Pro Medicus has delivered another half where the underlying business kept compounding and the market found reasons to sell it anyway. The first half of FY26 saw sales up 28%, EBITDA up 29% and NPAT up 29% on the prior corresponding period, landing at A$125 million, A$94 million and A$67 million respectively once the A$149 million fair value gain on the 4D Medical holding is stripped out. That is still a genuine growth business, but it fell a few percent short of consensus because new contracts are converting to revenue more slowly than expected. The share price has responded in classic Pro Medicus fashion, down 33.5% over three months and 44.4% over six months, and that is where we think the opportunity sits. At the current A$128.80 share price, the stock is trading at a meaningful discount to the 12-month price target of A$250, which implies roughly 94.1% upside on a Buy call.

Research published 19 February 2026. Price target and upside based on prices at time of publication.

About Pro Medicus

Pro Medicus (ASX PME) is an Australian healthcare imaging and informatics company that supplies its Visage 7 platform, along with radiology information system software and services, to hospitals, imaging centres and health networks. Its operations are concentrated in the United States, with a smaller footprint in Australia and Europe. The company is cloud-native in a market still dominated by legacy on-premise Picture Archiving and Communication Systems, and its competitive edge has consistently come down to two things that radiology customers care about, speed of image rendering and the operational advantages of a true cloud architecture. Pro Medicus is listed on the ASX with a market capitalisation of roughly A$14.7 billion. More information at promed.com.au.

The 1H26 Result in Context

The headline miss was always going to get the most attention. Revenue and EBITDA came in 4% to 5% below consensus, and that is what moved the stock in the days around the result. It is worth being clear about what actually drove the miss, because the wider thesis is unchanged. Management had laid out a schedule of large contract go-lives, and several of those slipped by a few months into the back half and into FY27. In a business where a single Trinity cohort can swing an annual number by tens of millions, the phasing matters. We do not read this as demand weakness or pricing pressure, and there was nothing in the result that pointed to churn. The pipeline is actually the strongest it has been, with the company making more sales in the last six months than it did across a full twelve months two years ago.

The margin picture is a similar story. EBITDA margin moderated to 75.1% in 1H26, down 275 basis points from the 77.9% printed in 2H25. The moving part here is reinvestment. Pro Medicus has been actively adding headcount and keeping the research and development budget running hot to support a larger implementation pipeline and to fund the build out of its adjacent products. That is not a margin we would want to see drift lower indefinitely, but in the context of a company still growing the top line at 28% and carrying net cash, a couple of hundred basis points of margin given back to build the next leg of growth is the right trade.

