The FY2027 Commonwealth Budget delivered the biggest change to capital gains tax since 1999. Institutional sell-side economics research assessed the Budget as broadly deficit-neutral at the headline level but incrementally expansionary for GDP growth once off-balance sheet spending, state government activity and the composition of revenues are factored in. MFAM’s read of the analysis is that the headline number understates both the fiscal impulse and the magnitude of the structural shift in Australian property investment rules. Every property investor in Australia needs to understand what changed last night.

Research published 13 May 2026. All figures from Commonwealth Treasury and institutional economics research.

The Headline Deficit Numbers Are Stable. The Detail Is Not.

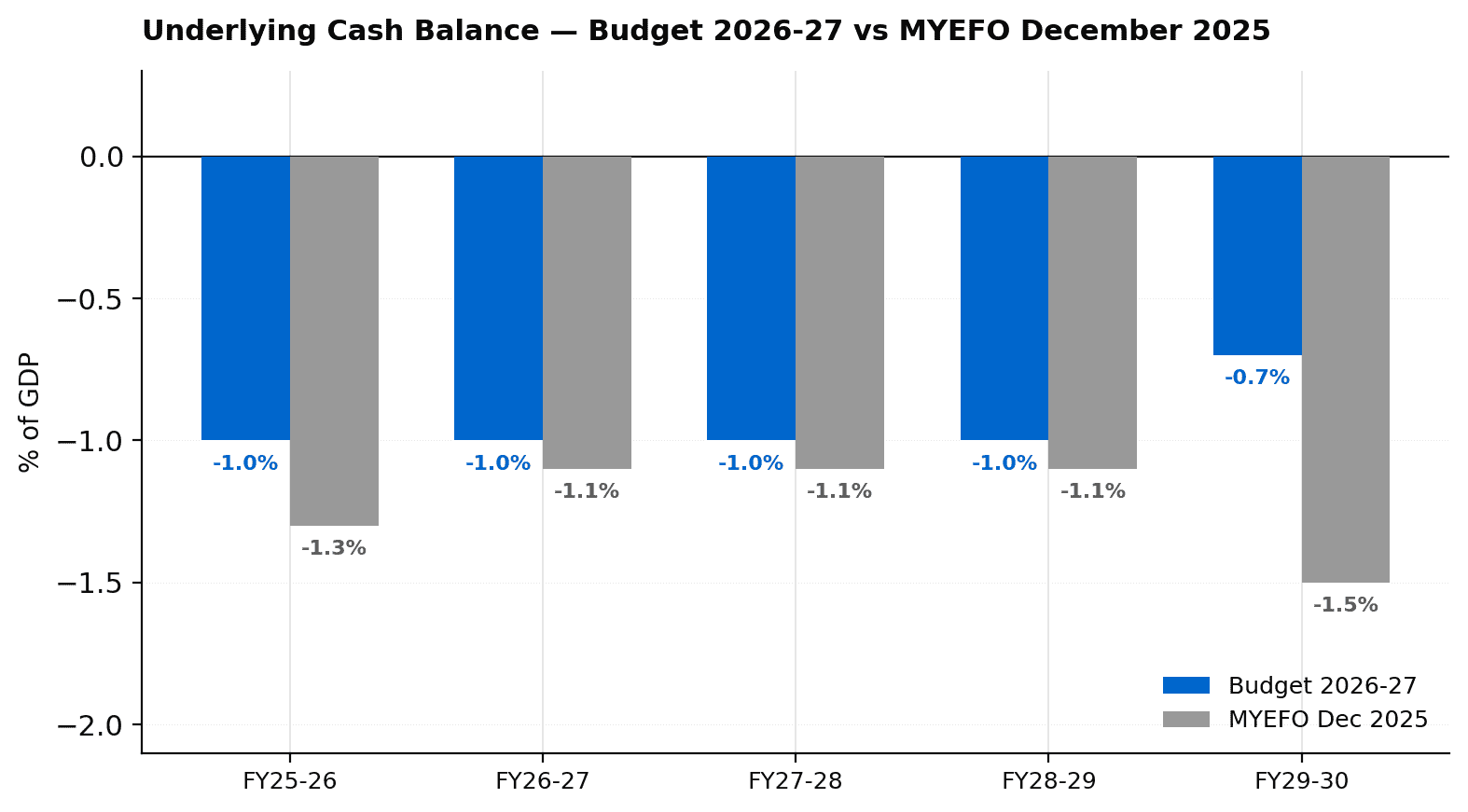

The FY2027 Budget projects an underlying cash deficit of A$31.5bn, or 1.0% of GDP, for the coming year. That deficit is forecast to hold at approximately 1.0% of GDP through to FY2029 before narrowing to 0.7% in FY2029-30. Relative to the December Mid-year Economic and Fiscal Outlook, the Budget shows a cumulative A$44.9bn improvement over the five years to FY2030. The headline looks modest. The improvement owes almost entirely to A$41.1bn in higher-than-expected tax revenues driven by commodity prices and personal income tax bracket creep, not to new policy restraint. The net impact of actual policy decisions was a more modest A$8.2bn improvement.

