Aristocrat Leisure used its 2026 Investor Day to set out how it turns its Interactive arm into a billion-dollar business, and the plan is credible enough that we are staying with the stock. This is no longer the cheap re-rating candidate it was a few months ago. The shares have run from the mid-forties in May to around A$61.40, so the easy value has been captured, and what is left is a quality compounder whose fastest-growing engine is only now hitting its stride. Institutional sell-side research has the stock rated Buy with a 12-month price target of A$70.00, nudged higher after the Investor Day, implying around 14 per cent upside from the recent close of A$61.40. The near-term upside is more modest than it was, but the multi-year story, led by the scaling of real-money gaming and iLotteries in the United States, has if anything strengthened.

Research published 6 July 2026. Price target and upside based on prices at time of publication.

Table of Contents

About Aristocrat Leisure

Aristocrat Leisure Limited is a global gaming company and one of the largest suppliers of game content and technology to the industry. It operates through three arms. Land-based Gaming designs and supplies the games, cabinets and systems that sit on casino and club floors around the world, where Aristocrat is the clear market leader in premium content. Product Madness is its social casino business, a portfolio of free-to-play mobile games monetised through in-app purchases. Interactive is the real-money online gaming and iLottery arm, the smallest of the three today but the fastest growing. The company carries a market capitalisation of roughly A$39.5 billion, is listed on the Australian Securities Exchange and reports in Australian dollars on a 30 September fiscal year. Having sold its Plarium mobile-games unit, Aristocrat has refocused on its core competency of slot content, and its investor materials are available on the company’s investor relations page.

