Today, we will look at why Ramsay Health Care shares (ASX:RHC) has good revenue growth potential as the world heads towards a post-lockdown future in our RHC share price forecast.

Ramsay Health Care (ASX:RHC) is one of the world’s largest private hospital chains.

The company has been of interest to the markets due to the spike in the number of hospital patients resulting from the pandemic.

Its recently released full-year FY21 results impressed with record performance, despite lost revenue from elective surgeries, which have higher margins than COVID-related services.

We first looked at Ramsay Health Care shares back in early September 2018. Since then, the RHC share price has gained around 28% and paid quite a few dividends, including during the pandemic when dividends for many companies were cut or suspended.

At the current RHC share price, Ramsay Health Care shares have returned 9.13% YTD, compared to 11.09% for the index.

About Ramsay HealthCare (ASX:RHC)

As mentioned, Ramsay Health Care (ASX:RHC) is one of the world’s largest hospital chains with a presence across Europe, Asia, the UK, and Australia.

The company focuses on private sector surgeries, rehabilitation, and psychiatry.

In total, RHC has more than 500 hospitals in operation with over 80,000 employees.

Its biggest markets by revenue, in descending order, are Europe, Australia, UK, and Asia.

At the current RHC share price, Ramsay Health Care shares have a market capitalization of A$15.6 billion.

Strong Pent-Up Demand To Drive Earnings In FY22

Although Ramsay Health Care (ASX:RHC) suffered losses from a drop in elective surgical patients and other elective non-surgical activities throughout FY21 (mainly from mid-March to August), the company still reported record performance during the year.

This was due to the full utilization of its resources for the treatment of COVID patients throughout Asia, Europe, the UK, and Australia.

Largely, the group reported revenue increases in all jurisdictions apart from the UK, and even their government grants for use of its facilities offset the shortfall.

While the spread of the delta variant across all its jurisdictions will hurt elective surgical and non-surgical volumes in FY22, Ramsay’s business is largely very resilient and is expected to perform moderately better than FY21 even in the worst case.

Data from the company shows significant pent-up demand existing for elective surgical and non-surgical patients due to lockdowns, the focusing of resources on COVID, and general public aversion of hospitals.

In Australia, elective surgical and non-surgical volumes were up 7%-15% and 3% respectively during FY20, on pre-pandemic levels, thus reflecting pent-up demand.

In FY22, the company’s UK operations will benefit from the increase in capacity from three new facilities completed over the last year.

The new capacity can be used to increase market share from pent-up demand for elective procedures.

The company’s patient volumes in Europe in 2HFY21 were significantly above its usual market share, particularly for general critical care due to COVID.

Ramsay Health Care (ASX:RHC) also estimates that elective procedures in European regions have big backlogs and the company will, therefore, focus on increasing its market share over the next year.

These trends have helped the company build a strong relationship with local governments and likely fortified its market position.

Overall, while the company suffered a loss in volumes from elective procedures, it performed admirably throughout the pandemic both financially and operationally as a support operation to public healthcare systems in its jurisdictions.

Coming out of the pandemic, it is well placed to benefit from the return of demand for elective procedures.

Workforce Exhaustion and FX a Potential Weakness

A potential weakness of the company is that its workforce is exhausted and depleted from non-stop services provided since the onset of the pandemic.

Over FY22, the company may not be able to cater fully to the resurgent demand for elective procedures due to significant staff fatigue.

Notably, Ramsay Health Care’s (ASX:RHC) significant business operations outside Australia expose it to currency risks due to potentially adverse volatility in exchange rates between the Australian dollar (Ramsay’s reporting currency) and the foreign (operational) currencies.

Significant Growth Opportunities Ahead Due To Strong Balance Sheet and Reputation

The stress caused by the pandemic on healthcare systems around the world has spurred monumental interest from governments who have become aware of the gaps in public healthcare systems.

Already budget-constrained, they are now looking to fill them through the invitation of private investment in healthcare, or public-private partnerships.

