to summarise where China is in 2026 is that the worst-case fears of 2023 and 2024 have not materialised. Property has not collapsed into a Lehman moment, deflation has not dug in, the renminbi has not been forced to break a band, and growth has not slowed to the 3% range that some bears were pricing. Each of those tail risks has been priced out incrementally over the last twelve months, and the equity rerating reflects that.

The policy mix that has done the work is not flashy. There has been no big bazooka, no PBOC rate cut, no aggressive stimulus headline. Instead there has been a steady widening of the augmented fiscal deficit, now running close to 12% of GDP, channelled through infrastructure, manufacturing capex, and trade-in programmes for consumer goods. The PBOC has held policy rates steady through the first half of 2026, with consensus building toward no further rate cut this year and the next move likely to be a hike if reflation continues. That is a meaningful inversion of the mood from a year ago, when the market was pricing further easing.

Growth Is Holding Above the Floor

Real GDP growth is tracking around 4.7% on the latest run rate, with consensus sitting near 4.6%. That is below the official 5% target but well above the 3.5%-to-4% range that the bears were modelling. The composition is more important than the headline. Net exports have remained robust because the global capex cycle in semiconductors, AI infrastructure, and renewables runs through Chinese supply chains. Manufacturing investment has continued to grow at double digits in the favoured sectors. Consumption is stabilising, with services running ahead of goods and retail sales pulling out of the late-2024 trough.

The drag is property, and that drag is still there. Residential floor space sold continues to fall year on year, and developer balance sheets are still being worked through. The crucial change is that the rate of decline has slowed and, in tier-one cities, sales are flat to up. Housing is no longer the marginal piece pulling growth lower each quarter, which is why the headline number can hold up even with property still negative.

