The Reserve Bank Board meets on Monday and Tuesday next week with a rate decision at 2:30pm AEST on Tuesday. This is the most anticipated single-meeting call we have had in nine months. The case rests on a Q1 CPI print released on Wednesday that did two things at once. The headline ripped higher and the underlying measure barely moved. Both reads are right, both matter, and the resulting call is harder than it looks.

We still think the RBA hikes on Tuesday from 4.10 to 4.35 percent, and the rest of this piece is why.

Published 1 May 2026.

What the Print Actually Said

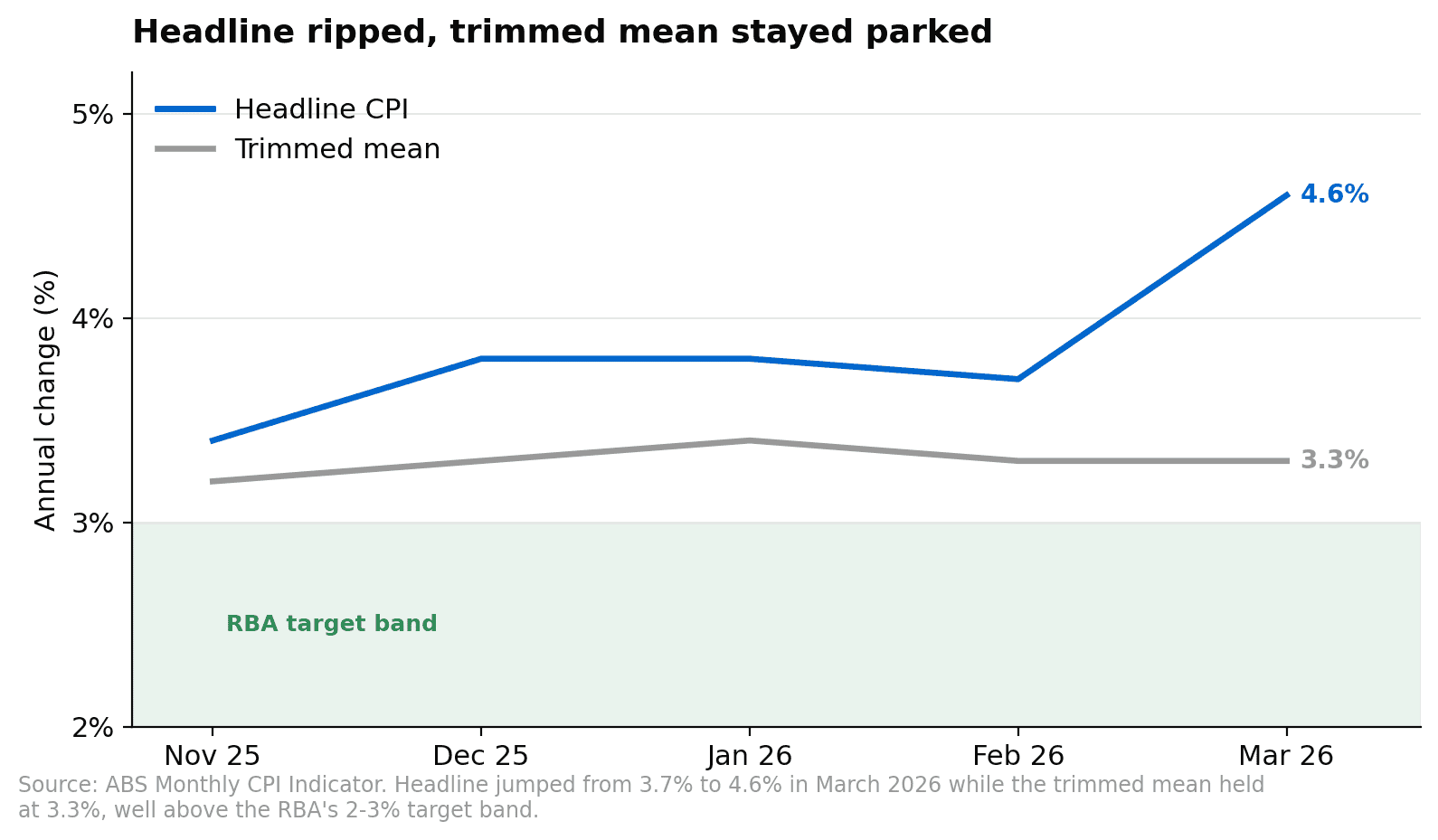

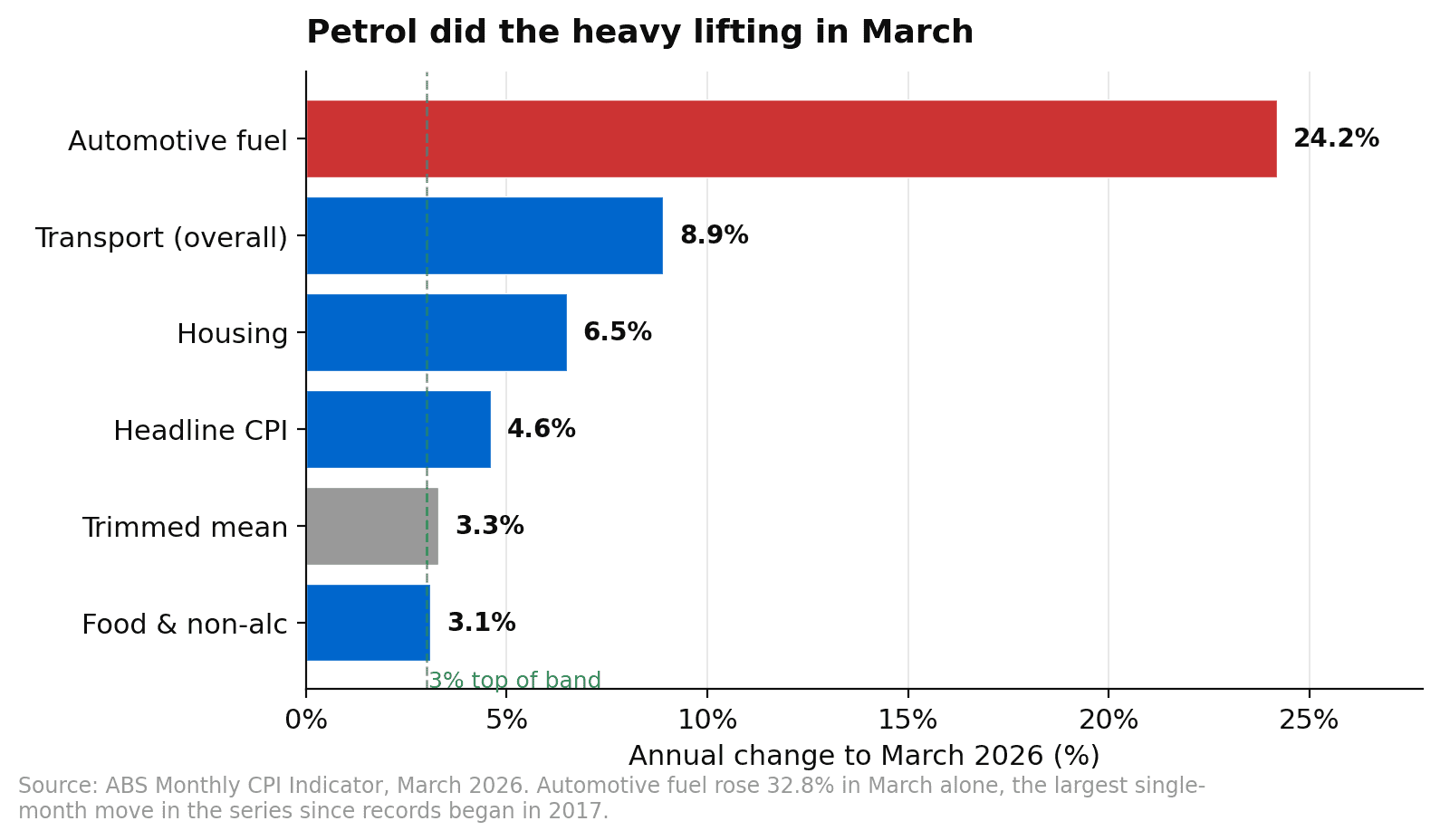

Headline CPI for the year to March came in at 4.6 percent, up from 3.7 percent in February. That is a one-month jump of nearly a full percentage point and the highest annual rate since September 2023. The quarterly rise was 1.4 percent, almost double the pace the RBA had been comfortable with for most of the last year. Petrol prices were the standout. Automotive fuel rose 24.2 percent over the year and 32.8 percent over March alone, which was the largest single-month jump in the series since records began in 2017.

The trimmed mean told a quieter story. It came in at 3.3 percent through the year to March, unchanged from February. The trimmed mean strips out the items moving the most in any given period, on the basis that those moves are usually noise rather than a signal about underlying demand. So when headline rips and trimmed mean stays put, the technically correct read is that the move is being driven by a handful of supply-side prices rather than by broad-based price pressure across the basket.

