Tradeweb Markets runs one of the largest electronic marketplaces for trading bonds, interest rates and other fixed income products, yet its shares have spent 2026 going backwards. The stock now sits roughly a third below its high of the past year and trades near the bottom of its multi-year valuation range, even as revenue keeps compounding at a mid-teens pace. The market has been worried about three things: whether that growth can last, whether the tokenisation of financial assets will eventually disrupt the model, and whether the whole listed trading-venue group deserves a lower multiple. We think the sell-off has run well ahead of the fundamentals. Institutional sell-side research has Tradeweb Markets rated a Buy with a 12-month price target of about US$146, implying roughly 47 per cent upside from the recent close of US$98.83.

Research published 15 July 2026. Price target and upside based on prices at time of publication.

Table of Contents

About Tradeweb Markets

Tradeweb Markets is a global operator of electronic marketplaces for fixed income, rates, credit, equities and money markets, connecting institutional, wholesale and retail investors with dealers and each other. Founded in 1996, it has grown into one of the core pieces of plumbing for electronic bond and swaps trading, with more than US$2 billion of annual revenue and a market value of around US$22 billion. Revenue splits across four main areas: Rates, its largest business, then Credit, Money Markets and Equities, supported by a growing market-data franchise. The company is listed on the Nasdaq and is majority-owned by London Stock Exchange Group. More detail is available through the company’s investor relations page and its filings with the SEC.

Rates trading is the engine, and the runway is long

Rates is Tradeweb’s biggest business, making up more than half of revenue, and it is also the fastest growing. The standout inside it is interest-rate swaps, where Tradeweb has grown volumes far quicker than the wider market and lifted its share into the mid-20 per cent range. That has been helped by a structural tailwind: the pool of government debt outstanding is large and still expanding, and as more of it trades, the volume of rates activity rises with it. Turnover, the rate at which that debt changes hands, has also been improving, which amplifies the effect.