Contract Momentum Is the Real Story

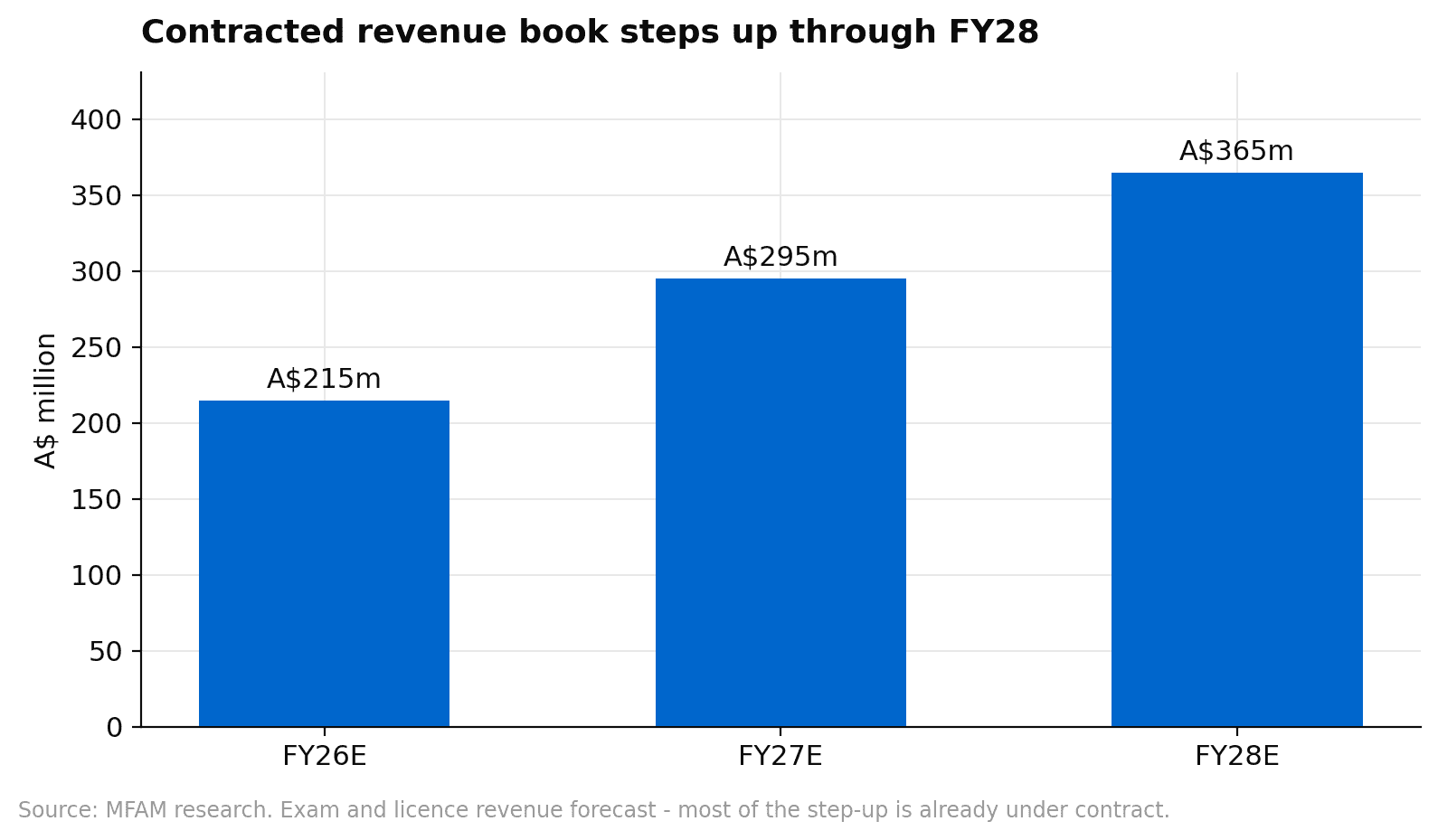

If you strip the result back to what actually matters over the next two years, it is the contract backlog and the rate at which it is converting to revenue. Four of the five Trinity Health cohorts are due to complete implementation by the end of FY26, with full run-rate flowing through in FY27. That alone is a material step up in the US footprint. Layered on top of Trinity is a set of new implementations scheduled through 2026 including UC Health, which adds both radiology and cardiology components, the Franciscan Missionaries of Our Lady Health System, the University Hospital Heidelberg expansion, Advanced Radiology Management, Roswell Park Comprehensive Cancer Center, Children’s of Alabama, Vancouver Clinic and the BayCare number two contract. The aggregate exam and licence revenue book is forecast to step up from around A$215 million in FY26 to A$295 million in FY27 and A$365 million in FY28, and most of that is under contract rather than hoped for.

The Veterans Affairs work continues to be one of the more interesting slower burn optionalities in the business. The VISN 23 migration is expected to complete by March 2026, and once it is live, it becomes a reference site for the other VA integrated service networks looking to move off legacy PACS platforms. Separately, Pro Medicus remains engaged in a Request for Information process with the US Department of Defense, and if that converts into an award, the scale is significant, on the order of 50 million scans a year. We are not pencilling that in, but it sits as upside to the existing numbers rather than as something that has to work for the thesis to play out.

The other underappreciated piece here is the North American contract win cadence. Pro Medicus has comfortably closed the gap on Sectra in North American contract announcements over the last three years, and for the first time is running roughly in line or ahead on new wins. In a market where almost every large health system either has the Visage platform on the evaluation shortlist or has already signed, the compounding effect of each reference customer is significant. Winning at large academic centres like Heidelberg is strategically useful beyond the revenue it adds, because those sites set the template for what a modern radiology stack looks like in their region.