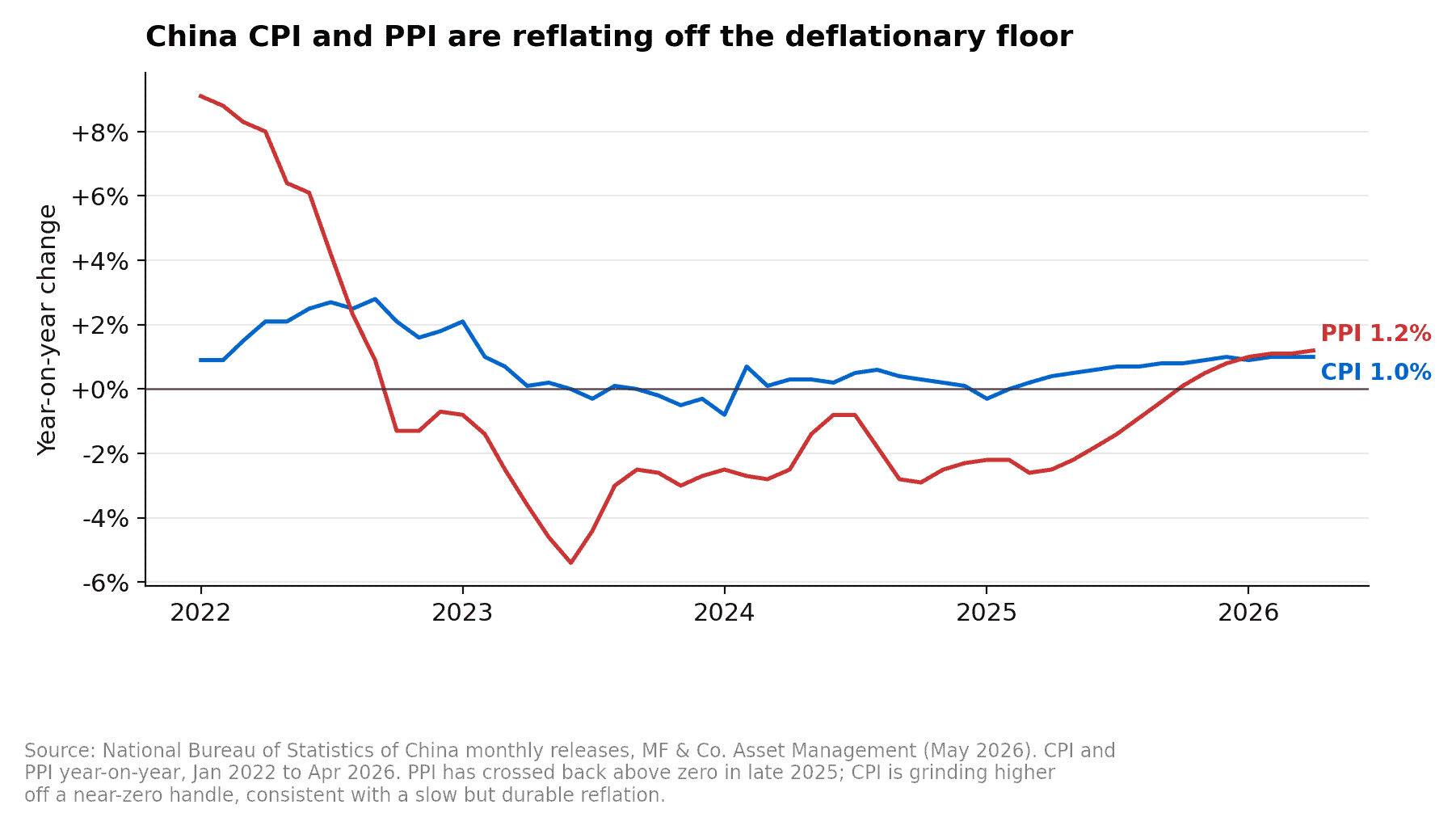

Inflation Is Reflating Off the Floor

The deflation story has quietly broken. CPI bottomed in early 2025 around -0.3% and is now running just above 1%, a slow grind but a clear direction. The bigger move has been in PPI, the producer-price index, which had been negative for more than two years. PPI crossed back above zero in the back half of 2025 and is now running close to 1.2% year on year. That matters because PPI is a leading indicator for industrial profit, for nominal GDP, and for the marginal pricing power of Chinese exporters in global markets.

The driver is partly base effects rolling out, partly the mild reduction in overcapacity in steel and cement as supply has been disciplined, and partly the early-stage pull-through from the manufacturing capex cycle. Consensus is building toward CPI averaging 1% for 2026 and PPI staying mildly positive. That is not a reflation that troubles the central bank, but it is enough to push back the bear case that China is heading toward a Japan-style deflationary trap.