For example, countries like Thailand, India, Saudi Arabia, Qatar, developing African nations, and Bangladesh are actively courting foreign investors/companies to help build resilient healthcare systems for them.

COVID has been devastating in Indonesia and Malaysia, where the company operates under a JV and has highlighted the need for additional healthcare capacity.

These countries are populous and the company has built a strong relationship with local governments over the tenure of the pandemic.

The tilt towards private-public collaboration in healthcare presents a potentially lucrative opportunity for Ramsay because it has a solid reputation as a global healthcare player and has a strong balance sheet.

Further, the pandemic has laid bare that even some of the countries where Ramsay already operates have huge growth potential and need significant new capacity.

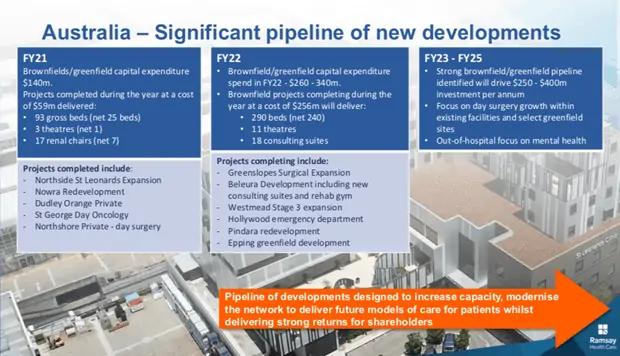

Ramsay Health Care (ASX:RHC) recognizes this and has in place ambitious expansion plans both in Australia and abroad.

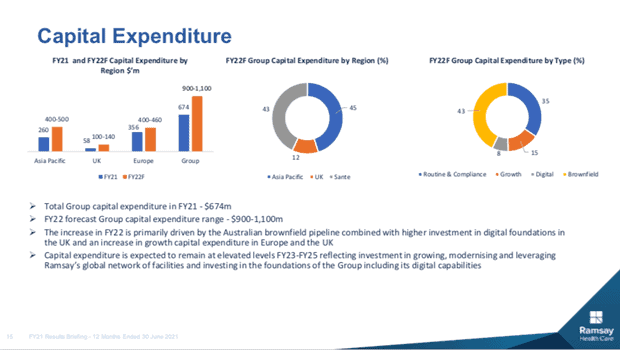

The company has announced plans to spend between A$260 million – A$340 million in FY22 and between A$250 million – A$400 million per year from FY23 to FY25 on green-field/brownfield projects in Australia.

Ramsay Health Care is also actively looking for opportunities in existing and new foreign jurisdictions.

It has earmarked a cumulative total of between A$387 million – A$483 million for brownfield projects in FY22.

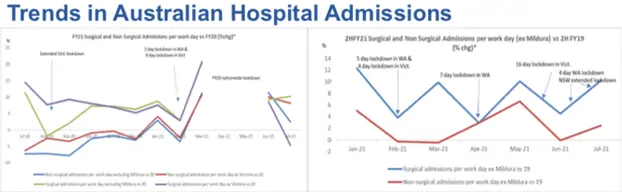

Covid Lockdowns Remain a Threat to Elective Surgeries

At present, a major threat facing Ramsay Health Care (ASX:RHC) is the impact of any potential future lock-downs in jurisdictions where Ramsay operates and their effect on elective procedure volumes.

The suspension of elective procedures in areas such as West Australia, Sydney, and Victoria negatively impact the company’s financials.

For example, the latest lockdowns cost the company in the region of A$13 million of EBIT just in July and last year’s 90-day restriction on elective surgeries in Victoria cost the company A$70 million in EBIT.

Hence, vaccination and containment of the virus are key to the company’s financial performance in FY22.

Given that the pandemic is worsening in Australia, the outlook for RHC is getting somewhat murkier in the short to medium term.

However, there is light at the end of the tunnel as Australia’s vaccination rates continue to climb.