Net debt is projected to peak at 21.9% of GDP by FY2030, somewhat lower than the MYEFO forecast of 22.6%. On a consolidated Australian Government basis, which includes state government debt, net debt is forecast to rise to 35.2% of GDP in FY2030. That continues to compare favourably to the advanced economy average of approximately 80% of GDP. The fiscal position is not a crisis by any international benchmark. But the trajectory is spending-driven, with receipts staying broadly stable as a share of GDP while payments rise.

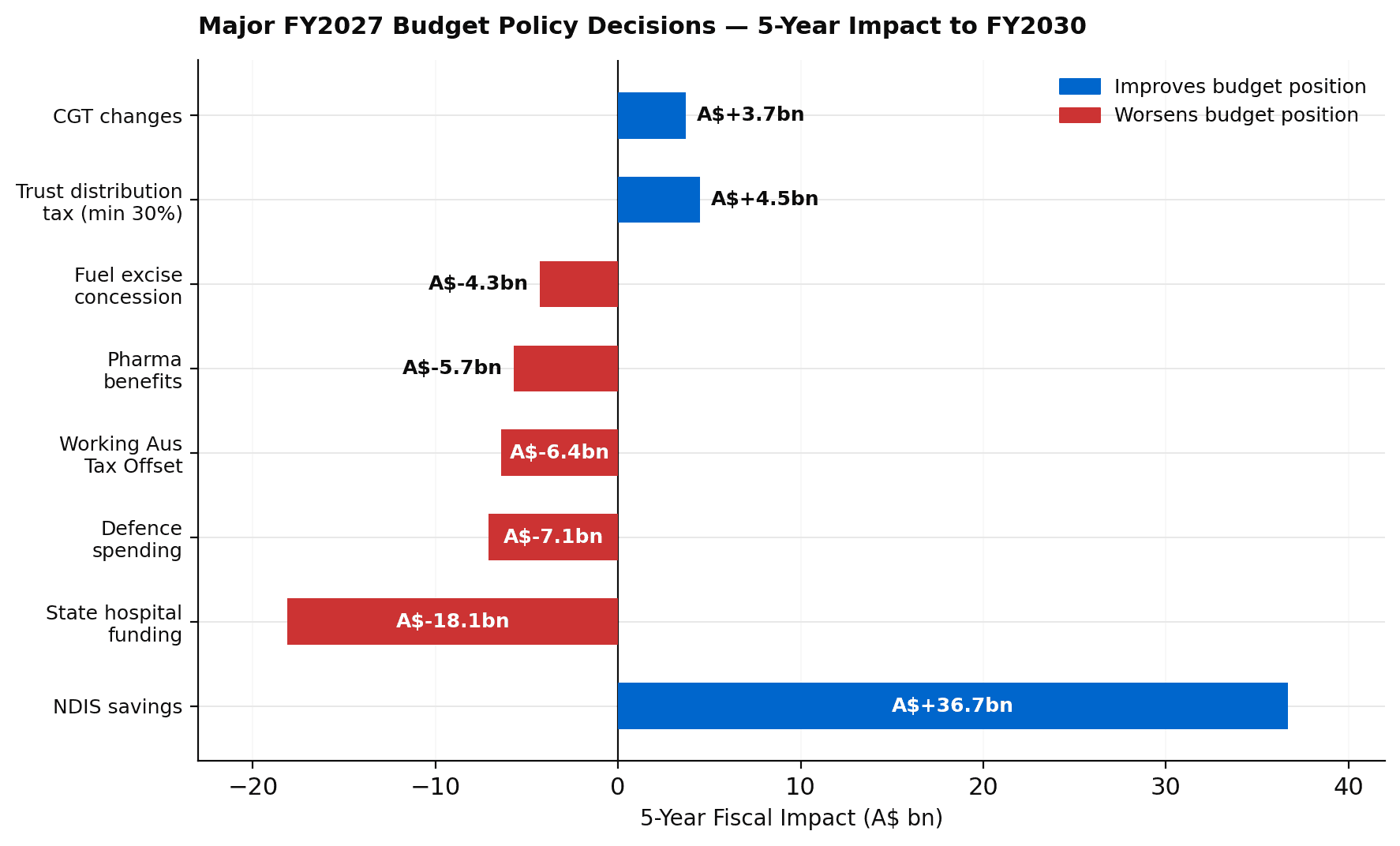

The Policy Decisions: NDIS Savings Fund New Spending

The net A$8.2bn improvement from policy decisions over five years masks a significant reallocation of spending. The government is projecting A$36.7bn in NDIS savings relative to the MYEFO trajectory, driven by tighter eligibility, a fraud reduction program and lower cost growth assumptions. Those savings are effectively being redistributed: A$18.1bn goes to state government hospital funding under the National Health Reform Agreement, A$7.1bn goes to additional defence spending to reach 3% of GDP by 2033, and A$6.4bn funds the Working Australians Tax Offset of A$250 per wage earner delivered in 2H2028.

The fuel excise concession cuts petrol and diesel by 32 cents per litre for three months and reduces the heavy vehicle road user charge to zero for the same period. New capital gains and trust distribution tax changes contribute a combined A$8.2bn improvement over the five years, which sounds significant in isolation but represents a small fraction of the overall tax revenue windfall. The big fiscal driver of the improvement is not policy reform. It is commodity prices and bracket creep lifting the revenue base in ways the government did not engineer.

Capital Gains Tax Reform: Australia’s Biggest Change Since 1999

From 1 July 2027, the 50% capital gains tax discount that has applied to assets held for more than 12 months will be replaced by an inflation indexation model. Under the new rules, the taxable capital gain is the real gain after adjusting for inflation at 2.5% per year, with a minimum 30% tax rate applying to the real gain. Existing assets are grandfathered: investors will have their assets valued as of 1 July 2027, and any gain accrued under the old rules up to that date remains eligible for the 50% discount. Any gain accrued after that date is taxed under the new indexation method.

The practical effect depends on the rate of return. When annual returns are more than roughly twice the rate of inflation, the indexation method produces a larger tax bill than the old 50% discount. For an investor generating 10% annual returns over a ten-year hold, the new rules place Australia in the OECD’s top three highest-taxing nations for capital gains on that asset class. For investors generating returns closer to inflation, the indexation method is more generous. Most Australian property investors have historically generated returns well above inflation, which means the change is not cosmetically neutral for the typical residential property owner planning to sell.

