Institutional sell-side rates WEB Travel Group a Buy with a 12-month price target of A$4.70. The stock closed at A$2.23 on 20 May 2026, implying roughly 111 per cent upside to that target. The bull case rests on three pillars: the hotel bed wholesaling sector is growing at double-digit rates across every major player and WEB is keeping pace; near-term headwinds from the Middle East conflict and a strong Australian dollar are cyclical rather than structural; and the stock is trading at less than half its historical valuation multiple, pricing in a permanent impairment that the underlying business does not support.

Research published 25 May 2026. Price target and upside based on prices at time of publication.

About WEB Travel Group

WEB Travel Group operates WebBeds, a global B2B accommodation platform that sits between hotels and the travel providers that sell those rooms to end customers. Those travel providers include online travel agencies, traditional travel agents, airlines and tour operators, and WebBeds connects them to hotel inventory across the world. WEB was part of Webjet Limited until the 2024 demerger split the business into two separately listed companies, with WEB taking the B2B wholesale operations and Webjet Group (ASX: WJL) retaining the consumer-facing business. WEB is now the world’s second-largest B2B accommodation provider by volume, sitting behind only Expedia’s B2B segment. The company has a market capitalisation of around A$813 million, is listed on the ASX, reports to a 30 June financial year end, and operates globally from its headquarters. More information is available at webbedsgroup.com.

