Corvus Pharmaceuticals is one of the more interesting clinical-stage biotechs in the market right now. The company has developed soquelitinib, a first-in-class oral ITK inhibitor that is attacking two very different opportunities with the same molecule, moderate-to-severe atopic dermatitis on one side and peripheral T cell lymphoma on the other. At the $15.04 current share price, the stock sits at a meaningful discount to the 12-month price target of $40, which implies roughly 166% upside.

Research published 21 April 2026. Price target and upside based on prices at time of publication.

About Corvus Pharmaceuticals

Corvus Pharmaceuticals (NASDAQ CRVS) is a US-based clinical-stage biopharmaceutical company founded in 2014, focused on the development of novel treatments for immunologic and inflammatory diseases and cancer. Its lead asset is soquelitinib, also referred to as SQL, a first-in-class oral small molecule inhibitor of interleukin-2 inducible T cell kinase (ITK). The company is headquartered in Burlingame, California, and trades on the Nasdaq with a market capitalisation of roughly $1.2 billion. More information at corvuspharma.com.

Why the Set Up Looks Attractive Here

The CRVS share price has had a wild ride. An early 2026 topline from the Phase 1 atopic dermatitis study was strong enough to take the stock from around $7 to a peak north of $25, before drifting back into the low to mid teens. That pullback is what has created the entry point. The current valuation, in our view, does not capture the full potential of a differentiated oral option in one of the largest biologics markets in dermatology, nor does it give enough credit for a late-stage, high probability of success programme in peripheral T cell lymphoma.

The global market for moderate-to-severe atopic dermatitis biologics is projected to grow from around $12.4 billion in 2025 to roughly $24 billion in 2035, driven largely by Dupixent, which alone is expected to generate around $13 billion in atopic dermatitis revenue in 2026. Despite that scale, the clinical picture remains unsatisfying. Roughly 20% of patients on advanced therapies remain refractory or not optimally controlled. Itch resolution in particular lags lesion clearance, and well over half of Dupixent patients do not achieve clinically meaningful itch reduction. That is the gap soquelitinib is walking into.

The ITK Inhibition Approach

Soquelitinib is a selective, oral inhibitor of ITK, a kinase involved in T cell activation and differentiation. By blocking ITK, the drug dampens Th2 and Th17 activity, which are the dominant inflammatory pathways in atopic dermatitis and hidradenitis suppurativa respectively. Critically, soquelitinib spares RLK (resting lymphocyte kinase), which preserves Th1 signalling. That matters because Th1 activity is what the body uses to fight off viruses and cancer, and switching it off is what has historically caused the safety problems with broader immunosuppressants.

The mechanism is effectively a reset for dysregulated T cell populations. By partially blocking ITK while leaving Th1 intact, the drug has been shown to push pro-inflammatory Th17 cells toward becoming functional regulatory T cells (Tregs), which is consistent with the early durable response signals the company has reported. Coupled with the convenience of an oral pill in a class that is currently dominated by injectable biologics, this gives soquelitinib a genuinely differentiated commercial positioning.

Safety has been the critical overhang for any novel immunology mechanism. On that front, Corvus has now treated over 150 patients for more than two years, representing more than 14,000 patient days of exposure, with no serious infections of any kind reported. None of the more than 30 patients in the Phase 1 PTCL study known to carry the EBV virus had any evidence of viral reactivation or related illness during treatment. Pharmacokinetic data also shows the 200mg twice daily dose achieves only around 75% ITK occupancy, meaning residual signalling pathways remain available to the immune system. That appears to be a deliberate feature, not a bug.

Atopic Dermatitis, Where the Bulk of the Commercial Value Sits

The Phase 1 Cohort 4 data is what makes this name hard to ignore. In moderate-to-severe atopic dermatitis patients who had previously stepped through at least one line of systemic or topical therapy, the 200mg BID arm over eight weeks achieved 75% EASI-75 against a placebo-adjusted response of 55%. Cross trial comparisons always need a health warning, but that 55% placebo-adjusted EASI-75 is the highest we have seen across emerging AD clinical stage candidates, and it is approaching the efficacy bar set by oral JAK inhibitors, which are the most potent systemic class currently approved.

The durability signal is what makes this look like more than just another entrant. In the Phase 1 extension, patients who had completed a 28 day treatment course showed EASI scores that remained broadly flat for three months post-treatment. Management has described this as a no rebound flares profile, which sits in direct contrast to the rebound seen with JAK inhibitors once therapy is paused. If that durability holds up in the larger Phase 2 SIERRA1 trial, it starts to frame soquelitinib not just as another maintenance drug but as something closer to a disease-modifying agent, giving patients the option of drug holidays rather than chronic daily dosing. That is a different conversation with prescribers, payers and patients.