Negative Gearing: Grandfathered for Existing Owners, Quarantined for New Ones

From 1 July 2027, negative gearing for established dwellings will be restricted. Investors who purchased their properties on or before 12 May 2026 remain exempt from the new rules and can continue to deduct investment property losses against all income under the old arrangements. For investors purchasing established dwellings after that date, any operating losses can only be deducted against rental income and future capital gains on the property, not against wage or other income. Negative gearing remains fully available for newly constructed dwellings regardless of purchase date.

The structure creates a two-tier property market. Older investors with existing properties retain a materially more favourable tax treatment, which is likely to reduce their incentive to sell. Younger buyers purchasing existing properties face a higher effective cost of carry, as any loss from holding a negatively geared property is now quarantined until the property generates rental profit or is sold. The one-year grace period before the rules take full effect means decisions made in the next twelve months still fall under the old framework. The combined effect of the CGT and negative gearing changes is expected to push house price growth down to around negative 5% over the next twelve months, against a prior forecast of approximately negative 3%.

The Fiscal Impulse Is More Expansionary Than the Headline Suggests

Institutional economics research assessed the Budget as delivering an incrementally larger tailwind to GDP growth over the near term than the headline deficit stability implies. Three factors explain the gap. First, the net impact of active policy decisions adds approximately 0.2% of GDP in net spending over FY2026 and FY2027, a real stimulus irrespective of how the deficit headline reads. Second, the underlying cash balance excludes off-balance sheet financing, including a portion of the 2026 National Defence Strategy to be delivered via private-sector financing arrangements, which understates the net amount of public spending hitting the economy. Third, state governments, which have run expansionary fiscal programs including direct cost-of-living support in Victoria and Western Australia, sit outside the federal Budget but inside the economic activity that the RBA must contain. The aggregate fiscal impulse is forecast to accelerate GDP growth by approximately 0.15 to 0.2 percentage points over the first half of 2026, scaling to approximately 0.6 percentage points by end-2027.