The market read this print as more dovish than feared. The Australian dollar barely moved, the front end of the bond curve was firmer rather than weaker, and the implied probability of a hike on Tuesday eased from above 75 percent to around 70 percent. That is the trimmed mean talking. If you only had time to look at one number, that is the one that gives the RBA cover to hold.

Why That Read Is Probably Wrong

The trimmed mean is a useful tool but it is not the only tool. It works well when supply shocks are isolated and short-lived. It works less well when the supply shock is large, persistent, and starting to seep into other prices. The Q1 print sits in the second category, and three pieces of context tell you why.

The first is the breadth of what is moving. Housing rose 6.5 percent over the year, transport rose 8.9 percent, and food and non-alcoholic beverages rose 3.1 percent. These are three of the biggest weights in the basket and the first two are running well above the target band. If the move were genuinely just petrol, transport would carry the weight by itself and the rest of the basket would be quiet. It is not. The shock is widening, and a widening shock is exactly what a trimmed mean cannot see, because the more items move together the fewer get trimmed out.

The second is the inflation expectations data. The ANZ-Roy Morgan measure rose to 6.6 percent in late April, up 0.3 percentage points from March. That is the highest reading in over a year. Households are not just feeling the petrol price, they are starting to revise their assumptions about future prices. This is the precise mechanism that drives second-round effects from a one-off shock into ongoing inflation, and it is the single most important variable for any central bank trying to distinguish a temporary disturbance from a persistent one.

The third is the labour market. The unemployment rate has been holding around 4.0 percent for several months, well below the decade average and well below most estimates of where the labour market starts to slacken naturally. That is the environment in which workers can negotiate higher wages in response to higher prices, and that wage push is the channel that turns a transient shock into a sticky one. We covered this in the 24 April piece on terms of trade, and nothing in this week’s data has weakened the argument.

Net it out, and the headline is doing more work than the trimmed mean can capture. The RBA knows this. It has spent a decade telling Australians it watches the underlying measure most of the time, but every time it steps off the underlying measure to give weight to a headline read, it does so when a supply shock is broad, persistent, and at risk of embedding. That is precisely the situation now.

What the Fed Just Did Tells You What Australia Is Up Against

The Federal Reserve held the funds rate at 3.50 to 3.75 percent on Wednesday morning Sydney time. That part was expected. What was not expected was the dissent pattern. Four members voted against the decision, the largest split since October 1992. One wanted to cut. Three wanted the statement to drop the easing bias. The Committee is genuinely fractured on whether to lean dovish or hawkish from here, but the dissents skewed hawkish, and the easing-bias language survived only because the Chair could pull together five votes for it.