The near term catalyst path is busy. Detailed Phase 1 Cohort 4 data is expected at the Society for Investigative Dermatology meeting in Chicago in May 2026, where the company will release additional biomarker and durability readouts. The Phase 2 SIERRA1 trial is already enrolling around 200 patients across three active dose arms (200mg QD, 200mg BID, and 400mg QD) plus placebo, with topline data expected around mid 2027. Phase 2 initiations in hidradenitis suppurativa and asthma are scheduled for later this year, both of which extend the pipeline-in-a-product thesis.

Peripheral T Cell Lymphoma, the Underappreciated Second Leg

The hematology story often gets less attention in the CRVS narrative, but in our view it provides a valuable de-risking underpin for the whole thesis. Peripheral T cell lymphoma (PTCL) is a group of aggressive non-Hodgkin lymphomas where outcomes are poor and treatment options are limited. In relapsed or refractory disease, two year survival rates sit around 25%, and the currently approved single agents, pralatrexate and belinostat, deliver overall response rates of only 25 to 29%, median progression free survival of just 3 to 4 months, and median overall survival between 8 and 15 months.

Soquelitinib’s Phase 1/1b data in this population at the 200mg BID dose showed an overall response rate of 39% (26% complete response), median duration of response of 17.2 months, median progression free survival of 6.2 months, and median overall survival of 28.1 months. Those numbers stack up well against the approved comparators, the trial has reported a clean safety profile with no dose limiting toxicities, and the FDA has granted the programme both Orphan Drug and Fast Track designations.

The registrational Phase 3 is open label, 150 patients, randomised 1 to 1 against investigator’s choice chemotherapy, with a crossover arm that allows patients in the control group to receive soquelitinib on confirmed progression. The primary endpoint is progression free survival. An interim futility analysis is expected by the end of 2026. We see the PTCL programme as potentially the first commercial product for the company with a realistic launch in 2029, which gives CRVS a base valuation foothold while the atopic dermatitis programme moves through its larger and longer pivotal readouts.

Pipeline In A Product

A lot of the value in CRVS does not sit in either of the two lead indications. It sits in the optionality that comes with having a mechanism that can plausibly address a wide range of Th2 and Th17 mediated conditions. Near term, the company has flagged hidradenitis suppurativa, a disfiguring skin disease where the standard of care is thin, and asthma, where IL-5 reduction by soquelitinib has already been demonstrated in early work, as the next two development priorities. Both have Phase 2 trials slated to initiate in 2026. Beyond that, the door opens to fibrotic disease, inflammatory bowel disease, systemic sclerosis, ALPS (an autoimmune lymphoproliferative syndrome), and solid tumour oncology.

Dupilumab provides the obvious precedent here, expanding from a single AD indication through asthma, CRSwNP, EoE, and several paediatric atopic diseases to become a genuine multi-billion dollar franchise. There are similar stories at Argenx with efgartigimod, and at Insmed with brensocatib and TPIP. The point is not that soquelitinib will do exactly what any of those did, but that the market is used to paying for well executed indication expansion once a lead molecule works. Corvus’s composition of matter patent runs through to 2042 with method of use coverage extending into 2044, so the commercial runway is long enough for the company to run that playbook.

