Walmart closed down 7.3% after its 1Q26 earnings beat and management reiterated full-year guidance, creating what we think is an attractive entry point for the world’s largest retailer. Institutional sell-side research has Walmart rated Buy with a 12-month price target of approximately $154, implying around 30% upside from the recent close of $118.57. The company delivered a solid US comp of +4.1%, driven by traffic gains of +3.0% and average ticket of +1.1%, while eCommerce net sales grew 26% in the US. Transaction growth in the US was the strongest it has been in six quarters, and market share gains in general merchandise hit the highest level in five years. We think the combination of share gains, an accelerating advertising business, and growing membership income positions Walmart to keep compounding through what remains a challenging consumer environment.

Research published 27 May 2026. Price target and upside based on prices at time of publication.

About Walmart

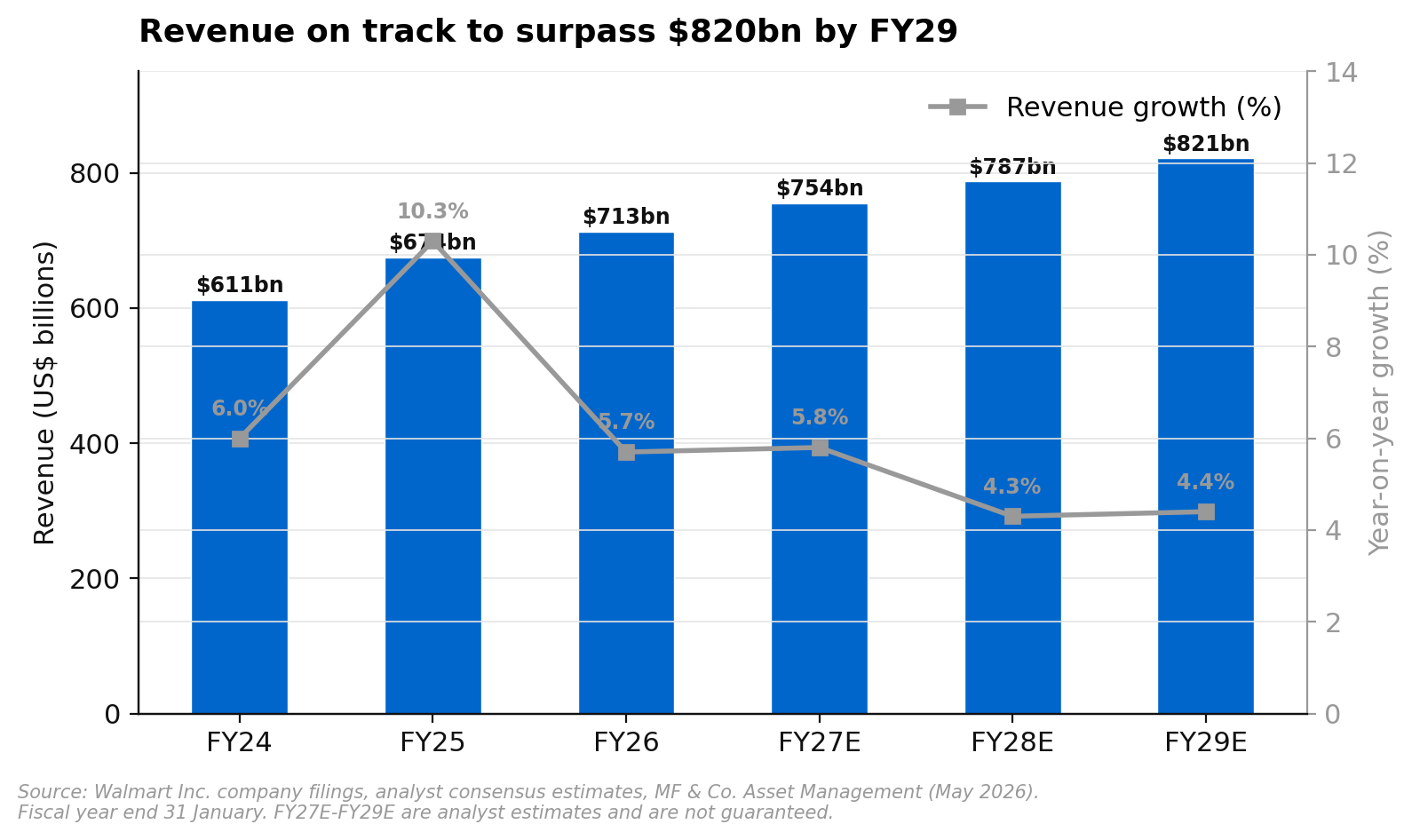

Walmart Inc. is the world’s largest retailer by revenue, operating approximately 10,600 stores and clubs across 19 countries under the Walmart, Sam’s Club, and Flipkart banners. The company generated over $713 billion in revenue in fiscal year 2026 (ending January 2026), making it the largest company in the world by sales. Walmart’s US segment accounts for roughly two-thirds of total revenue, with the International segment and Sam’s Club contributing the remainder. The company has a market capitalisation of approximately $945 billion and is listed on the New York Stock Exchange. Walmart’s most recent quarterly filings and investor presentations are available on the company’s investor relations page.

Traffic-Led Comps Show the Value Proposition Is Working

Walmart US same-store sales grew 4.1% in 1Q26, comfortably ahead of consensus expectations of 3.6%. The quality of the comp matters just as much as the headline number. Traffic was up 3.0% and average ticket rose 1.1%, which tells you that customers are visiting more frequently rather than simply paying more per trip. That traffic-led mix is exactly what you want to see from a retailer in an environment where consumers are watching every dollar. Transaction growth was the strongest it has been in six quarters, and management noted that the time horizon for new customers to become members is shortening, which is a leading indicator that the flywheel is gaining momentum.

By category, grocery was up mid-single digits, health and wellness grew low single digits, and general merchandise was up mid-single digits for the first time in 18 quarters. That last point is worth dwelling on. General merchandise has been a headwind for Walmart (and most mass retailers) since late 2022, so the fact that it flipped positive in 1Q26 is a meaningful inflection. Management called out strength in fashion and hardlines, with some help from tax refunds, but was careful to note that the growth extends beyond any single catalyst. Fashion is seeing outsized growth, and categories like home decor and beauty are benefiting from a derivative lift.