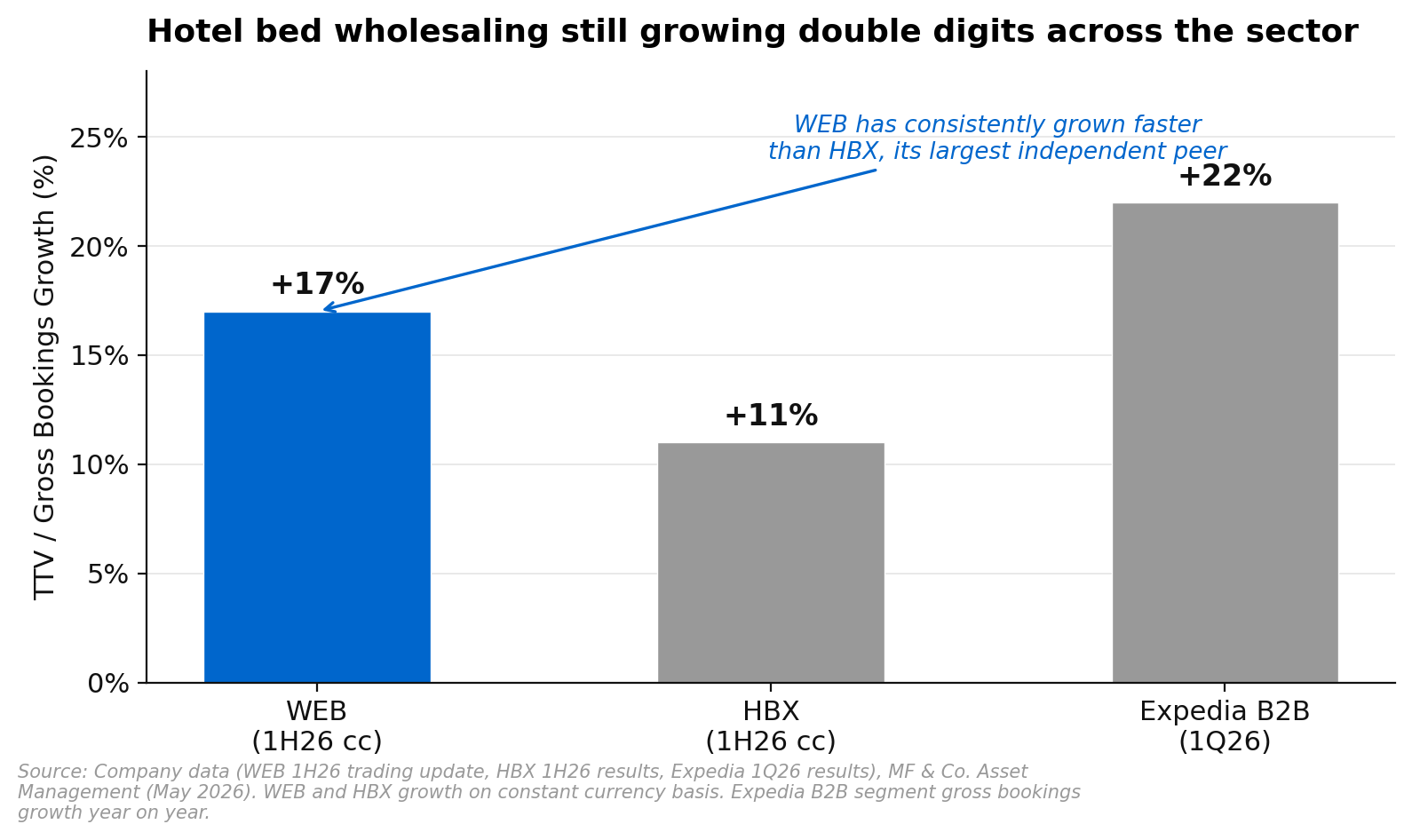

Hotel Bed Wholesaling Is Growing Faster Than Peers

The hotel bed wholesaling sector is in a genuine structural growth phase, and WEB is participating fully in it. WEB posted 17 per cent constant-currency total transaction value growth in the first half of FY26, which sits comfortably alongside what its direct peers are reporting. HBX, the other major listed bed bank, is guiding to 11 to 17 per cent constant-currency growth for the full year and delivered 8 to 19 per cent growth across its reporting periods. Expedia’s B2B segment grew gross bookings by 22 per cent in the first quarter of 2026. Every major player in this niche is compounding at double-digit rates, which tells you the growth is being driven by something structural, not just one company taking share.

WEB has consistently grown faster than HBX over time, which makes the current valuation gap puzzling. WEB trades at roughly a 40 per cent premium to HBX on forward earnings, compared to a historical average premium of around 65 per cent. The market has compressed that premium at exactly the moment WEB’s growth trajectory remains intact. That kind of dislocation tends to close as results confirm the underlying business is still performing.