Interactive Is Inflecting Toward a Billion-Dollar Business

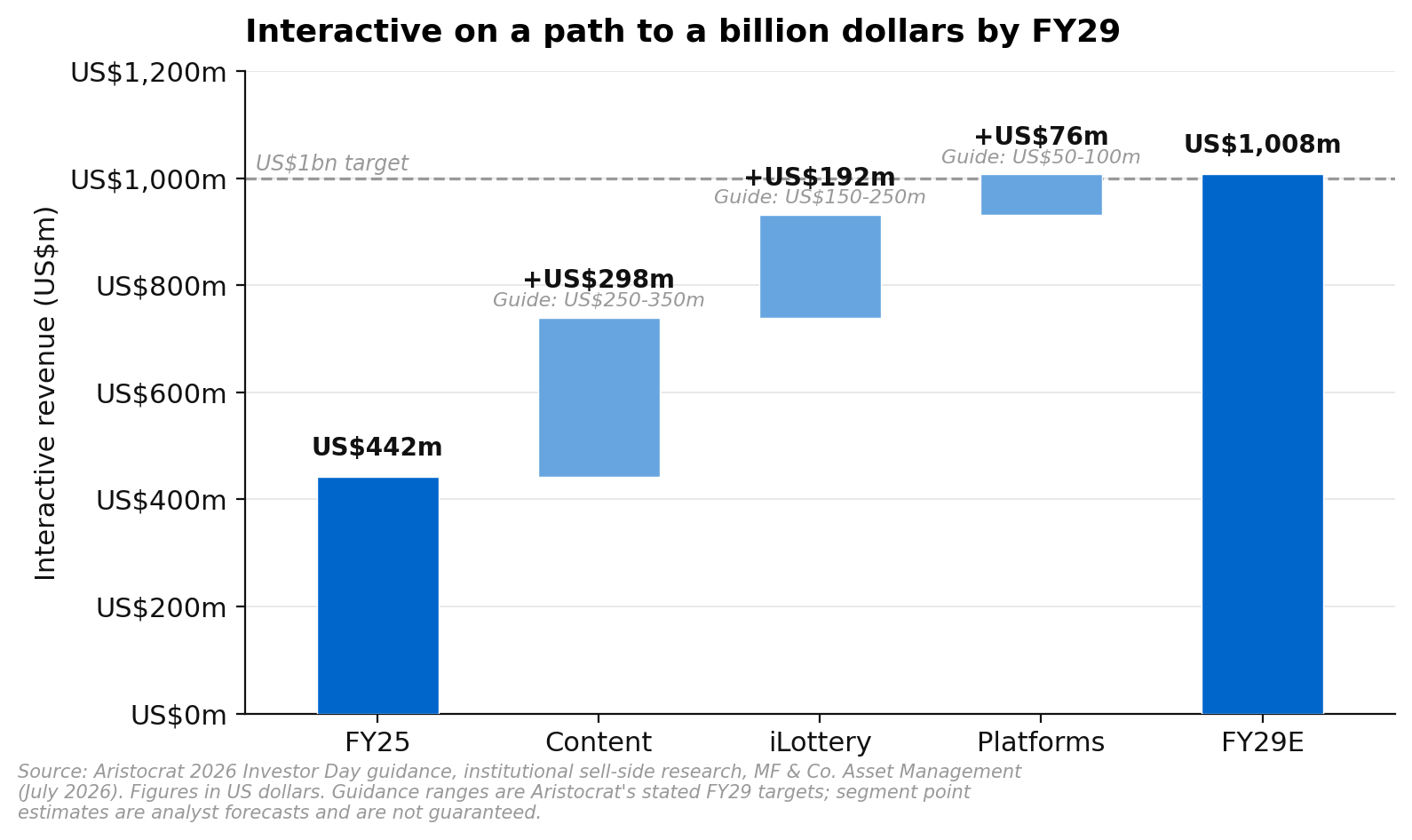

The centre of the Investor Day was Interactive, and the headline is a target of around one billion US dollars of revenue by the 2029 financial year, up from a little over four hundred million in FY25. Management laid out three building blocks to get there. Content, meaning the online slot games Aristocrat licenses to real-money operators, is guided to add between US$250 million and US$350 million. iLottery, where the company runs digital lottery programmes for state lotteries, is guided to add US$150 million to US$250 million. And platform revenue, the technology layer that sits underneath, is guided to add a further US$50 million to US$100 million. The single biggest near-term catalyst is that Lightning Link, one of Aristocrat’s most proven land-based franchises, goes live across all seven legalised online-gaming states this month, which management expects to drive strong share gains from a real-money gaming share of only around four per cent today toward something closer to ten per cent.

What makes this more than a hopeful target is that the market itself is growing underneath the company. Regulated online slot gross gaming revenue in the United States has expanded from well under a billion dollars in 2019 to around eight billion in 2025, and is forecast to keep climbing toward roughly eleven and a half billion by 2029, before counting any upside from additional states choosing to legalise. On the lottery side, Aristocrat has been winning new state contracts, with recent wins in New Hampshire, Massachusetts and Michigan and further bids live in Virginia and North Carolina. The result is that Interactive, which contributes a small share of group profit today, is set to become a materially larger part of the earnings mix over the next several years. This is the part of the story that the market is really paying for.

The cash engine that funds all of this is the land-based Gaming business, and it is still gaining ground. Across North America, Aristocrat holds around sixteen per cent of the installed base, and management believes that can keep climbing toward the higher shares it already commands in more mature segments, where it runs closer to thirty-eight per cent in gaming operations and twenty-seven per cent in outright cabinet sales. The reason it keeps winning is game performance. Aristocrat’s top premium leased games are indexing at 2.73 times the average floor, against 1.86 times for its nearest competitor, and that performance edge has let it capture roughly eighty per cent of new premium units placed over the past seven years.

On top of that base, there are new doors opening. Several US states are expanding into video gaming terminals outside traditional casinos, with Ohio, Missouri, North Carolina and Pennsylvania flagged as potential markets representing a combined opportunity of well over one hundred and forty thousand units. New casino openings in Las Vegas, where Aristocrat typically wins an outsized share of the floor, add further placement growth, and management pointed to a healthy pipeline of new openings and expansions across Europe, the Middle East and Africa. None of this is dramatic on its own, but together it keeps the installed base growing and the recurring gaming-operations revenue compounding, which is exactly what you want the mature part of a business like this to do.