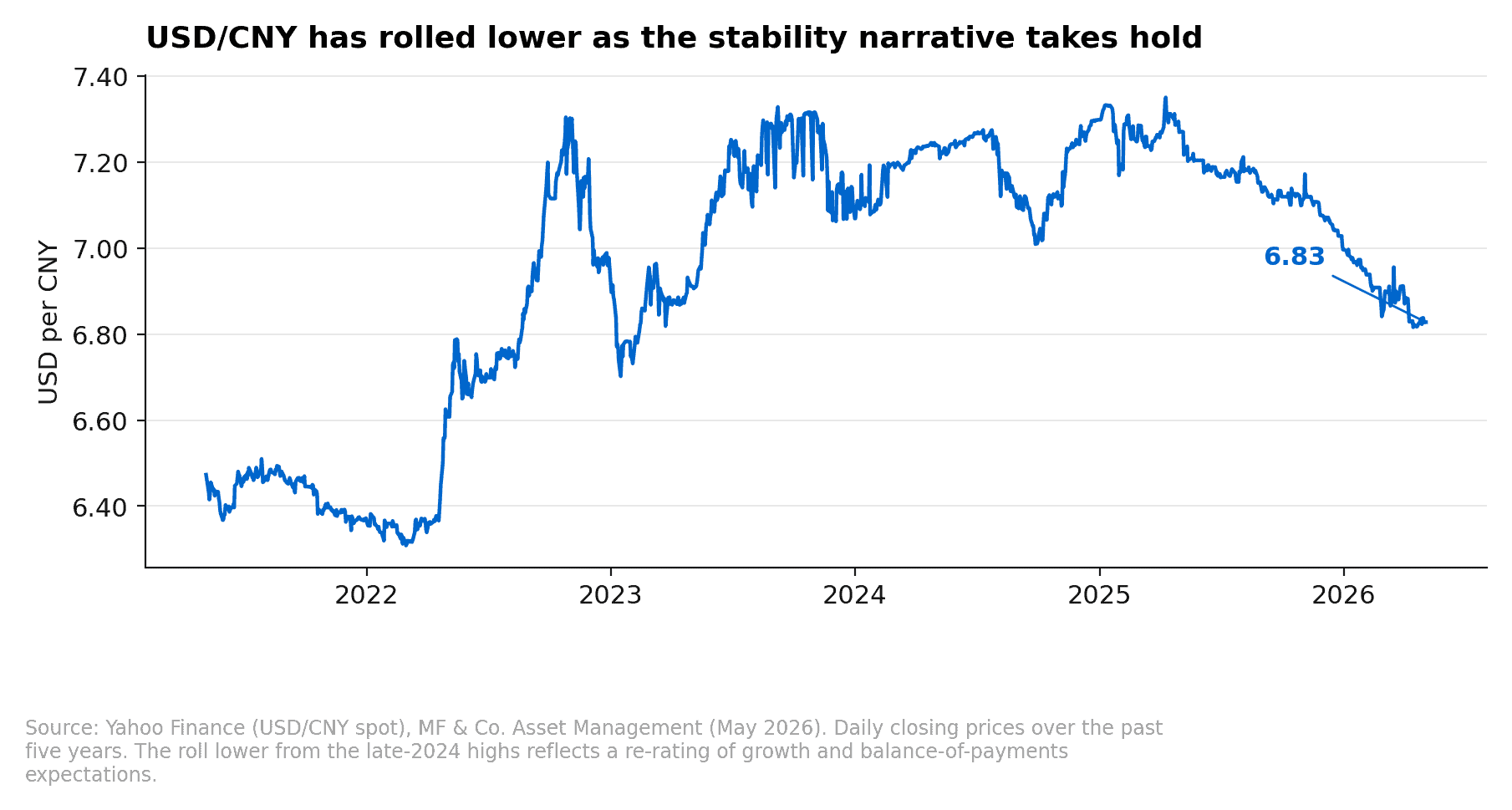

The Currency Has Turned

USD/CNY traded in a narrow range around 7.20 to 7.30 through most of 2024 and 2025, with each test of the upper band met by stepped-up daily fix guidance from the PBOC. Through the first half of 2026 the cross has rolled back through 7.00 and is now trading near 6.83. There is a growing case for a 12-month target near 6.70, which would unwind most of the post-2022 weakness.

The mechanics behind the move are straightforward. China continues to run a goods trade surplus near 5% of GDP, the current account is comfortably positive, and capital outflows have moderated as domestic equity returns improved. The dollar side has helped too. As the Federal Reserve moved toward a less restrictive stance in late 2025 and global growth differentials narrowed, the safe-haven bid for the USD eased. A stable to slightly stronger renminbi flips the script for foreign investors in China, because it removes the FX drag that had eaten into dollar-denominated returns from MCHI and FXI.

Tech, AI, and the Self-Reliance Dividend

The 2026 narrative on China and AI is not the same one global investors were pricing for the United States. China is not racing to commercialise general-purpose foundation models at the same scale. What it is doing is integrating AI horizontally across industrial workflows, robotics, and logistics, while building out the domestic semiconductor stack so that future capacity sits inside the country. The investment case here is less about the next ChatGPT moment and more about productivity gains rolling through manufacturing margins and a structurally larger domestic chip equipment market.