The Advertising and Membership Flywheel Is the Margin Story

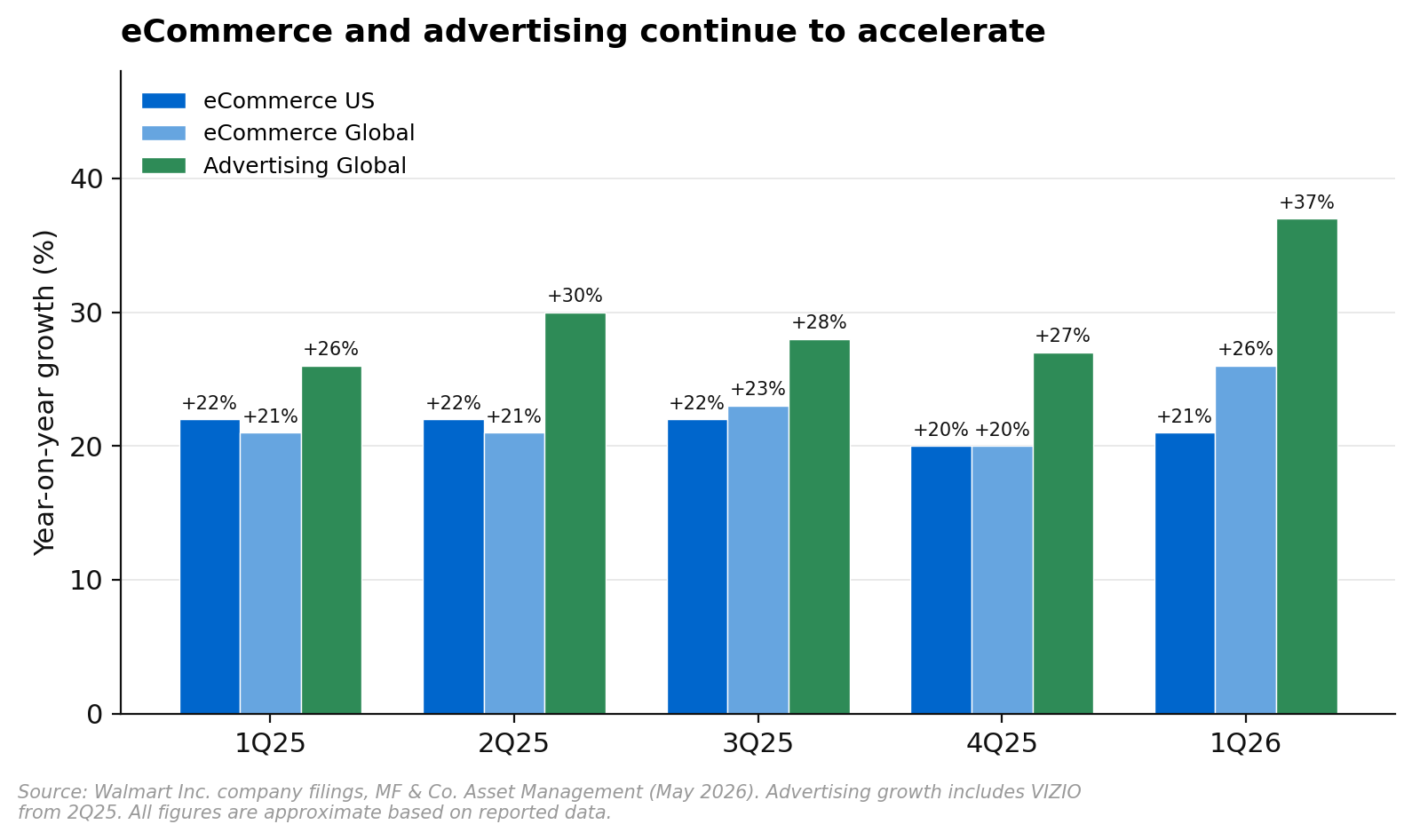

Walmart’s pivot from a pure-play retailer to a platform business is well underway, and the numbers are starting to show it. Global advertising revenue grew 37% year-on-year in 1Q26 (including VIZIO), while Walmart US advertising grew 44% excluding VIZIO. Management reported strong engagement from marketplace sellers, who grew their advertising spend by over 50% and saw a corresponding lift in sales. The VIZIO acquisition, which closed in early FY26, gives Walmart a connected TV advertising platform that slots neatly into its closed-loop retail media offering.