The implication for Australia is that there is no help coming from offshore on the dovish side of the trade. If anything, the Fed is closer to the next meaningful policy decision being a removal of easing bias than another cut. Australian rates can no longer free-ride on a coherent global easing narrative because there is no coherent global easing narrative. That makes domestic data more important to the local rates path than it has been at any point this cycle.

The Case for the RBA Holding

It is worth stress-testing the hike call, because the case for a hold on Tuesday is not nothing.

The trimmed mean staying flat is a real signal. The RBA has framed the cycle around getting underlying inflation back inside the 2 to 3 percent band by year-end, and the trimmed mean at 3.3 percent is consistent with that path even after the headline ripped. A central bank that hikes off a headline driven by petrol takes ownership of an outcome that may resolve itself within two months as fuel prices stabilise.

Consumer spending data is also softer than it was in late 2025. Retail spending growth has been running below the inflation rate in real terms for two consecutive months, and household saving rates are starting to rebuild from the lows of mid-2025. A central bank that hikes into a softening consumer is taking on growth risk for an inflation outcome that the trimmed mean tells you is contained.

And the Statement on Monetary Policy that drops alongside the decision will set forecasts for the next two years. If the RBA wants to revise its inflation forecast higher without moving on the cash rate, the May SMP gives it the platform to do that and signal that more hikes are on the table without acting before it sees the next print.

These are real arguments. We do not think they win.

Where We Land

The RBA hikes on Tuesday to 4.35 percent. The combination of a 4.6 percent headline, broadening underlying pressure, rising inflation expectations, and a labour market that has not loosened gives the Board the cover it needs to lean in rather than look through. The trimmed mean is the cleanest counter-argument and it is still consistent with hiking once and then taking stock at the June and August meetings.

The bigger picture is the divergence trade. The Fed is fractured but tilting hawkish on the margin and a long way from cutting. The RBA is moving in the opposite direction on a cleaner data path. The Australian rate cycle is now genuinely out of phase with the rest of the developed world, and a market that is still pricing the AU curve through an offshore easing lens is going to have to reprice that.

What This Means For An Australian Portfolio

Miners remain the cleanest beneficiary of the macro setup. Iron ore and LNG continue to trade well, and the names with the most leverage to the export commodity basket benefit from both the price moves and the AUD support that flows from a higher domestic rate path. We covered this in detail in the 24 April piece and Tuesday’s decision does not change the conclusion.

Banks face the same near-term tailwind from any cash rate move that we flagged a fortnight ago. Net interest margins widen mechanically when the cash rate rises ahead of deposit repricing. The medium-term call is more nuanced because two more hikes from here puts genuine pressure on mortgage serviceability, but the May print itself supports the names.

Bond proxies remain the stretched part of the local market. Listed REITs, infrastructure trusts, and long-duration growth names have been priced through the back half of 2025 on an easing rate narrative that has now decisively reversed. Anyone holding oversized positions in the names that ran hardest through that period needs to be running the scenario where the two-year yield is 50 basis points higher in three months and asking what it does to their valuation.

The Australian dollar gets a boost from both the rate differential and the terms of trade dynamic. It is a headwind for offshore-earner industrials like CSL, ResMed, and James Hardie. It is a tailwind for domestic retailers importing inventory and for any business carrying USD-denominated debt.

The Broader Point

Tuesday’s decision is the cleanest test we have had this cycle of whether a central bank, faced with a real-time supply shock that is starting to broaden, takes the textbook step of leaning in. The textbook says hike, the trimmed mean gives a counter-argument, and the easy money has already been made on the offshore commentary that says the world is easing. Australia is not the world, and the data this week was strong enough to make the call.

We will know on Tuesday afternoon whether the Board agrees.

Want to discuss how the RBA decision and the rates outlook affect your portfolio? Call us on 1300 889 603 or book a call-back.