Operating Leverage and the Path Back to Margin Expansion

Pro Medicus runs on a software licence and transaction model with very little cost of goods sold, so revenue acceleration tends to show up quickly in EBITDA margin once the step up in headcount is absorbed. We expect 2H26 margins to recover as the large implementations start contributing full run-rate revenue, and the FY27 EBITDA margin is expected to sit around the 78% level the business reached in 2H25. Free cash flow generation remains strong, with FY26 free cash flow forecast at A$134 million rising to A$257 million by FY28, and the balance sheet carries net cash of roughly A$175 million at the end of FY26. That gives the business the ability to keep reinvesting, to keep paying a modest dividend, and to buy back stock at the board’s discretion, without any real constraint.

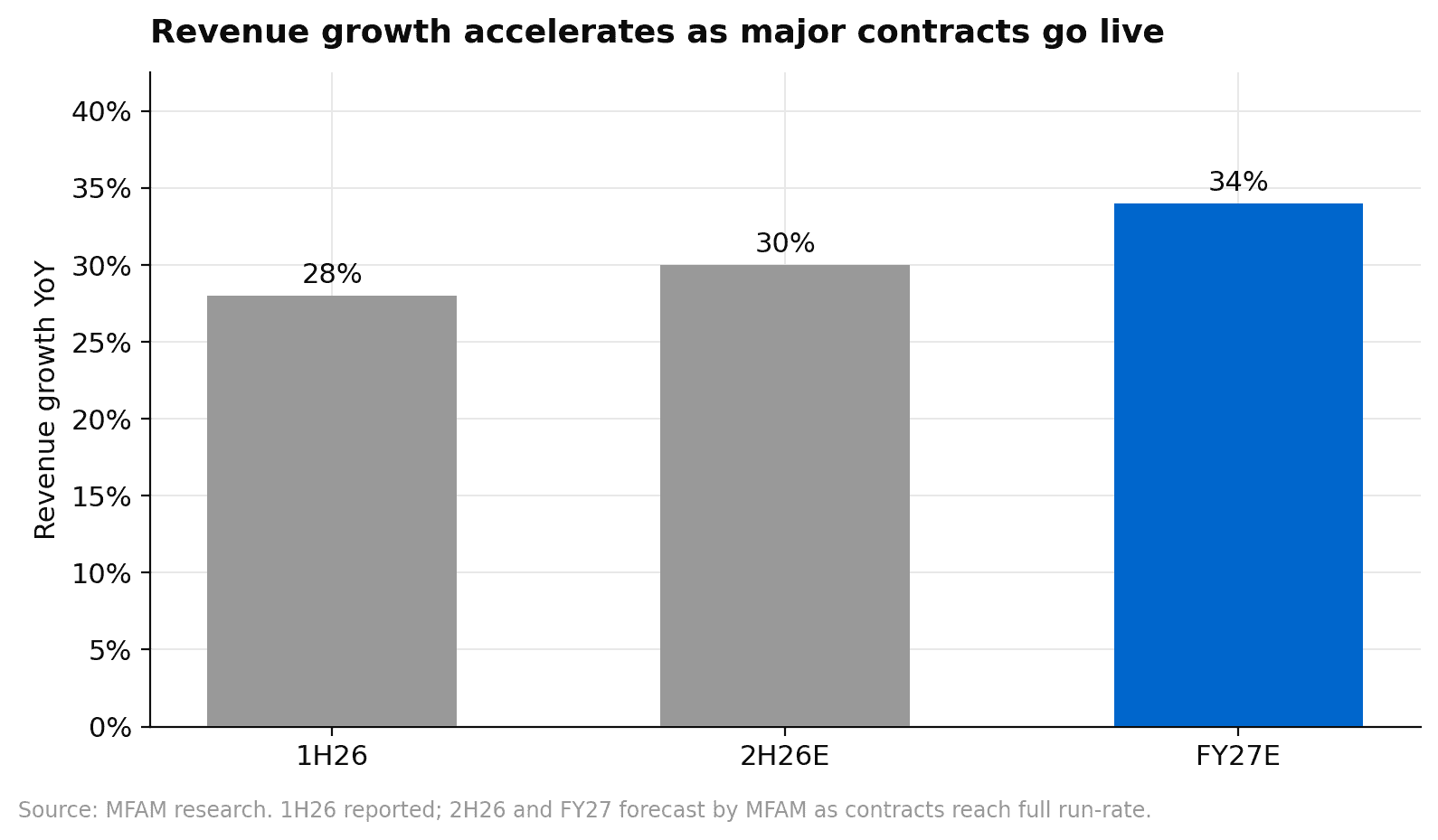

The revenue trajectory in the near term looks like 28% growth in 1H26 stepping up to around 30% in 2H26 and accelerating further to around 34% in FY27 as the major contracts move to full run-rate. That is not a growth rate that is accessible in many places on the ASX, and when it is available it is usually attached to a business with a substantially lower margin profile or a much weaker balance sheet.

Adjacent Growth, AI, Cardiology and Pathology

The three adjacent opportunities are where most of the longer term optionality sits and where the market has been sceptical about execution. On AI, Pro Medicus continues to add capability and has been building a library of algorithms that can run inside the Visage workflow, and the technical work is progressing. Monetisation, however, is still limited, and we would not include material AI revenue in our base case