Near-Term Headwinds Are Temporary

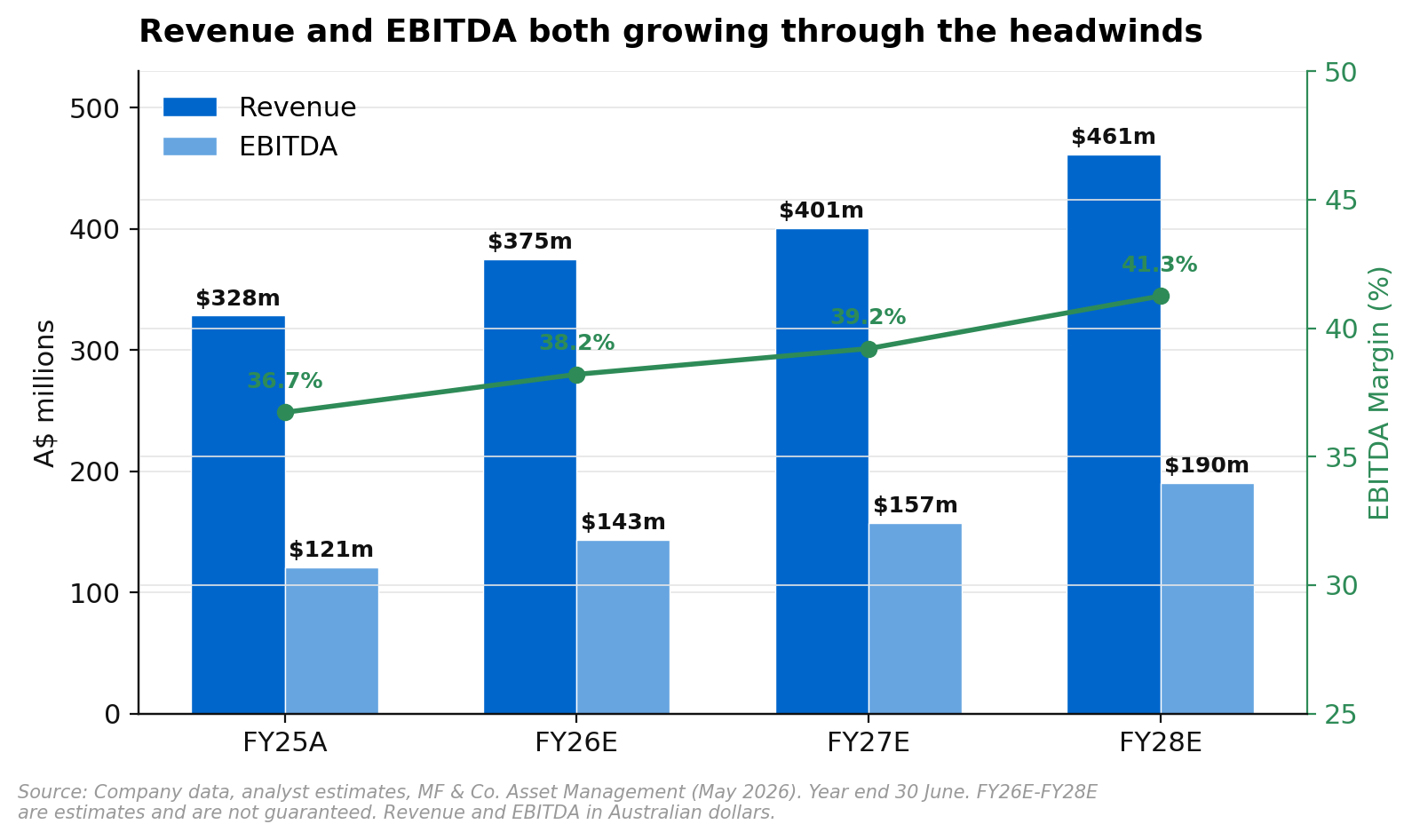

Two factors are weighing on near-term estimates and the stock has sold off to reflect them. The first is the Middle East conflict. Dubai occupancy is running at around 10 per cent in the second quarter of 2026, down from 80 per cent in February, and March occupancy came in at 36.2 per cent compared to 71.4 per cent a year earlier, according to Moody’s Analytics and CoStar data. That is a significant disruption in isolation, but the Middle East represents less than 9 per cent of WEB’s total transaction value. The arithmetic on that means the FY27 TTV drag is roughly 4 per cent at the group level, which is manageable rather than catastrophic. The second headwind is the Australian dollar. WEB earns most of its revenue in US dollars and euros, so a stronger AUD compresses translated earnings even when the underlying business is growing. Institutional sell-side has lowered FY26 to FY28 EBITDA estimates by 6 to 18 per cent to reflect both of these factors.

Neither of these is a structural problem with the business. Travel demand fundamentals remain strong, WEB is continuing to win share in the Americas, and the Middle East will normalise once the geopolitical situation stabilises. The catalysts for a re-rating are straightforward: continued Americas share gains showing up in results, a recovery in Middle East travel volumes, and the resolution of a small accounting matter that has added noise to recent reporting. None of those require anything heroic to materialise.