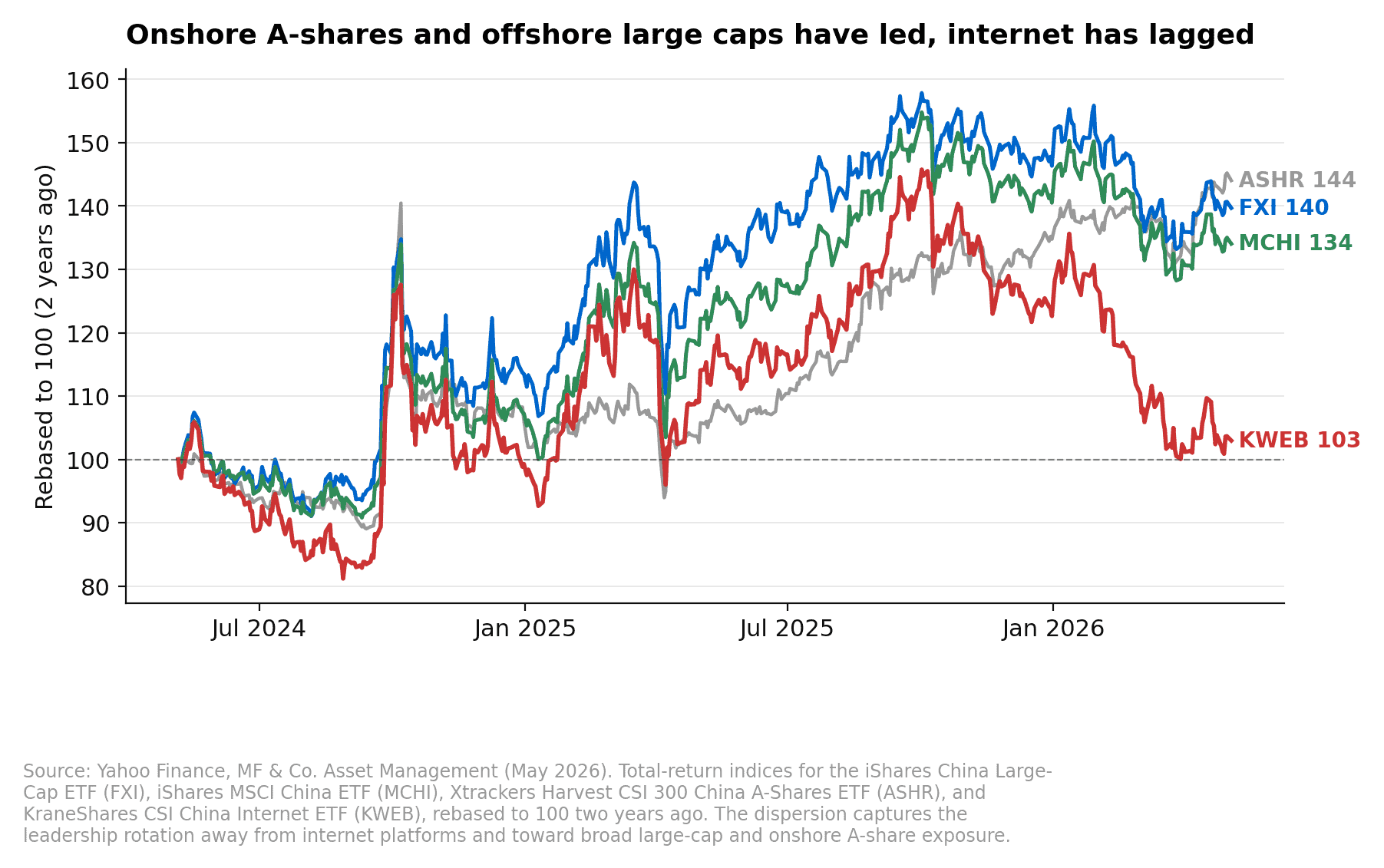

The hyperscaler capex of Alibaba, Tencent, ByteDance, and Baidu has stepped up materially through 2025 and 2026 as each tries to lock in domestic compute supply. That is feeding through to the listed semiconductor names, equipment vendors, and increasingly to the AI-adjacent industrials. The internet platforms themselves have lagged the broader complex because the regulatory overhang from 2021 and 2022 has been slow to lift, but earnings are growing again and ad markets have stabilised. Over a one-to-three-year window, the catch-up trade in offshore platform names is one of the more contrarian setups in the China complex.

Property and the Local Government Backstop

The property cycle remains the swing factor. Our base case is that the worst is behind, but the recovery is uneven and the policy work to clean up local government balance sheets is still in progress. The relevant numbers are that residential floor space starts have fallen close to 60% from the 2021 peak, prices have stabilised in tier-one cities, and the inventory clearance programmes that buy unsold housing for use as affordable rentals are running at scale in selected provinces. The fiscal cost is real but contained, and it is being absorbed through the augmented deficit rather than through forced restructurings of the developer balance sheets.

The risk to flag is that local government financing vehicles still carry an estimated USD 9 to 12 trillion of debt, and the rolling refinancing of that stack is the quiet macro story most foreign investors are not watching. The central government has shown willingness to backstop systemic LGFVs and the cost of insurance on those names has come down meaningfully, but a setback here would be the cleanest way for the bear case to come back into focus.

Tools for China Exposure

For an investor wanting broad China exposure, the cleanest blunt instrument is FXI, which gives you the largest 50 mainland-listed names with offshore-tradable wrappers. MCHI is broader and includes more of the platform internet companies. ASHR gives onshore A-share exposure, which is a different beast because the buyer base is dominated by domestic retail and the correlation to global risk-off is lower. KWEB is the focused internet platform play and is the highest-beta way to be long the catch-up trade if the platform names keep healing.