at this stage. The cardiology opportunity is more tangible in the near term, with the UC Health go-live in April 2026 representing the first meaningful combined radiology and cardiology implementation. Cardiology has historically been a fragmented market with weaker incumbents than radiology, and Pro Medicus is entering it with a product that is already credible with the customer base.

Pathology is the third leg and the one that will start contributing first. Management has flagged that the initial client launch is expected within the next few months, and there has been significant interest from the existing radiology customer base. The pathology market has lagged radiology in its move to digital, and the vendor landscape is still unsettled, which is exactly the environment where Pro Medicus has historically done well. None of these three adjacencies need to deliver for the stock to work over our 12-month view, but any of them starting to scale in FY27 or FY28 would support further upside to the price target.

Valuation Has Reset

Pro Medicus has always been expensive, and sensible investors have argued over the right way to value it for years. What is different now is that the multiple has compressed meaningfully. On 12-month forward EV/EBITDA, the stock is trading at around 51 times, roughly 39% below the 5-year average of 80 times or so, and well below the 140 times peak from the back half of 2025. The earnings profile is broadly unchanged, the contract pipeline is arguably stronger now than at any point in the last two years, and the balance sheet is in better shape. In other words, the derating has been driven almost entirely by sentiment and by short term phasing rather than by any fundamental degradation in the business.