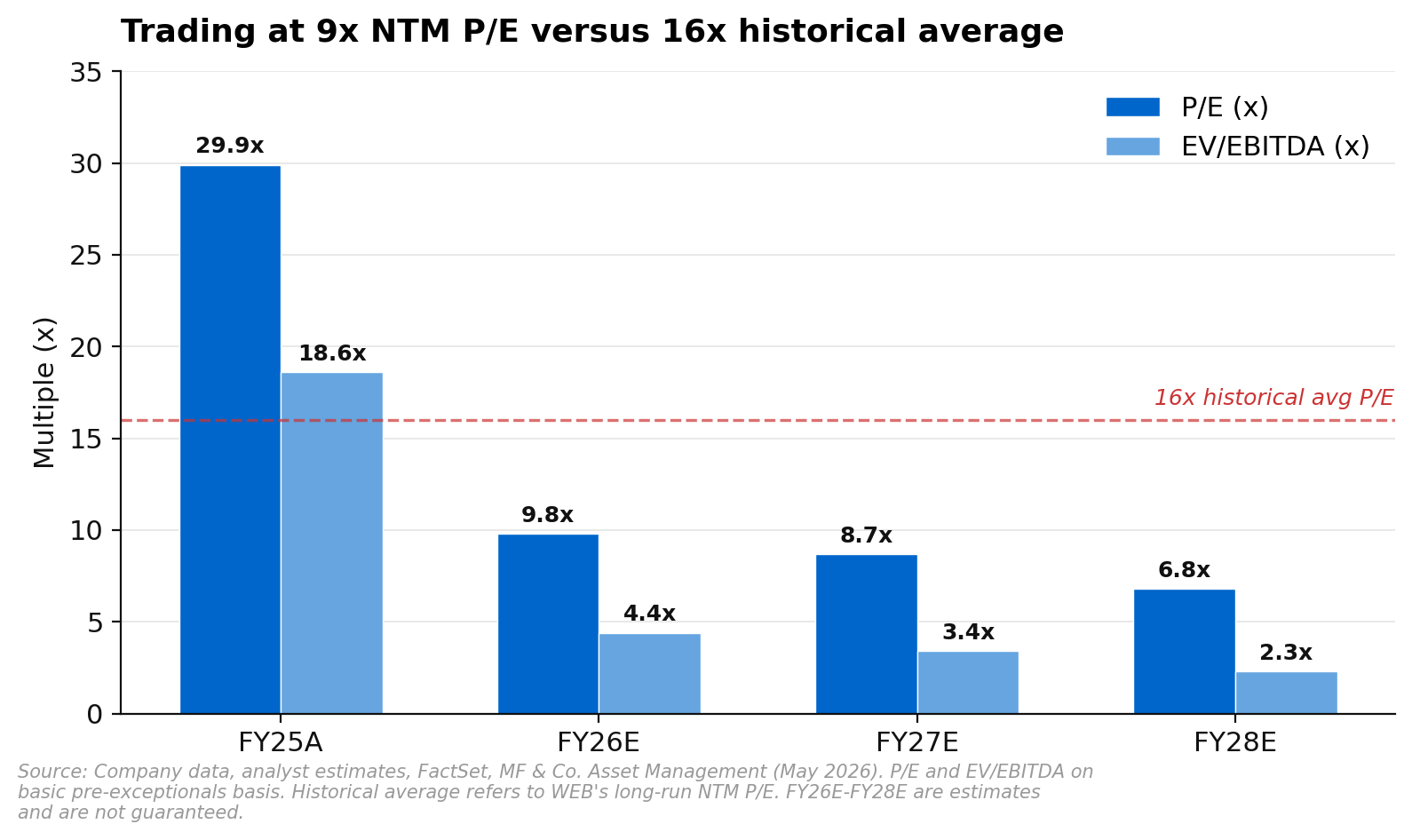

Valuation Is Deeply Discounted to History

WEB is trading at 9 times next-twelve-months earnings against a historical average of 16 times. On an EV/EBITDA basis the stock compresses from 4.4 times in FY26 to 2.3 times by FY28 as earnings grow into the current price. These are not the multiples of a business with a structural problem. They are the multiples of a business the market has decided to treat as impaired.

The institutional sell-side price target of A$4.70 is built from two components. The fundamental value piece applies a FY27 EV/EBITDA of 9.0 times to A$151 million of WebBeds EBITDA, arriving at an enterprise value of A$1,360 million. Subtracting net debt of A$176 million at June 2026 gives an equity value of A$1,536 million, or A$4.21 per share. That component carries 85 per cent of the target weight. The remaining 15 per cent reflects the theoretical M&A value of the asset at 17.0 times EV/EBITDA, which implies A$7.50 per share. Blended together, the 12-month target is A$4.70. At the current price of A$2.23, the market is effectively pricing in a permanent impairment of the Middle East business and giving zero credit to the Americas growth that is already showing up in results.

Risks to the Buy Call

A sharper-than-expected consumer spending slowdown driven by global macro uncertainty would reduce travel volumes across WEB’s customer base and compress TTV growth. Revenue margin could come under pressure if competition between bed banks intensifies or if the mix shifts toward lower-margin bookings. Hotels accelerating direct booking initiatives and bypassing wholesalers entirely would reduce the addressable market over the longer term, though this risk has existed for years without meaningfully denting bed bank growth rates. A prolonged Middle East conflict that extends beyond current estimates would mean the 4 per cent TTV drag runs for longer than the market is already pricing. And continued Australian dollar strength would continue to suppress translated earnings even if the underlying USD and EUR revenue lines are growing.

Our View

Institutional sell-side has WEB Travel Group at a Buy with A$4.70 of fair value, built from a blend of fundamental EV/EBITDA and theoretical M&A. The stock is at 9 times forward earnings with a clear path to 7 times by FY28. The sector it operates in is growing at double digits across every major player. The two things weighing on near-term estimates are a regional conflict affecting less than 9 per cent of TTV and a currency headwind, neither of which touches the underlying growth engine of the business. The stock has fallen from above A$7 in late 2024 to A$2.23 today, and the market is pricing it as though something is permanently broken. The numbers do not support that conclusion. The swing factor is how quickly Middle East travel normalises, but even setting that aside, the Americas growth trajectory and expanding margins should be enough to drive a re-rating from here over the medium term. The risk-reward at current levels looks compelling.

If you would like to discuss WEB Travel Group or how it might fit within your portfolio, request a callback or call us on 1300 889 603. The above is general advice and does not consider your individual circumstances. Past performance is not a reliable indicator of future returns.