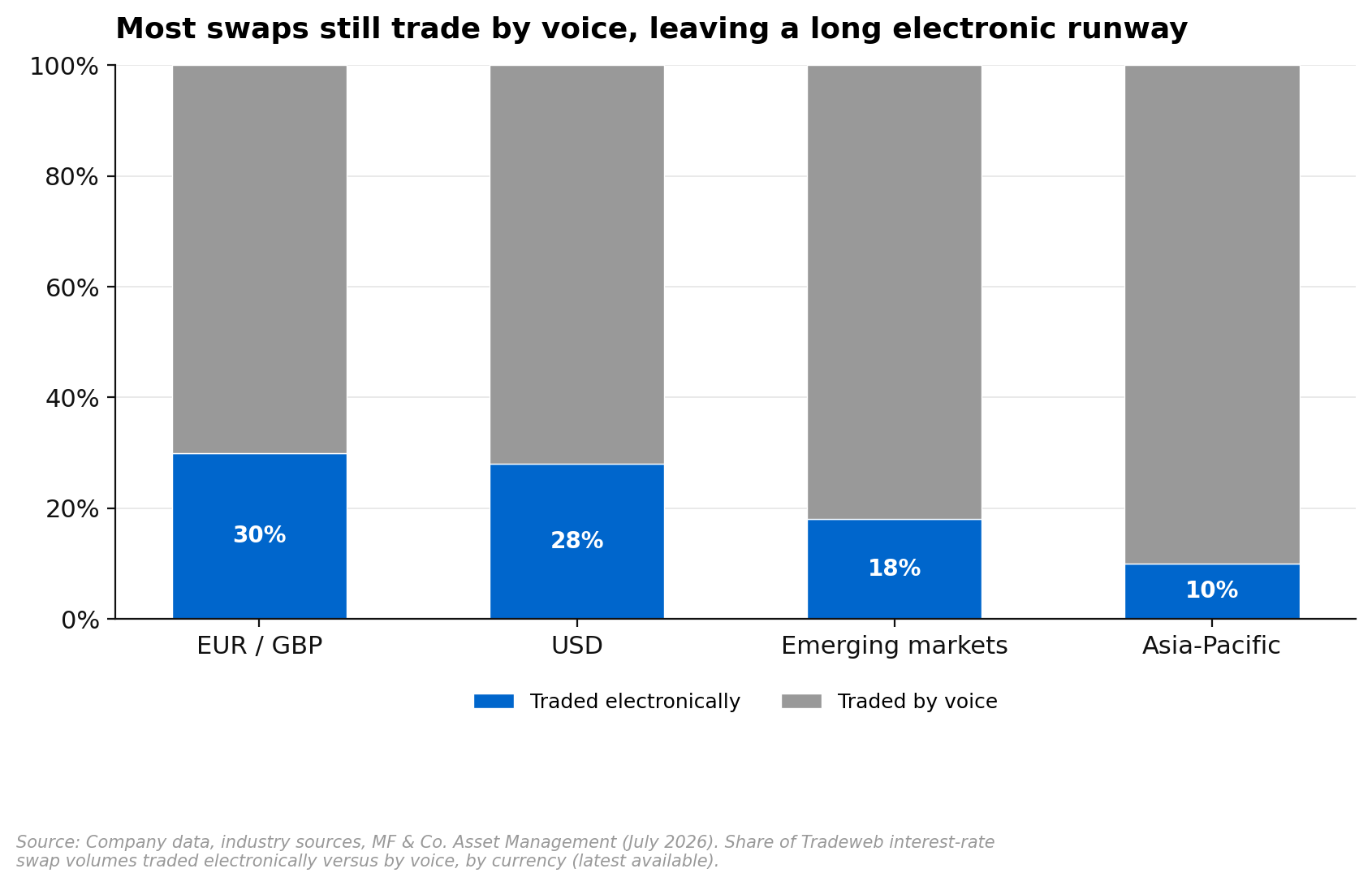

The bigger point is how early electronic trading still is in this market. Across the major currencies, most interest-rate swaps still trade the old way, by voice, with electronic penetration only in the twenties or thirties per cent and lower still in emerging markets. That gap is the opportunity. As trading shifts onto screens, and as Tradeweb keeps winning share, the Rates business has years of growth ahead of it even after a strong run.

Emerging-market swaps are a smaller but telling example of where this is heading. Non-US swaps now make up the majority of Tradeweb’s swaps volumes, and the emerging-market slice, though still modest in size, has been one of the faster-growing parts of the book. It also carries richer economics than the average trade, so as the mix shifts in that direction it lifts the average fee Tradeweb earns per trade, not just the volume. That is the kind of quiet mix-shift that tends to get overlooked when the market is fixated on headline growth rates.

Cash trading tells a similar story. Tradeweb clears a large and rising share of US Treasury and agency-mortgage trading, both of which are supported by heavy government issuance and the same improving-turnover trend. In mortgages in particular the firm holds a dominant share of the electronic market, with a big pool of activity still done by voice and ripe to move across.

The credit worry looks overdone

The main bear case is Credit, Tradeweb’s second-largest business at around a fifth of revenue. Growth here slowed to mid-single digits as competition intensified and the trading mix shifted toward lower-fee protocols, and the market has extrapolated that slowdown into the future. We think that is too pessimistic.

The underlying credit market is expanding. Record levels of corporate bond issuance have lifted the pool of tradable debt, and turnover is running at high levels without the market stress that normally drives those spikes, a sign that the shift to electronic and basket-based trading is structural rather than a passing cyclical bounce. Within that market, Tradeweb’s share in portfolio trading, the protocol that has reshaped how large credit baskets change hands, has stabilised after some earlier erosion, and the firm still has room to grow in request-for-quote trading and in emerging-market credit, where it remains under-represented.

Two shifts help the recovery along. Corporate bond issuance is on track for another very strong year, which keeps feeding the pool of debt available to trade, and the large banks that count among Tradeweb’s most important customers have been rebuilding their corporate bond inventories after years of running them down. Both put more flow through the system that Tradeweb can capture as electronic trading keeps taking share from the phone. The thesis does not need a return to the old high-teens growth rate to work. A recovery back toward double-digit growth is enough to change the picture, and the backdrop is lining up to support it.