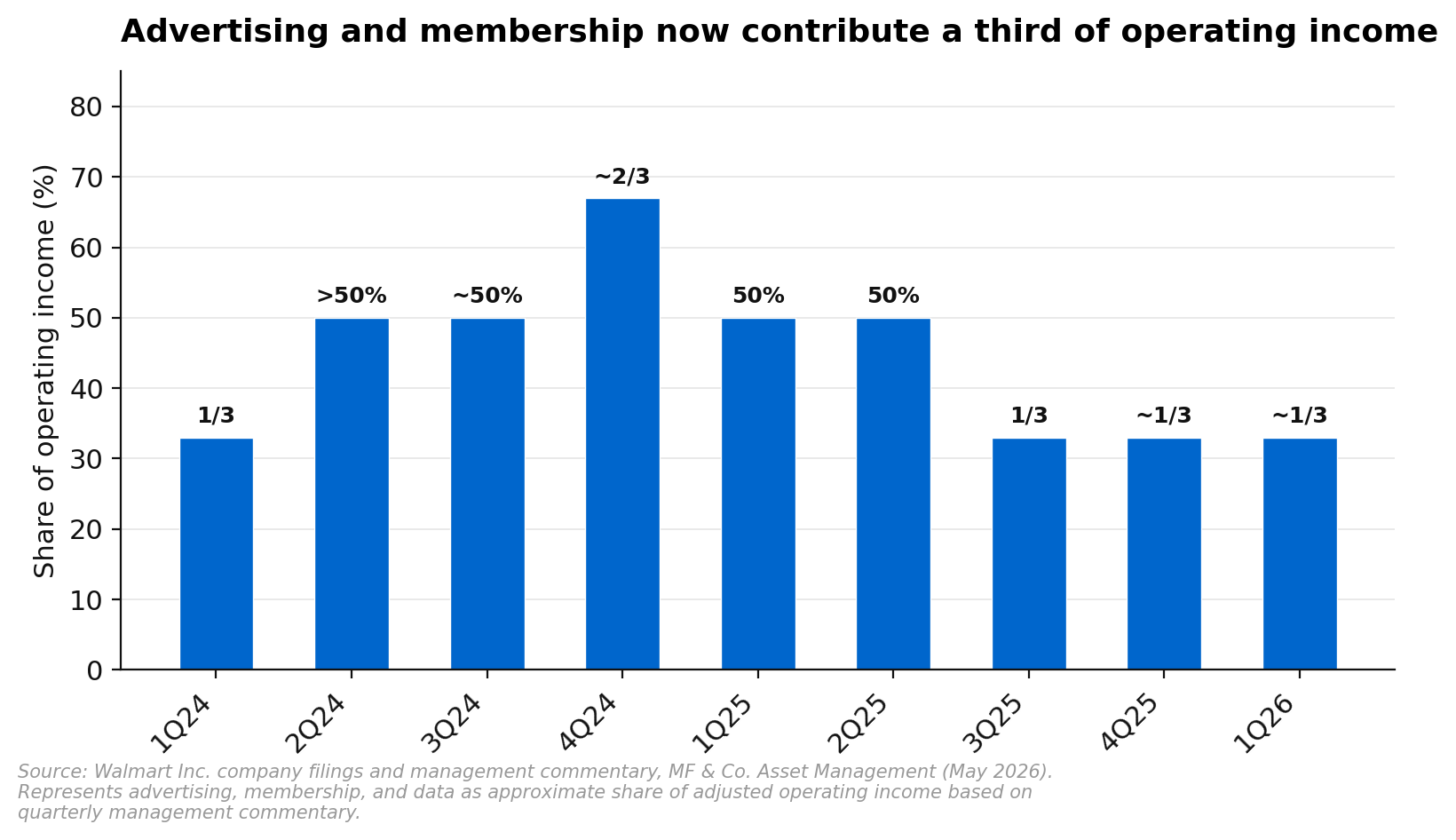

The bigger picture is that advertising, membership, and data services now contribute approximately one-third of Walmart’s consolidated operating income. That ratio has held steady over recent quarters, but the composition is improving. These are structurally higher-margin revenue streams than traditional retail, and they are growing at multiples of the core business. Walmart Connect (the advertising arm) reached US and global eCommerce profitability for the first time in 1Q25, and advertising and membership are now a quarter of profits and rising.

Membership income also grew double digits, with Walmart+ continuing to add subscribers. The membership base gives Walmart a recurring revenue stream and a stickier customer relationship, while the data it generates feeds directly into the advertising targeting engine. We expect management to contribute about two-thirds of total profit growth from newer businesses (advertising, data, fintech, and membership) over the next few years, which should support ongoing margin expansion even if the retail environment remains competitive.

eCommerce Is Scaling and the Unit Economics Are Improving

Walmart’s eCommerce business has reached a scale where it is no longer a drag on group profitability. US eCommerce net sales grew 21% in 1Q26, while global eCommerce grew 26%. The company now has one of the largest eCommerce operations in the world, and the combination of store-fulfilled delivery, marketplace expansion, and Walmart+ membership is creating a virtuous loop. Marketplace sellers are drawn to the platform by traffic, they spend on advertising (growing +50%), which funds the ecosystem and drives further traffic.