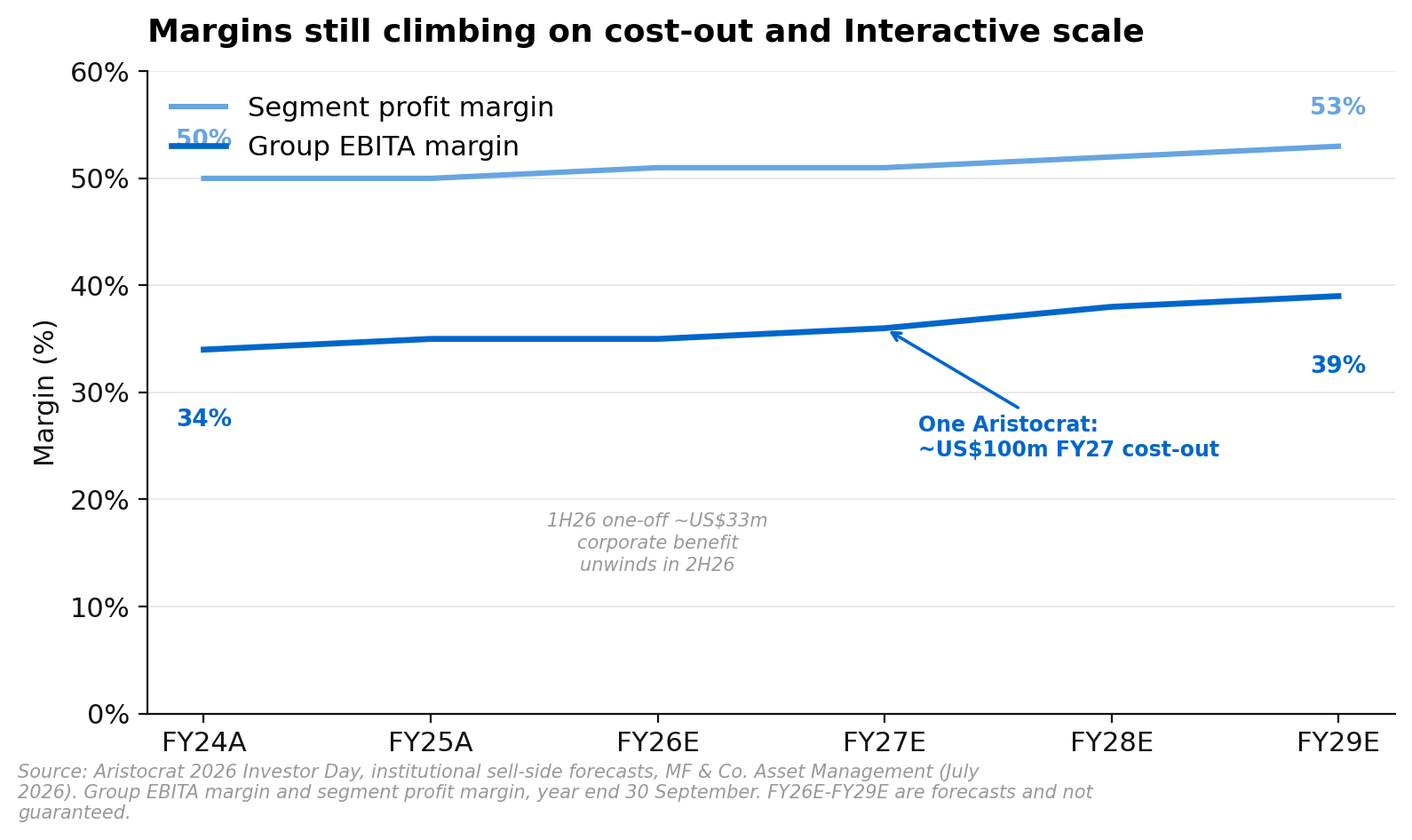

AI and One Aristocrat Do the Heavy Lifting on Margins

The margin story rests on two levers that are both firmly within the company’s control. The first is artificial intelligence applied to game development. In Product Madness, generative AI tools have cut the time to deliver new content to roughly six to eight weeks, against five to six months when that work was outsourced. The clearest evidence is output per head. The number of creative assets the studio delivered grew to about fourteen thousand in 2025 from eight thousand in 2021, and it did so with a smaller design team, roughly one hundred and three designers against one hundred and twenty-eight previously. Faster, cheaper content production feeds directly into both revenue velocity and margin.

The second lever is a cost programme the company calls One Aristocrat, which is targeted to take out around one hundred million US dollars of cost in FY27. Together with disciplined design-and-development spend that is expected to grow more slowly than revenue, these levers are what allow group margins to keep expanding off an already industry-leading base. There is one honest wrinkle to flag. The first half of FY26 carried a one-off corporate cost benefit of about thirty-three million US dollars that unwinds in the second half, so the reported group margin flattens out this year before resuming its climb. Look through that timing effect and the direction of travel is clearly upward.