Valuation

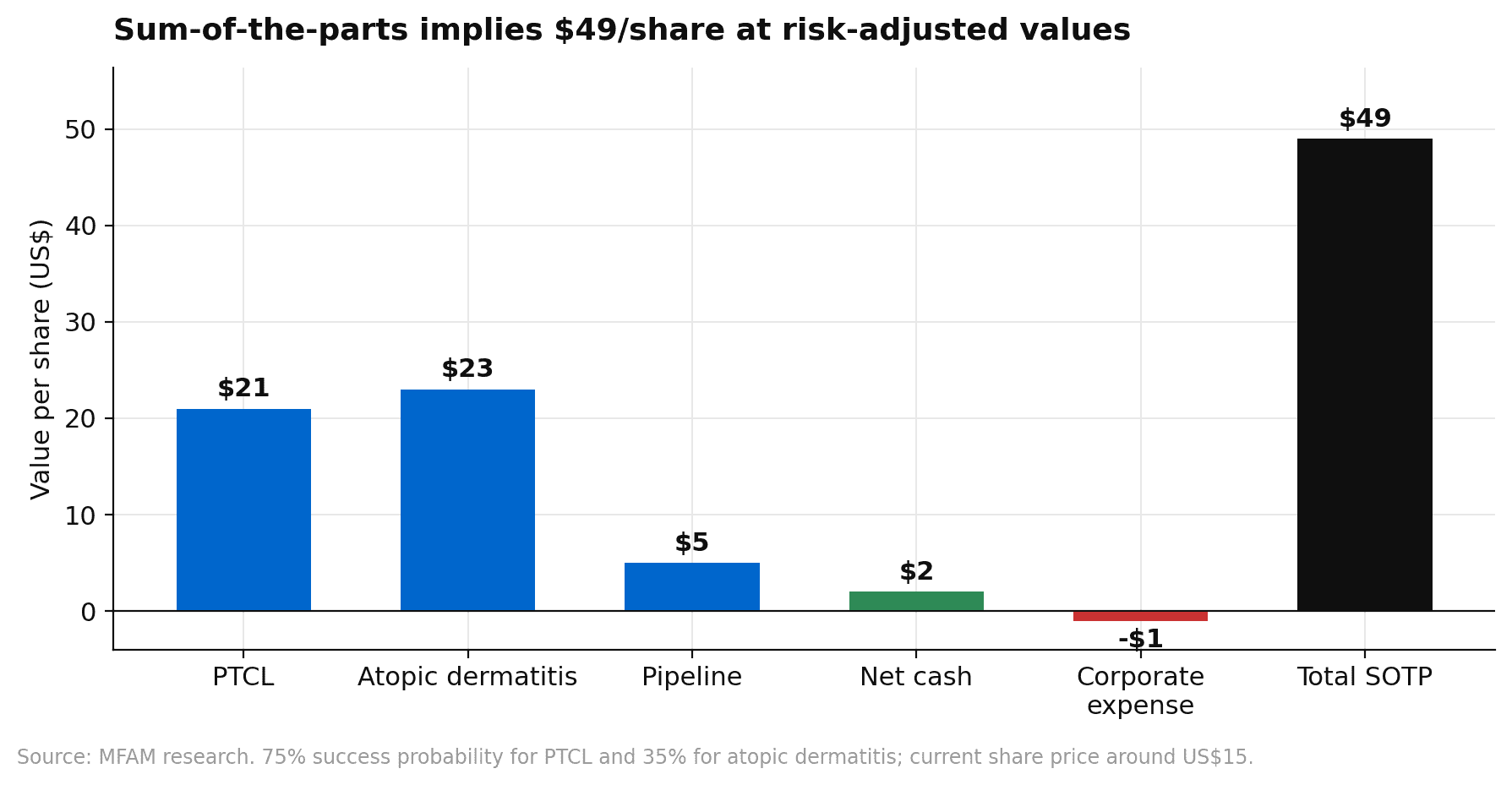

A discounted cash flow analysis using a 13% WACC, consistent with other clinical stage biotechs running pivotal hematology studies, and a 1% terminal growth rate produces an intrinsic value close to $40 per share. A sum-of-the-parts analysis with a 75% probability of success for PTCL and 35% for atopic dermatitis reaches $49 per share, with roughly $21 coming from PTCL, $23 from atopic dermatitis, $5 from the pipeline optionality, and $2 of net cash, offset by around $1 of corporate expense.

Under a 35% probability of success, risk-adjusted peak atopic dermatitis sales are modelled at around $1.5 billion in 2040, or roughly $4.2 billion on an unadjusted basis. PTCL peak sales are more modest at around $550 million globally by 2036, but that programme has a much higher success probability and a nearer commercial launch in 2029.

Risks

The risks to the thesis are clear. First and most obvious, the Phase 2 SIERRA1 trial may not replicate the Phase 1 Cohort 4 efficacy, especially given the small n of the earlier study. Expectations for novel mechanisms are high, and a placebo-adjusted EASI-75 that undershoots competitor benchmarks would meaningfully dent the case. Second, the safety profile, while clean so far, remains relatively young from a long term follow up perspective. Any emerging signal around infection, viral reactivation, or malignancy in a broader patient base would be taken hard by the market given how critical safety is to positioning in chronic immunology diseases.

Third, the AD market is crowded and getting more so. Apogee’s zumilokibart, Nektar’s rezpegaldesleukin, Pfizer’s tilrekimig, UCB’s galvokimig, Kymera’s KT-621 and others are all advancing through the clinic, some with their own claims to long dosing intervals, differentiated mechanisms, or oral delivery. Soquelitinib will need to continue differentiating on the durability, itch control and safety vectors to carve out meaningful share. Fourth, even with approval, newer AD agents have historically struggled with formulary access. Dupixent’s entrenched position means payers are willing to require step therapy, prior authorisation, and other constraints that slow real world uptake.

Our View

What we like about this set up is that we do not have to bet on any single outcome to make the position work. The PTCL programme alone, with its 75% modelled probability of success and a differentiated efficacy and safety profile against very weak standards of care, gives CRVS a floor that looks underappreciated at the current price. The atopic dermatitis programme is higher risk, higher reward, but the Phase 1 data is strong enough and the unmet need big enough that a credible path to a meaningful commercial product exists. The pipeline in a product optionality across hidradenitis suppurativa, asthma, and beyond is essentially free at the current level. The 12-month price target sits at $40, and on the weight of the clinical and commercial set up, we think the stock is worth a serious look here.

If you would like to discuss this or any of our other research positions with one of our advisers, please book a call back or phone 1300 889 603.