The Reserve Bank (RBA) has been in a tough spot lately.

Yes, it misread the economy in the aftermath of the pandemic. But the RBA wasn’t the only central bank that went all out in providing stimulus.

It wasn’t just the RBA that was late in recognising inflation risks. And it wasn’t the only central bank that said they thought interest rates would remain low for a very long time.

However, it isn’t the RBA which is the problem for the public. It is the current conditions facing the economy.

Inflation is too high for comfort at an annual rate of 7.8% or 7.4% with the monthly measure.

At the same time, while households face higher costs for everything – petrol, energy bills, even a holiday up or down the coast, costs much more than what it used to be.

It would feel as though the last thing that would be needed is a bigger interest rate bill.

But when the economy has been running too hot for the capacity of the economy, demand needs to slow. Interest rates are just a tool to help achieve that.

In this topsy-turvy world, bad news may have become good news.

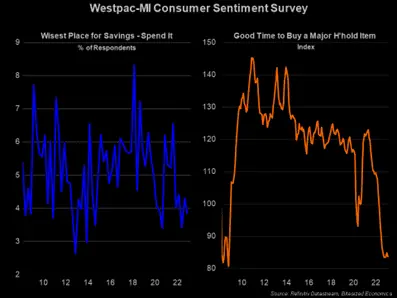

So perhaps the good news is that there are signs that the economy is slowing. This weakening has been most evident with the consumer. They no longer think it’s a good time to be spending up.

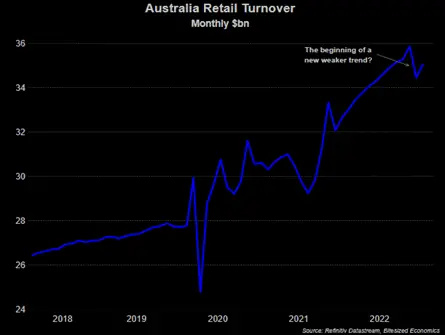

Of course, it isn’t enough for people to say they don’t want to spend. It’s what they actually do. On this front, you can see that a weaker trend might be beginning to form:

It also makes intuitive sense that consumers will be spending less, because those rate hikes are going to bite more than what they had in previous rate-tightening cycles.

We haven’t been in a rate-tightening cycle in over 12 years, so there’s an added uncertainty about how rate hikes are hitting the economy.

A lot has changed since then – home prices have risen nearly 60%. An average new mortgage for an owner-occupier used to be worth around $350,000.

Today, the average size for a new owner-occupier home loan sits at around $600,000.

Analysis from the RBA has shown that over half of borrowers on owner-occupier loans with variable rates would have spare cash flows decline by over 20% over the next couple of years.

For those on fixed rates, the adjustment is even bigger – the RBA estimates that over 60% of borrowers would see an increase of at least 40% in their minimum repayments this year (assuming the cash rate rises to above 3.60% in 2023).

Thankfully, the RBA has continually been at pains to express that borrowers have built up large savings buffers over the years when interest rates were low.

Whether these borrowers decide to cut down on spending or draw down on their savings or a bit of both is up for debate. However, it would be expected that the majority of people would now be thinking more carefully on what they are spending.

Renters are also facing a bigger squeeze, given that they also need to devote a bigger chunk of their income to rent.

So, there is good reason to believe that the interest rates to date will indeed, negatively impact demand in the economy in a tangible way. And more so than in previous rate-tightening cycles.

That will mean lower inflation. Stable oil prices, easing inflation in other parts of the world and the waning flood impact are also all suggesting that inflation should come down over the year.

There is still the big question of how much demand will need to weaken to bring down inflation sufficiently.

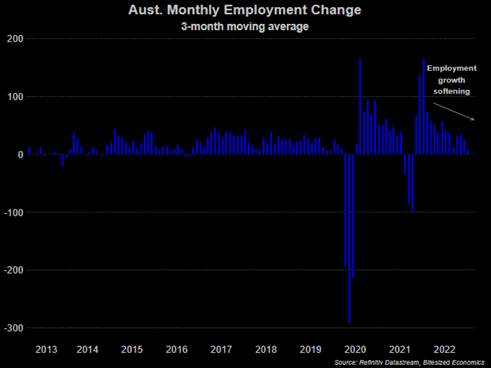

The good news for the inflation outlook is that there have been early signs that job growth has softened. Policymakers look at the labour market carefully because it has implications for the longer-term inflation outlook and wage outcomes.

Recently, financial markets have become more concerned about the strength of economic activity and inflation in the US and that it would result in higher interest rates than what had been expected.

But it would be a mistake to automatically translate the US experience to Australia.

For one, Australian economic data of late is painting a different picture, and secondly, there is a valid argument that rate hikes from the RBA impact the economy more than the US.

Australian home loans tend to be on a variable or shorter-fixed term rate compared to the 30-year fixed-rate mortgages in the US.

Governor Lowe once said that the relatively slower pace of wage growth in Australia would mean that it would not face the same extent of inflationary pressures as the rest of the world.

While that kind of thinking likely eventuated into a late policy response to the inflationary pressures that Australia witnessed, Lowe is not wrong in thinking that in some ways, Australia is different.

The RBA is likely to raise interest rates higher still, but a more cautious approach would be the smart move. It remains early days, but the evidence is suggesting that demand, and inflation, are being hit. Especially for the consumer.

If you would like to see more of her thoughts and analysis on global and Asian economic developments, you can subscribe to her newsletter or access all her other content at Bitesized Economics.

Janu isn’t afraid to step away from consensus and do things a bit differently. This has been the motivation for her to start Bitesized Economics in 2021. Bitesized Economics is an economic service providing independent analysis and content that is easily accessible, ‘bite-sized’ and easy to understand. The aim is to allow both financial experts and the everyday person to digest the important implications for their life and work.