Valuation and What You Are Paying For

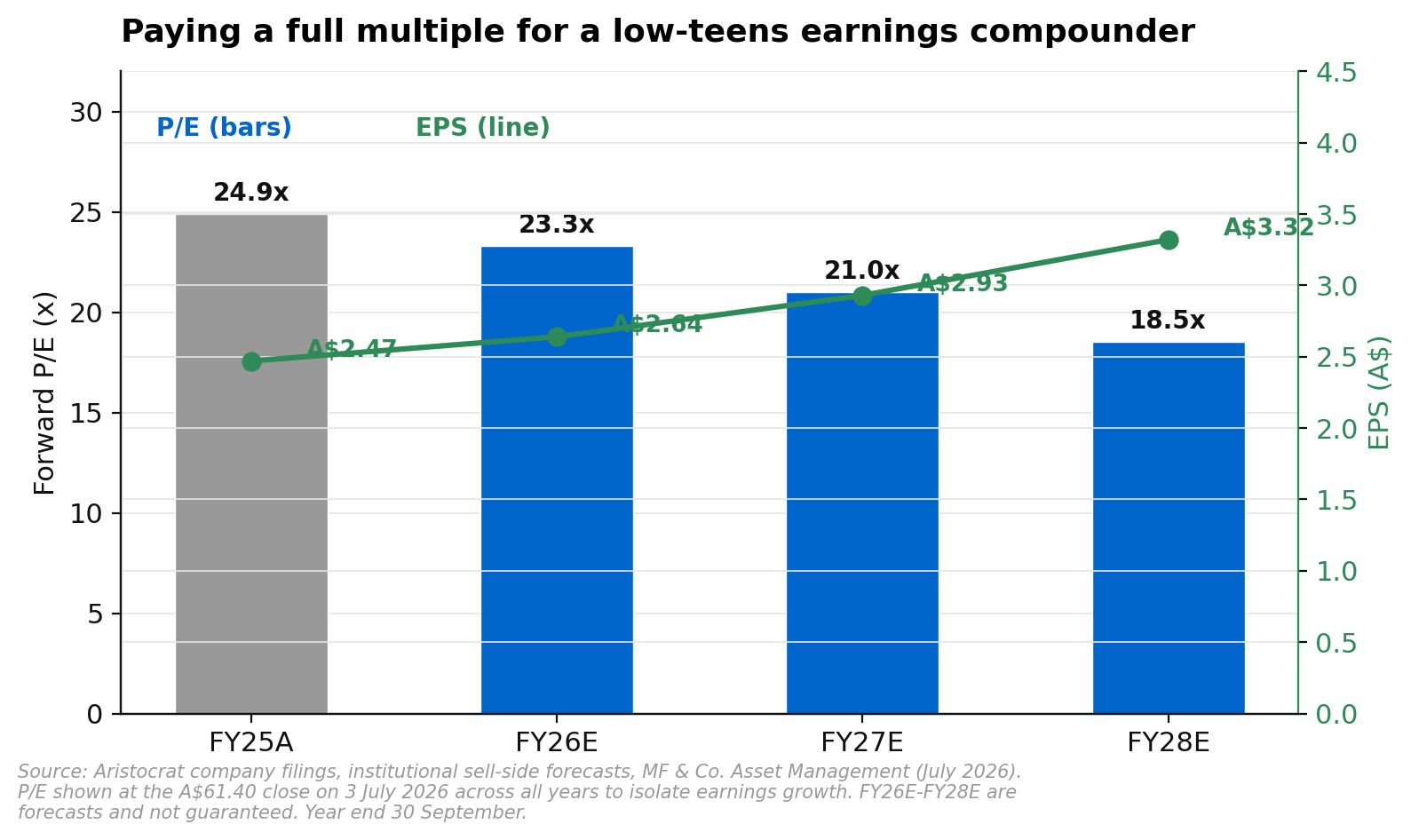

The valuation is where investors need to be clear-eyed. After a run of more than thirty per cent since our May note, Aristocrat is no longer cheap. At A$61.40 the stock trades on about 23 times FY26 forecast earnings, easing to roughly 21 times FY27 and about 19 times FY28 as earnings per share grow from A$2.64 to A$3.32 over that window. In other words, the multiple eases from here mainly because earnings rise into a roughly steady share price, not because the price has to fall. The 12-month price target of A$70.00 is built on a sum-of-the-parts approach that values Gaming, Product Madness and Interactive separately on forward earnings, rolled forward to FY27, and it was lifted by about eight per cent after the Investor Day to reflect that roll-forward and the firmer Interactive outlook.

The forecast dividend yield is modest, at around 1.6 per cent on FY26 and rising toward 2 per cent by FY28, so this is plainly a growth holding rather than an income one. The way to think about the risk and reward is that you are paying a full but not extreme multiple for a business growing earnings at a low-teens percentage rate, with a genuinely large and under-penetrated Interactive opportunity layered on top and a proven track record of taking share in its core market. The near-term price upside of around 14 per cent is real but unspectacular. The case for owning it is the compounding over the next three to five years, not a quick move to the target.

Risks to the Buy Call

There are four risks worth weighing. The first is competition. Aristocrat’s edge rests on producing better-performing games than anyone else, and any slippage in that hit rate, in either land-based or online content, would erode both share and pricing. The second is regulation. Gaming is one of the most