The RBA Is Not Done

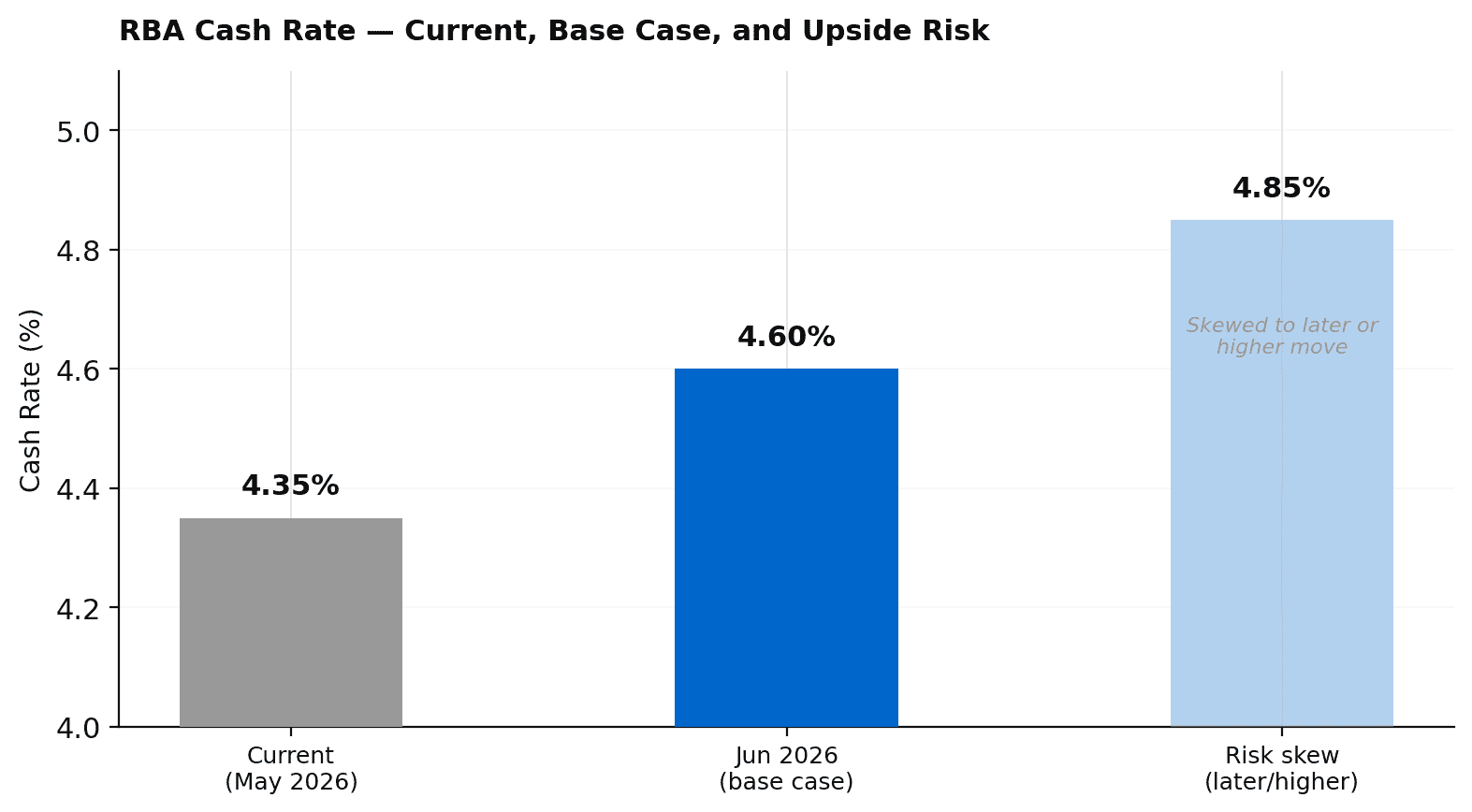

From the RBA’s perspective, the FY2027 Budget does not ease the case for further tightening. The central bank will take some comfort from the absence of major near-term cash handouts and the delay of the Working Australians Tax Offset until the second half of 2028. But the increase in net policy-related spending in the near term, the upside risk to residential rents from the housing tax reform reducing investor supply in established dwellings, and persistently high oil prices all add to the inflation picture. The base case for institutional economics is a June rate hike of 25 basis points, taking the cash rate to 4.60%, with the balance of risks skewed toward a later or larger move higher.

The housing market implication of a June rate hike is material. The combination of higher rates, CGT reform, and negative gearing restriction all weigh on investor demand for established dwellings simultaneously. Newly constructed dwellings are carved out of both the CGT and negative gearing changes, which may direct some capital toward new supply, but the near-term demand destruction on the established market looks more immediate than the new supply response. Property investors who purchased on or before 12 May 2026 are grandfathered under the old rules, which means the window for acquiring established property under the old tax framework closed last night. Whether that creates a near-term rush on newly constructed properties or a broader reassessment of residential property as an investment class is the key question for portfolio allocation in the months ahead.

Interested in how we can help? Get in touch with our team or call us on 1300 889 603.