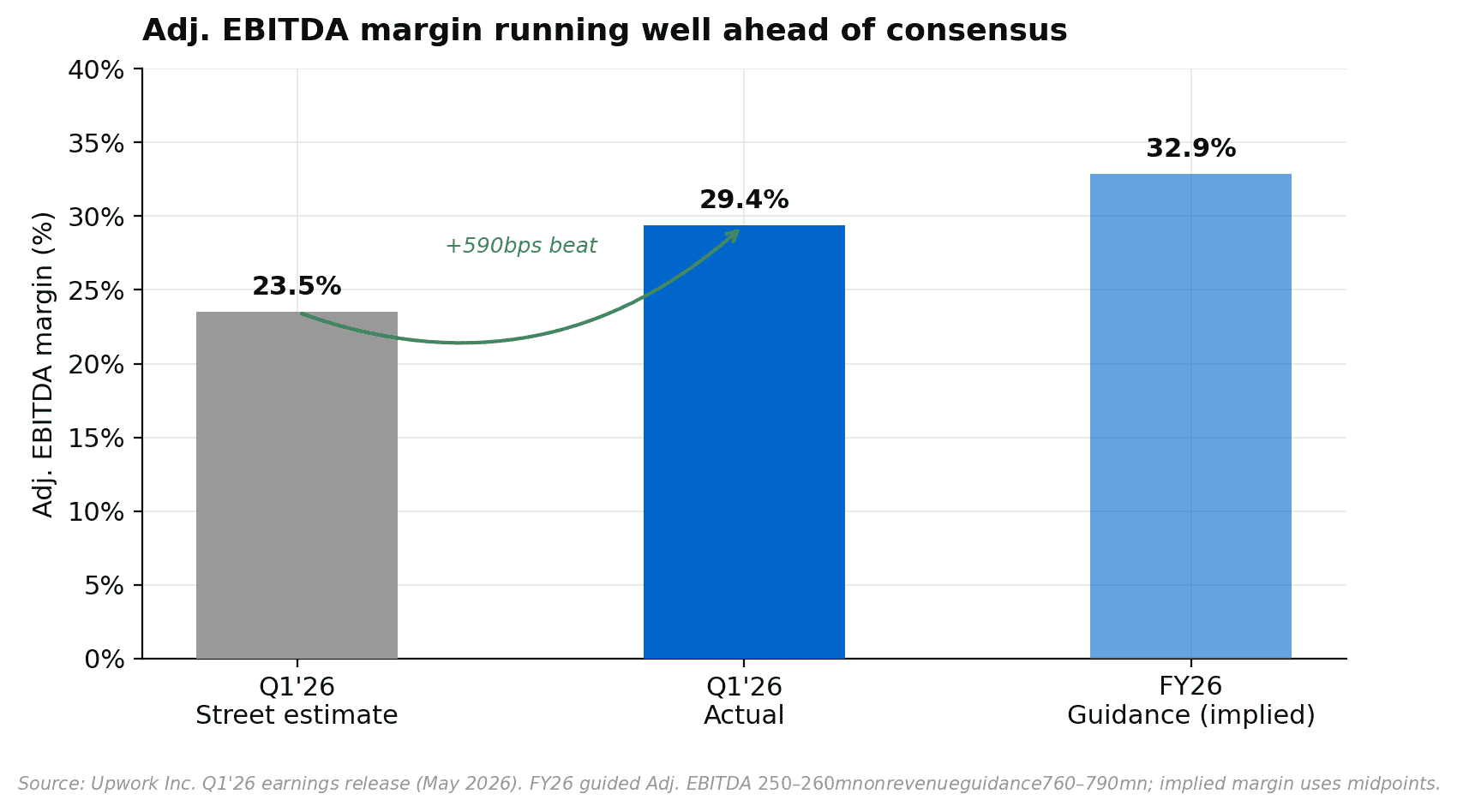

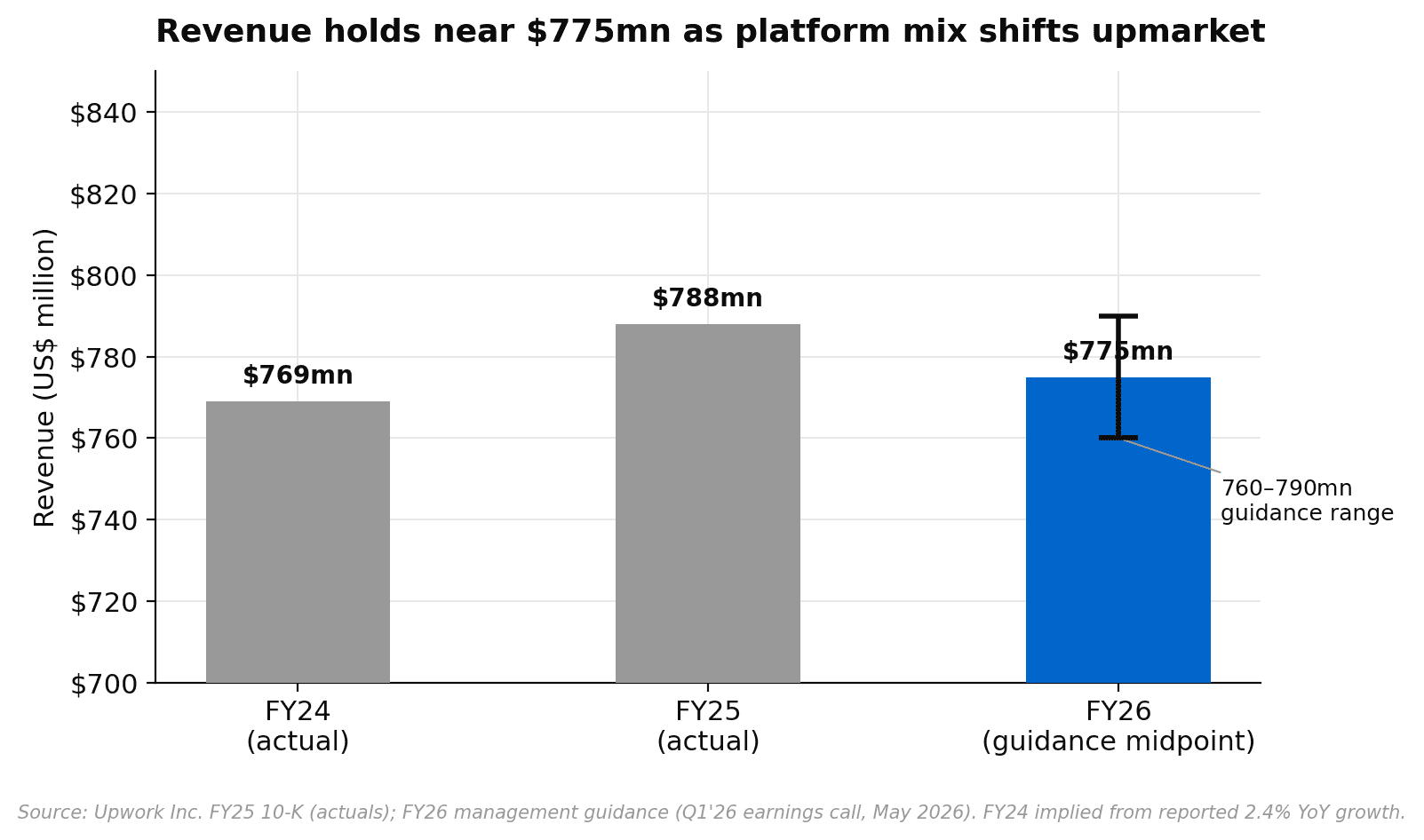

Upwork delivered a Q1’26 result that landed on the right side of a bifurcated narrative. Revenues came in around the midpoint of guidance at $195mn, while Adj. EBITDA of $57mn came in nearly 24% above consensus expectations, with the margin beat tracing back to a cost restructuring that has moved faster and cut deeper than the market had assumed. Institutional sell-side research rates Upwork a Buy with a 12-month price target of approximately US$17.50, implying around 98% upside from the recent close of US$8.82. The thesis is not that the revenue headwinds are finished, because they are not, but that the cost structure has been reset in a way that makes the forward margin profile look materially different from what the stock was priced for coming into the print.

Research published 13 May 2026. Price target and upside based on prices at time of publication.

About Upwork

Upwork is the world’s largest online work marketplace, connecting businesses with independent professionals across software development, creative services, finance, marketing and operations. Founded in 2013 through the merger of oDesk and Elance, the company is headquartered in San Francisco and generates revenue primarily through marketplace take rates, running at approximately 20% of Gross Services Volume (GSV), and enterprise managed services for larger clients. The platform serves around 784,000 active clients and a global pool of skilled freelancers spanning more than 180 countries. Upwork trades on the Nasdaq under the ticker UPWK with a market capitalisation of approximately US$1.2 billion. For more detail, see the Upwork investor relations page and the company’s most recent SEC filings.

The Cost Restructuring Is the Headline, Not the Revenue Softness

The Q1’26 result was, at its core, a profitability story. Management announced a restructuring plan that reduces headcount by approximately 24%, expected to deliver around $70mn in annualised savings. The Adj. EBITDA margin of 29.4% for the quarter was nearly 600 basis points above what the market had modelled, and Upwork responded by raising its full-year Adj. EBITDA guidance to $250-260mn while simultaneously lowering its revenue guidance to $760-790mn. That combination is worth sitting with. A company that cuts its revenue forecast and raises its profit forecast is not in structural trouble. The implication is that the business can generate meaningfully higher margins even in a softer revenue environment, which is not what the stock was pricing.