With the government plan for us to live with the virus rather than locking down again, the direction Australia is headed in should be a net positive for Ramsay Health Care shares.

In other jurisdictions, while Europe has done better than most Asia-Pacific countries in terms of virus containment, the risks still exist.

However, the availability of healthcare personnel is a matter of concern given the enormous strain from the past 15 months.

Critical staff may be infected in the resurgent pandemic and they may need to be supplemented by more expensive people – this could be a financial issue particularly when, as expected, elective procedures and elective surgeries come back with a rush, post-pandemic.

It is undeniable that Australia is paying an economic toll due to the pandemic.

Business shutdowns and rising joblessness could make private health insurance unaffordable for large swathes of people, and this could affect Ramsay’s revenues.

As yet unquantified, there is a definite shift towards telehealth, and this could be a threat for Ramsay Health Care shares if the trend intensifies.

Ramsay Health Care (ASX:RHC) Financials

Last April, amidst the first wave of the pandemic, Ramsay Health Care raised A$1.5 billion through an institutional placement to ensure its financial strength during the emergent situation.

This has helped the company lower its net debt levels and financing costs over the past year.

In FY21, the company reported group revenue of A$13,332.3 million, up 7.3% (YoY); direct revenues from clients rose 3.88% to A$12,435.5 million, and revenue from government contracts/grants surged 101% to A$857 million.

The company reported an EBIT of A$1132.6 million, +29% YoY, and a net profit after tax of A$511.5 million, +65.4%.

The biggest growth in earnings was driven by the UK, +83.4% YoY, followed by Europe, +38.3% YoY, and then APAC, +18.9% YoY.

Over the year, the company paid a dividend of A$1.515 per share, a mammoth 142% higher than last year.

At the current RHC share price, Ramsay Health Care shares have a dividend yield of 2.22%.

The company has given no guidance for FY22 due to the uncertainty around the pandemic.

However, given Australia’s current state of lockdowns, its profitability is likely to be affected.

The company has planned a Capex of A$900 million – A$1100 million during FY22, the bulk of which is planned for brownfield expansions.

We compare Ramsay Health Care shares (ASX:RHC) to Healius Ltd. (ASX:HLS), an Australian company that owns healthcare business across a variety of formats, and Mediclinic (LON:MDC), a UK-based international hospital chain operator.

| Metric | RHC | HLS | MDC |

|---|---|---|---|

| Price/Earning Ratio | 37.69 | 45.54 | 34.89 |

| Net Profit Margin | 3.89% | 3.49% | 2.64% |

| Return On Equity | 11.32% | 3.5% | 2.37% |

| Asset Turnover | 0.66 | 0.45 | 0.44 |

| Dividend Yield | 2.22% | 2.73% | – |

At the current RHC share price, Ramsay Health Care shares are cheaper than Healius but marginally more expensive than Mediclinic in terms of P/E multiple.

However, it has a higher net profit margin and significantly higher return on equity than both its peers.

The company is also more capital efficient than both Healius and Mediclinic – apparent from its nearly 50% higher asset turnover – an important metric in a capital-heavy business like healthcare.

While Ramsay Health Care shares’ dividend yield at the current RHC share price is slightly lower than Healius, Ramsay enjoys a larger size and better operational metrics.

Mediclinic doesn’t pay a dividend, so clearly, the advantage lies with Ramsay.

COVID Has Bolstered The Outlook For Healthcare In The Long Term

The pandemic has made it clear that across the globe, healthcare needs to be expanded and prepared for more such unfortunate events.

The long-term outlook for Ramsay Health Care shares (ASX:RHC), both at home and abroad, is therefore secure.

In the shorter term, the impact on the company’s profitability due to postponement/cancellations of outpatient visits/elective procedures/elective surgeries is negative.

However, as vaccinations gather pace, people are expected to lay aside their apprehensions and “get it over with.”

Ramsay’s stock is currently on a downtrend, but this may be an opportunity to enter on declines and add a somewhat recession-proof and dividend-paying flavour to a portfolio.