For more directional exposure, leveraged ETFs are the wrappers retail investors reach for. YINN is the 3x bull and YANG is the 3x bear, both daily-reset products built on the FTSE China 50 index that FXI tracks. We trade the leveraged China side in our own systematic momentum book, where YINN sits as one of the long-side legs alongside semiconductors and biotech. Over a multi-year horizon, the path-dependency of daily-reset 3x ETFs is real and material in choppy regimes, which is why we treat them as tactical instruments inside a systems-driven framework rather than buy-and-hold positions.

For investors who want individual-name exposure, the cleaner setups in our view are the offshore platform names that have lagged the broader rerating, the domestic semiconductor and semicap equipment names benefiting from the localisation push, and select consumer staples where the deflation grinder has now reversed. We avoid the developer names and the LGFV-exposed banks, where the work to clean up the balance sheet is still in progress.

Catalysts to Watch

The political calendar is heavy through the back end of 2026. The Trump-Xi tariff pause is set to expire on 11 November 2026, and the APEC summit is hosted by China in Shenzhen on 18 to 19 November 2026. The market is not pricing a clean re-escalation of tariffs, but the expiry is the tightest fixed-date catalyst on the calendar and the path through it is the single most important variable for offshore-listed China exposure into year-end. A constructive outcome reinforces the stability premium and pulls in incremental allocator capital. A worse outcome would not unwind the structural reflation but it would compress multiples in the export-heavy names.

The Central Economic Work Conference in mid-December typically sets the policy tone for the following year, and the National People’s Congress in March 2027 will fix the next twelve months of fiscal targets. Between now and then, the data points to watch are monthly PPI prints to confirm reflation continues, monthly residential floor space sold to confirm property stabilisation, and the official PMI to confirm manufacturing momentum.

Key Risks

The risks to the constructive view fall into three buckets. The first is geopolitics, where a Taiwan flare-up or a hard tariff escalation would force a re-pricing of the equity complex regardless of domestic fundamentals. The second is property and LGFVs, where a missed rollover or a sharper-than-expected leg lower in tier-two and tier-three city prices would pull the property drag back into the headline. The third is currency, where a renewed dollar bid driven by a more hawkish Fed or a global risk-off would reverse the recent USD/CNY move and reintroduce the FX drag on dollar-denominated returns.

For Australian investors there is one extra layer to think about, which is that the AUD is correlated to Chinese demand for iron ore and base metals. A stronger China through 2026 should be marginally supportive for AUD, which means the unhedged dollar return for an AUD-based investor in FXI or MCHI is partly offset by the FX move. This is a smaller effect than the headline equity move but it is worth modelling if the position is sized.

Where We Land

The setup that mattered for the China trade in 2024 was capitulation. The setup that matters now is the slow grind of stability becoming consensus. Growth is holding, prices are rising, the currency has turned, and the policy mix is doing exactly what it should without forcing the central bank into a corner. The equity wrappers have moved off the lows but the rerating is not stretched, and the offshore platform names have lagged enough to offer a clean catch-up trade if the constructive view plays through. The honest call is to be selectively long the China complex into the back end of 2026, with the leveraged wrappers used tactically and the platform names used as the higher-beta expression of the catch-up.

If you would like to discuss the China complex or how this exposure might fit within your portfolio, request a callback or call us on 1300 889 603.

ETF Universe

- FXI · iShares China Large-Cap ETF · 1x FTSE China 50, broad mainland blue-chips

- MCHI · iShares MSCI China ETF · 1x MSCI China, broader index including platform internet names

- ASHR · Xtrackers Harvest CSI 300 China A-Shares ETF · onshore A-share exposure

- KWEB · KraneShares CSI China Internet ETF · focused tech-platform exposure

- YINN · Direxion Daily FTSE China Bull 3X · 3x daily long FTSE China 50

- YANG · Direxion Daily FTSE China Bear 3X · 3x daily short FTSE China 50

Note. Leveraged ETFs are designed for daily directional exposure and exhibit volatility decay over multi-day holding periods. They are appropriate inside a systematic trading framework with defined entry, sizing, and exit rules, not as buy-and-hold instruments.

References

- National Bureau of Statistics of China – CPI, PPI, GDP, retail sales monthly releases

- People’s Bank of China – monetary policy reports and FX fixings

- iShares FXI fact sheet

- iShares MCHI fact sheet

- Xtrackers ASHR fact sheet

- KraneShares KWEB fact sheet