heavily regulated industries there is, and while new states legalising online gaming is a source of upside, changes in rules, tax rates or licensing in existing markets can move the numbers quickly. The third is macro and currency. Aristocrat earns the majority of its revenue in the United States, so a weaker US consumer would soften gaming operations, and a stronger Australian dollar reduces the value of those earnings on translation. The fourth is execution on the Interactive ramp itself. The billion-dollar target depends on scaling content, lottery and platform revenue together, and take rates on online content can compress as operators consolidate, so the path is unlikely to be perfectly smooth.

Our View

We are staying positive on Aristocrat, but with our eyes open about what has changed. The May thesis was partly a cheap-multiple story, and that part has largely played out with the shares up more than thirty per cent. What remains is a high-quality compounder with a mature, share-gaining cash engine funding a fast-growing Interactive arm that is only now reaching an inflection point. The Investor Day did not change the numbers much, but it did firm up the credibility of the billion-dollar Interactive target and the levers behind the margin expansion. At around 14 per cent upside to the A$70.00 target plus a small and growing dividend, the near-term return is ordinary, and anyone buying today is doing so for the multi-year growth rather than a quick re-rating. On that longer view we think the risk and reward still favours owners.

If you would like to discuss Aristocrat Leisure or how ASX-listed growth companies might fit within your portfolio, request a callback or call us on 1300 889 603. The above is general advice and does not consider your individual circumstances. Past performance is not a reliable indicator of future returns.