Gross margin held at 77.2% in Q1’26, consistent with recent quarters. The restructuring targets approximately $70mn in annualised savings, with the run rate building through the second half of FY26 as the workforce reduction takes full effect. Management expects to contribute approximately $40mn in savings from the FY26 year in aggregate, scaling to the full $70mn run rate in FY27. The cost base has been meaningfully reset, and that reset now anchors a forward margin profile that was previously not visible to the market.

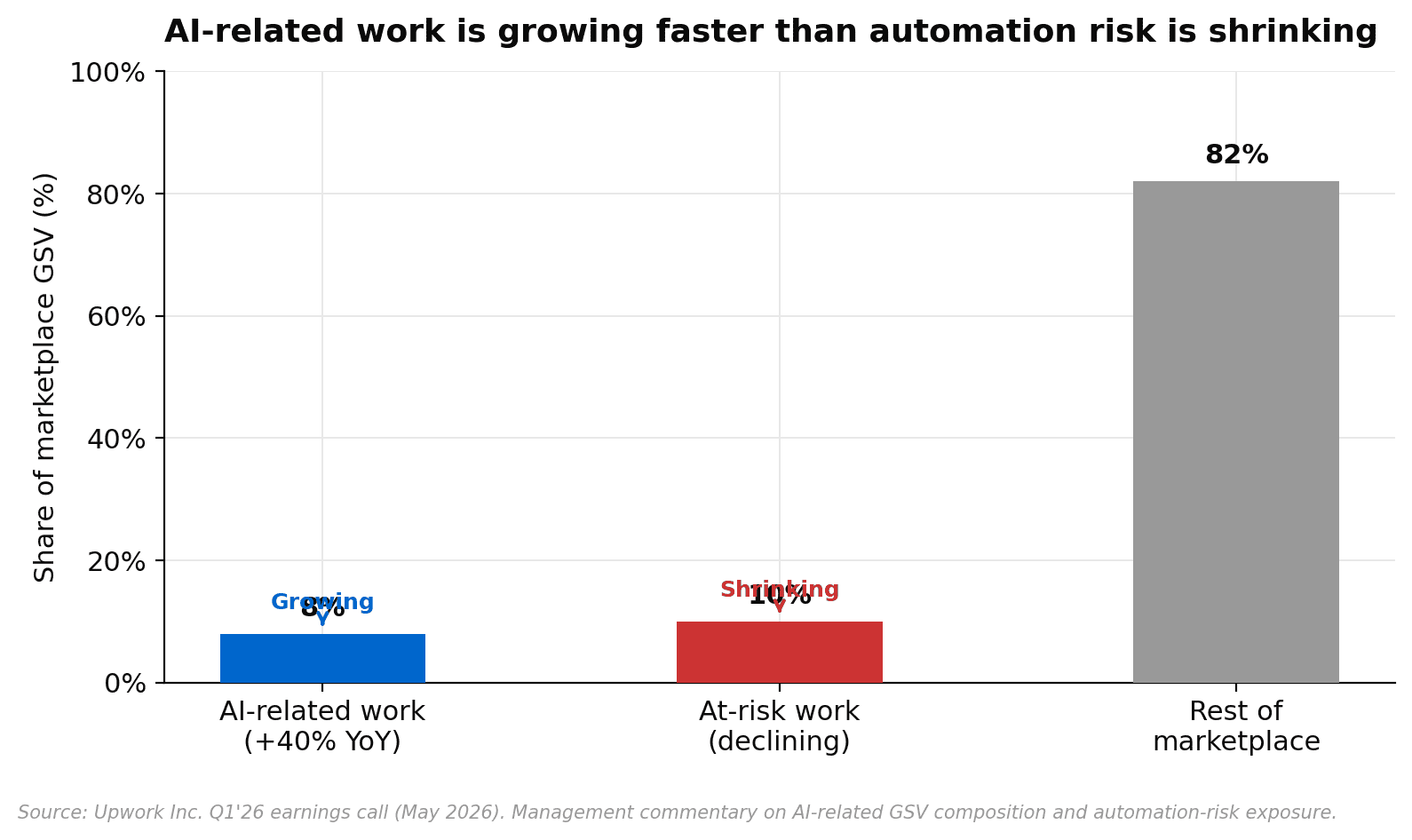

AI Is a Growth Driver on the Platform, Not a Threat

The central bear case on Upwork has been that AI automation would hollow out the low-value, repeatable tasks that represent a large share of freelance work. The Q1’26 data suggests that narrative is playing out selectively rather than broadly. AI-related GSV, meaning work tied to AI model training, prompt engineering, AI integration and adjacent tasks, grew approximately 40% year on year in Q1’26 and now accounts for around 8% of total marketplace GSV. At the same time, the portion of marketplace GSV considered at high risk of AI automation declined from approximately 11% to around 10%, and management indicated that proportion is expected to continue falling as the platform shifts toward higher-complexity work categories.