The gross margin picture is also improving. 1Q26 gross margin came in at 24.3%, up 7 basis points year-on-year. Walmart US gross margin increased 29 basis points, and management noted that this was the first time in 18 quarters that merchandise mix contributed favourably to gross margin. That shift matters because it suggests the margin expansion is structural rather than a one-off. The company absorbed approximately $175 million (or 250 basis points) of operating income growth from elevated fuel costs in the quarter, choosing to invest in lower prices to support long-term share gains rather than protect short-term margins. That willingness to invest through cost headwinds is classic Walmart, and it is one reason the company continues to gain share across income cohorts.

Consumer Resilience and Tariff Positioning

Management’s commentary on the consumer was nuanced and worth unpacking. The consumer remains resilient overall, but pressure has increased for lower-income households amid higher gas prices. This was visible in a shift on the discretionary side towards consumables. Higher-income consumers, however, continued to drive the top line, and the company is gaining share across income cohorts including lower, middle, and the bottom end of higher income. About 75% of customers say they feel financially concerned, but this is more sentiment than actual spending behaviour, and Walmart’s value proposition tends to strengthen in exactly this type of environment.

On tariffs, management was measured. The company currently has roughly 7,200 rollbacks in place (up more than 20% year-on-year), and it reiterated FY26 guidance of +3.5% to 4.5% net sales growth on a constant-currency basis, now trending towards the upper end of that range. Tariff-eligible refunds represent less than 0.5% of US annual sales, and the company signalled it would prioritise price investment over margin protection. Walmart’s scale, sourcing diversification, and private-label capabilities give it more room to absorb tariff costs than most peers, and the share gains that come with aggressive pricing are likely to compound over time.

Valuation

At $118.57, Walmart trades at approximately 40x FY27 estimated earnings per share of $2.97. That multiple compresses to 35x on FY28 estimates of $3.37 and 31x on FY29 estimates of $3.84. The institutional sell-side price target of $154 implies approximately 30% upside and is anchored by a revenue base approaching $755 billion, accelerating higher-margin alternative revenue streams, and a track record of share gains across economic cycles. The valuation framework uses relative P/E multiples with downside, base and upside scenarios at 175%, 180% and 185% of the S&P 500 forward multiple, reflecting Walmart’s defensive franchise and structural growth from newer businesses.

Risks to the Buy Call

A slowdown in US economic activity or deterioration in consumer confidence would weigh on discretionary spend, particularly in general merchandise where the recent inflection could reverse. A more intense pricing environment, whether driven by tariffs, competitive responses from Amazon and Costco, or input cost inflation, could pressure gross margins and offset the gains from higher-margin alternative revenue. Wage and transportation cost inflation remain headwinds, and the company’s willingness to invest in price rather than protect margins creates earnings volatility in quarters where costs spike unexpectedly. Foreign exchange volatility, particularly in the Mexican peso and Chinese yuan, could impact international earnings translation.

Our View

Institutional sell-side has the stock at a Buy with $154 of fair value. At 40 times forward earnings with a clear path to 31 times by FY29, a consumer franchise that is gaining share across income cohorts, and an advertising and membership flywheel that is structurally shifting the margin profile, the risk-reward looks favourable after the post-earnings pullback. The 7.3% drawdown following a quarter where the company beat on comps, reiterated guidance, and reported the strongest transaction growth in six quarters looks like a sentiment-driven overreaction to consumer caution commentary rather than a fundamental deterioration.

The alternative revenue trajectory is the swing factor. If advertising and membership continue to grow at multiples of the core and expand their share of operating income beyond one-third, the margin expansion story accelerates and the premium multiple is justified. If the macro environment deteriorates and discretionary spend softens, the general merchandise recovery could stall and the margin trajectory flattens.

If you would like to discuss Walmart or how US consumer equities might fit within your portfolio, request a callback or call us on 1300 889 603. The above is general advice and does not consider your individual circumstances. Past performance is not a reliable indicator of future returns.