Seek is the dominant Australian online recruitment, employment and training advertiser.

The company is growing its revenues strongly year on year and dividends have been steady as the company matures.

With a strong, entrenched and dominant business, Seek is a good blue-chip, longer-term investment which should see continued revenue growth.

About SEEK Limited (ASX SEK)

SEEK Limited (ASX SEK) is a publicly listed Australian company that focuses on the online employment and training market. It was founded in 1997, but its operations now span Australia, New Zealand, China, South East Asia, Brazil, Mexico, Africa, and Bangladesh.

SEEK makes a positive impact on employment on a truly global scale, operating in a total of 18 countries with market-leading positions in 14 countries.

SEEK Limited derives revenue from online advertising such as employment classifieds, occupational training, and higher education courses.

Group sales revenue increased in FY19 by18% from $1299.5 million to $1537.3 million. It is targeting a growth rate of 15-18% in 2020, according to the latest guidance.

Further, the company’s total EBITDA grew by 6%, and post-tax net profits increased by 245% compared to FY18.

For 2020, EBITDA is forecast to grow by 8-11%, while post-tax net profit is likely in the range of $145 – $155 million.

SEEK’s Strategy

SEEK divides its operations into three broad categories: its core Australia and New Zealand online employment marketplace, international operations, and education-related operations.

The conpany creates product technology solutions to match job seekers and hirers. SEEK Learning offers trusted advice concerning career-related education. SEEK Volunteer is the largest single source offering not-for-profit volunteering opportunities in Australia and New Zealand.

SEEK earns revenue from job advertisements, CV search/download, education services, other recruitment services, etc.

During FY19, the company made strategic investments resulting in strong revenue growth. This trend was witnessed in Chinese subsidiary Zhaopin and across the company’s investment portfolio.

In FY19, Zhaopin achieved stellar revenue growth of 34% in a competitive market. Also, Early Stage Ventures (ESVs) achieved strong growth and operational metrics.

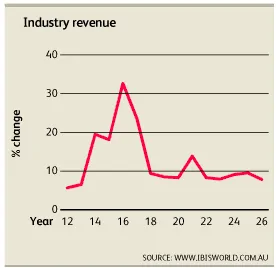

Industry Analysis

Internet Publishing and Broadcasting in Australia expanded rapidly over the past five years and is projected to grow at an annualized 16.1% over the following five years to $4.1 billion.

Major players in the online advertising market have expanded, and online video streaming has become increasingly popular, driving the growth of the industry.

The Internet Publishing and Broadcasting industry is in a growth stage. Consumers are increasingly using the internet for their everyday needs. Strong smartphone penetration over the past five years has further boosted internet usage.

The growing popularity of smartphones is leading to higher demand for internet access and thereby assisting growth.

Broadband provider NBN may provide faster connectivity to handle high data usage.

These are factors working in favour of the industry.

Global broadband connectivity and increasing affordability of ICT (information and communications technology) products are expanding the industry.

Further, the advertising segment is growing rapidly due to its low-cost and value proposition. These factors are projected to drive further growth in this industry.

However, advertising revenue has flown overseas due to the dominance of Facebook and Google, which are both foreign entities.

This trend has pressured advertising prices as firms compete to gain revenue from marketing. As a result, industry profitability has declined.

However, these advertising platforms are not focused on recruitment advertising. In addition, recruitment advertising is highly localised.

Therefore, the effect of foreign entity penetration of the Australian advertising market is minimal and Seek is able to keep its dominant position in this uniquely localised sector.

Advantages and Risks

Market opportunities

- Dominant position. SEEK is a dominant player in the industry; hence, it is difficult for new entrants to gain market share. SEEK has consolidated its market position over the past five years and become a central hub for jobs-related advertising. As a result, it has gained a major share of web traffic for job advertisements. This factor further incentivizes consumers to use SEEK’s websites and businesses for advertising.

- Zhaopin’s strong revenue growth. SEEK’s Chinese subsidiary Zhaopin achieved strong revenue growth of 34% in FY19. The website is the largest and most popular Chinese job portal. Its rapid growth within a huge market is a major business advantage to SEEK.

Following the development of high speed Internet, the market size of the online recruitment industry in China has shown steady growth.

According to Analysys data, China’s Internet recruitment market grew at a rate of over 20% in 2017-2018.

The online recruitment industry market is, therefore, a valuable market opportunity as more job seekers go online.

Accordingly, SEEK’s subsidiary Zhaopin is likely to contribute strongly to SEEK’s growth and profitability.

Potential Risks

- Increasing competition. The Internet Publishing and Broadcasting industry have very low barriers to entry. For SEEK, the ease with which entrepreneurs can now start up an online business is a matter of concern. Unsurprisingly, the increasing competition will drive down the price of advertising slots. However, due to Seek’s dominant position, it will be hard for new competitors to take market share unless there is a very significant investment in building an initial client base.

- Macro concerns. Slowing global growth has a severe impact on the job market. Global growth is under a cloud from the seemingly endless U.S. – China trade wars. SEEK has already warned that near-term in China weak macro conditions will impact its financials.

Financial Performance and Peer Comparison

SEEK’s performance:

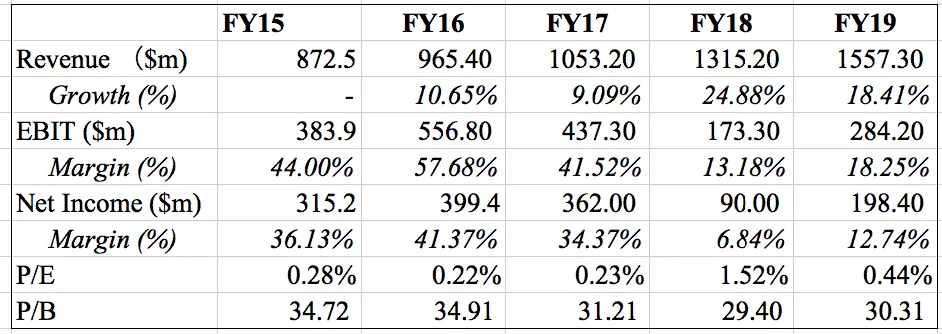

As seen from the above table, the company’s Revenue showed an upward trend over the past five years. However, EBIT and Net Income suffered a significant decline in 2018 due to impairment losses and other one-off items aggregating $179.5 million.

This decline was followed by a slight increase in these metrics in 2019.

Seek is also paying a dividend yield of about $0.65 per share and has held this steady in the past 3 years. If revenues continue to grow and if they can continue to increase their margins, we should expect dividends to also grow.

Peer comparison

A similar player in this industry is the REA Group (ASX REA), an online property advertising services.

From the table, REA group had higher profit margin (26.00% versus 12.74% of SEEK) and EBIT margin (26.83% versus 18.25%) but lower revenue growth (8.50% versus 18.41%) in FY19.

The data indicates that SEEK has higher revenue growth. However, REA has relatively better profitability.

However, keep in mind that both these companies serve completely different target markets and are not competitors.

Conclusion

SEEK provides technological products to satisfy the needs of both job seekers and hirers.

Its dominant position and positive results from subsidiary Zhaopin would support continued growth and expansion.

The industry experienced strong growth over the past five years. This trend is expected to continue in the future due to rising internet usage and internet accessibility.

In particular, Seek looks to be increasing their margin’s and accelerating growth through expansion into China.

However, due to increasing competitive pressure, both from domestic as well as global companies, profit margins could continue to come under pressure and is something to be wary of.