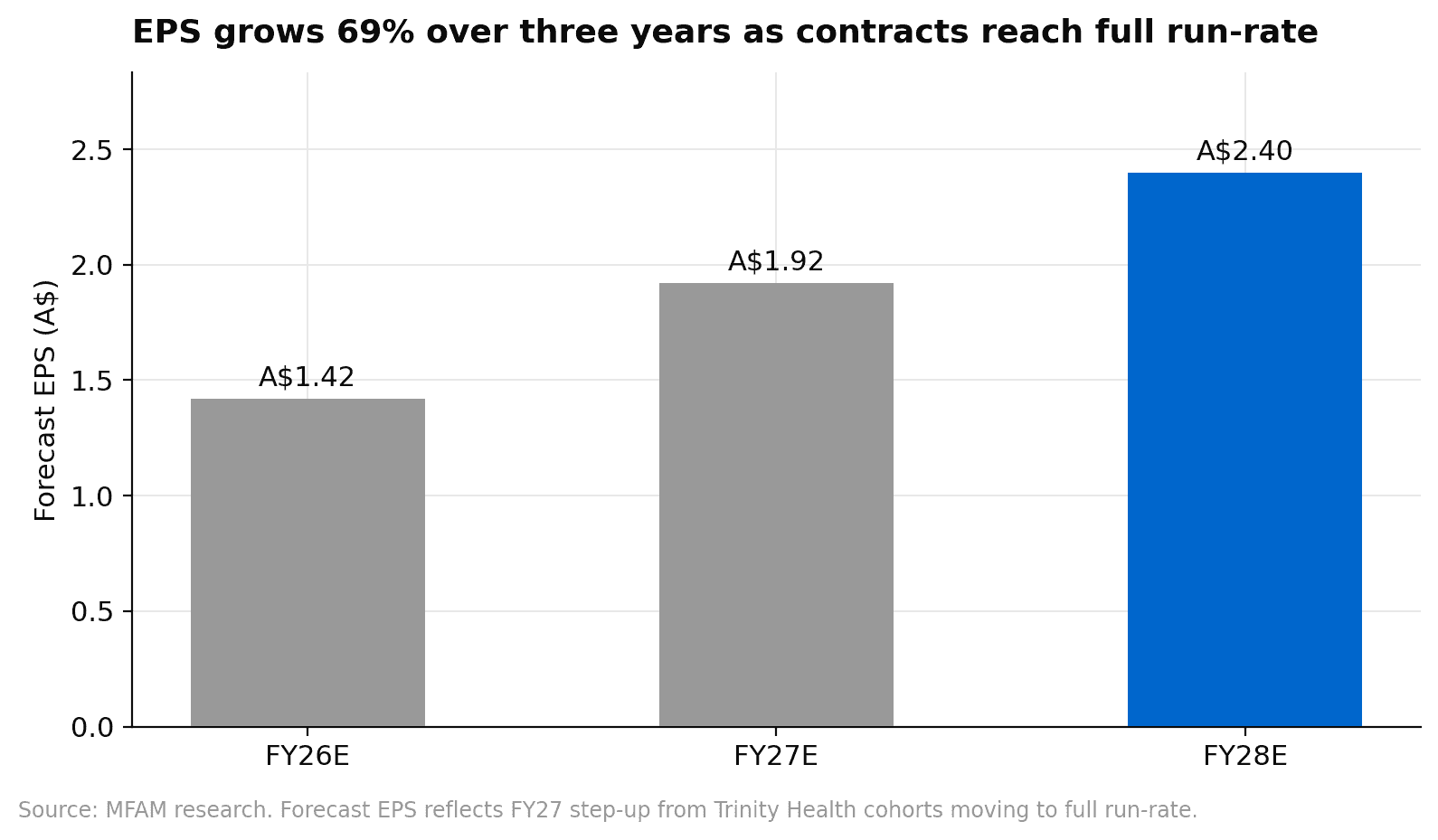

The 12-month price target of A$250 is based on an 85% weighting to a fundamental valuation that works out to A$240 per share, and a 15% weighting to a merger and acquisition valuation at 115 times FY27 EV/EBITDA, which works out to A$305 per share. The forecast earnings per share sits at A$1.42 in FY26, A$1.92 in FY27 and A$2.40 in FY28. On the FY27 number, the stock at A$128.80 is trading on a price to earnings ratio of around 67 times, falling to 54 times on FY28. Those are still premium multiples, but when revenue growth is running at 25% plus, EBITDA margins are sitting at 78% and the return on equity is close to 50%, we think a premium is appropriate and the current price is not demanding it.

Risks We Are Watching

The risk set is concentrated in five areas. The first is a slower pace or smaller size of new contract wins, which would reduce both the pipeline and the reference signalling effect. The second is a failure to scale AI adoption in a way that translates into revenue over the medium term, which would not hurt the 12-month thesis but would matter for the long run multiple. The third is competitor activity narrowing the Visage speed and cloud advantage, with Sectra remaining the most credible alternative. The fourth is a decrease in imaging exam rates across the US health system, which would reduce the transaction linked portion of revenue. The fifth is pricing power, which has held up well so far but which is worth monitoring as the customer base grows and as the market becomes more competitive.

Our View

Pro Medicus is doing what it has always done, winning the large high-profile contracts, reinvesting, expanding into adjacent markets and compounding the top line at a rate very few ASX businesses can match. The 1H26 result did not change our view of the business, and the pull back in the share price since the result has given us a more attractive entry point than we have seen in a long time. At 51 times forward EV/EBITDA the stock is trading roughly 39% below its 5-year average, the earnings are still growing strongly, and the contract backlog coming online over 2H26 and FY27 gives us confidence in the growth trajectory. The rating stays at Buy with a 12-month price target of A$250, implying roughly 94.1% upside from the current A$128.80 share price.

If you would like to discuss Pro Medicus or any other stock in more detail, you can book a time at our call back page or phone us on 1300 889 603.