The dynamic that matters for the forward thesis is that Upwork is capturing AI-driven demand, not simply losing commodity work to AI tools. Management’s analysis suggests AI integration is generating new categories of work rather than purely displacing existing ones, and the platform is well positioned to intermediate that demand the same way it has intermediated software development and creative work for the past decade. The AI exposure on the platform is now a feature of the bull case, not a feature of the bear case.

Business Plus and Lifted Are Pulling the Platform Upmarket

The clearest structural shift in Q1’26 was the acceleration in Business Plus. Active clients in Business Plus grew 35% quarter on quarter, with GSV up 34% QoQ. Business Plus serves mid-market companies with higher average spend per project, sitting above the entry-level marketplace but below the full enterprise managed services tier. The 35% sequential client growth reflects deliberate platform investment in this cohort, and the GSV growth tracking alongside it suggests spend per client is also rising rather than simply more clients posting lower-value work.

The enterprise segment remains a near-term headwind, with revenue declining approximately 6% year on year in Q1’26. The forward catalyst is Lifted, Upwork’s new enterprise offering that combines AI-assisted talent matching with a cost structure management says delivers materially lower client acquisition costs compared with legacy enterprise configurations. Initial Lifted customer migrations are targeted to begin in June. The enterprise pipeline expanded in Q1’26 and management expects the Lifted rollout to translate into improved enterprise revenue in the second half of the year. The near-term softness is real, but the Lifted launch gives the enterprise segment a product catalyst the business has lacked for several quarters.

End-Market Softness Is Concentrated in the Low-Value Tail

Not everything in Q1’26 pointed in the right direction. Active clients declined approximately 3% year on year to 784,000, and total GSV of $987mn came in slightly below consensus. Management attributed both to weakness in the tail-end of the marketplace, the cohort of buyers and freelancers transacting on sub-$500 projects. That part of the platform is most exposed to the macro slowdown that has weighed on discretionary business spending since late February, as well as to competition from AI tools that can handle straightforward task automation at low or zero cost.

The revenue guidance of $760-790mn for FY26 reflects management’s expectation that headwinds on low-value work will persist through the year, with stabilisation expected into Q2 and a return to top-line growth anchored by the higher-value segments from there. The take rate of 19.8% held well in Q1’26, which matters because it tells us the revenue softness is volume-driven rather than pricing-driven. Losing low-value volume while holding the rate suggests the platform’s pricing power is intact, and the mix is shifting toward the kind of work where Upwork has more durable competitive positioning.

Valuation

The 12-month price target of approximately US$17.50 implies around 98% upside from the recent close of US$8.82. At the current share price, the market appears to be pricing the revenue softness and active client decline without giving meaningful credit to the margin transformation or the platform optionality from Business Plus and Lifted. Upwork trades at an enterprise value of approximately $933mn against a full-year Adj. EBITDA guidance midpoint of $255mn, a valuation that does not reflect the profitability trajectory the cost restructuring has now unlocked. The path to the price target is anchored by three things: a reset cost base delivering margins materially above what the market expected before the restructuring, an accelerating premium segment in Business Plus driving higher revenue per active client, and Lifted giving the enterprise segment a genuine product catalyst for the back half of FY26. For a platform where the margin story is now running ahead of the revenue story, and where the AI narrative is an asset rather than a liability, the risk-reward looks asymmetric.

Key Risks

The main downside risk is that end-market weakness in the low-value tail proves more persistent than the second-half stabilisation management is guiding for, which would put further pressure on the $760-790mn revenue range. Active client counts declining for multiple consecutive quarters is a platform health indicator to monitor closely; a continuation of the trend would signal the marketplace is contracting rather than simply remixing toward higher-value work, which is a structurally different problem. Enterprise recovery depends on Lifted migrations beginning in June as planned and scaling at meaningful volume, both of which carry execution risk in a product that has not yet seen broad commercial deployment. Broader macro deterioration and ongoing geopolitical instability have been management’s stated drivers of the demand slowdown that began in late February, and either factor intensifying would push the recovery timeline further out. Investor appetite for small-cap growth technology at any meaningful premium remains constrained in the current environment, which means a genuine fundamental recovery may take time to translate into share price performance.

If you would like to discuss Upwork or how US technology stocks might fit within your portfolio, request a callback or call us on 1300 889 603.