The market has sold the growth

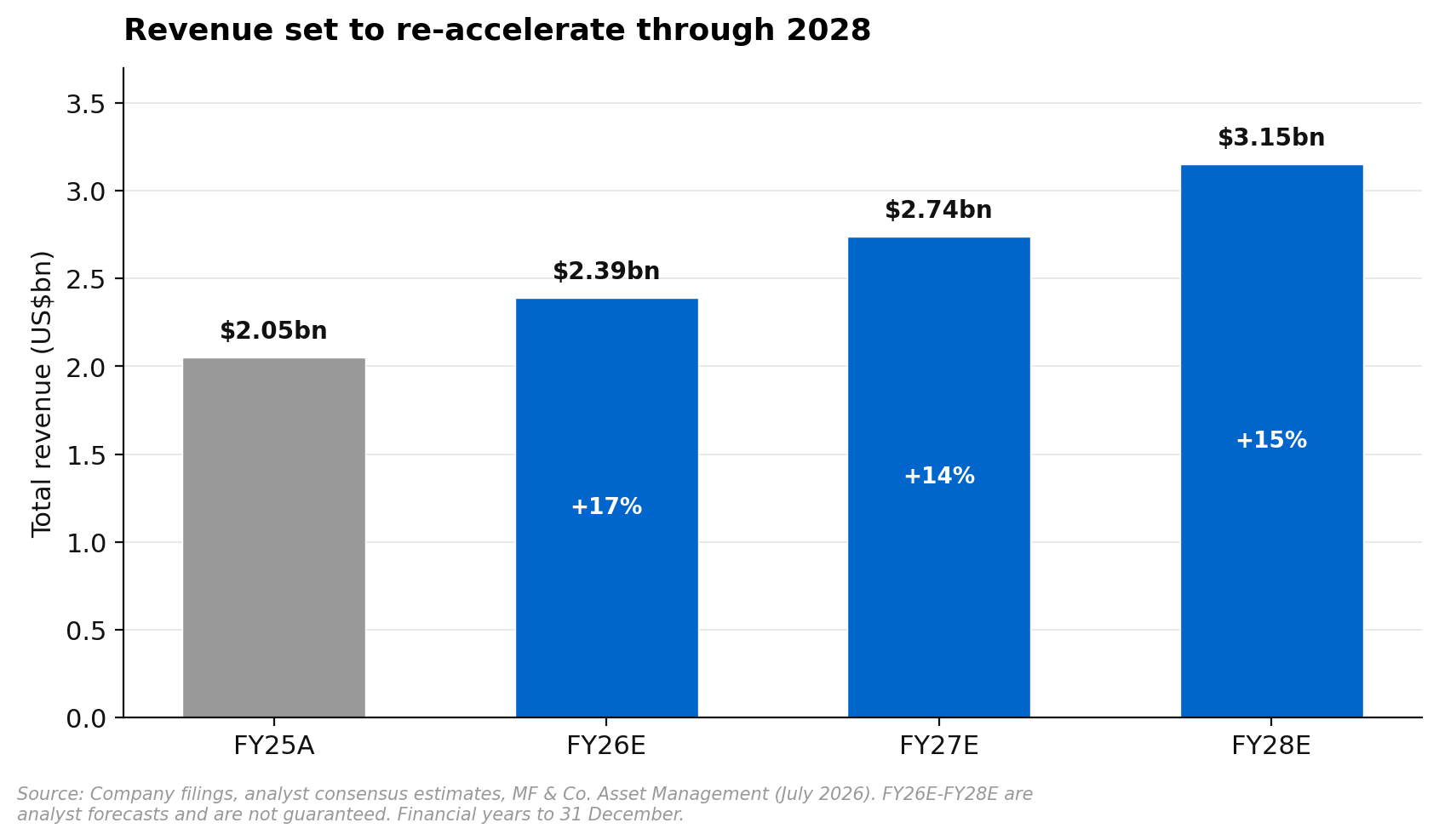

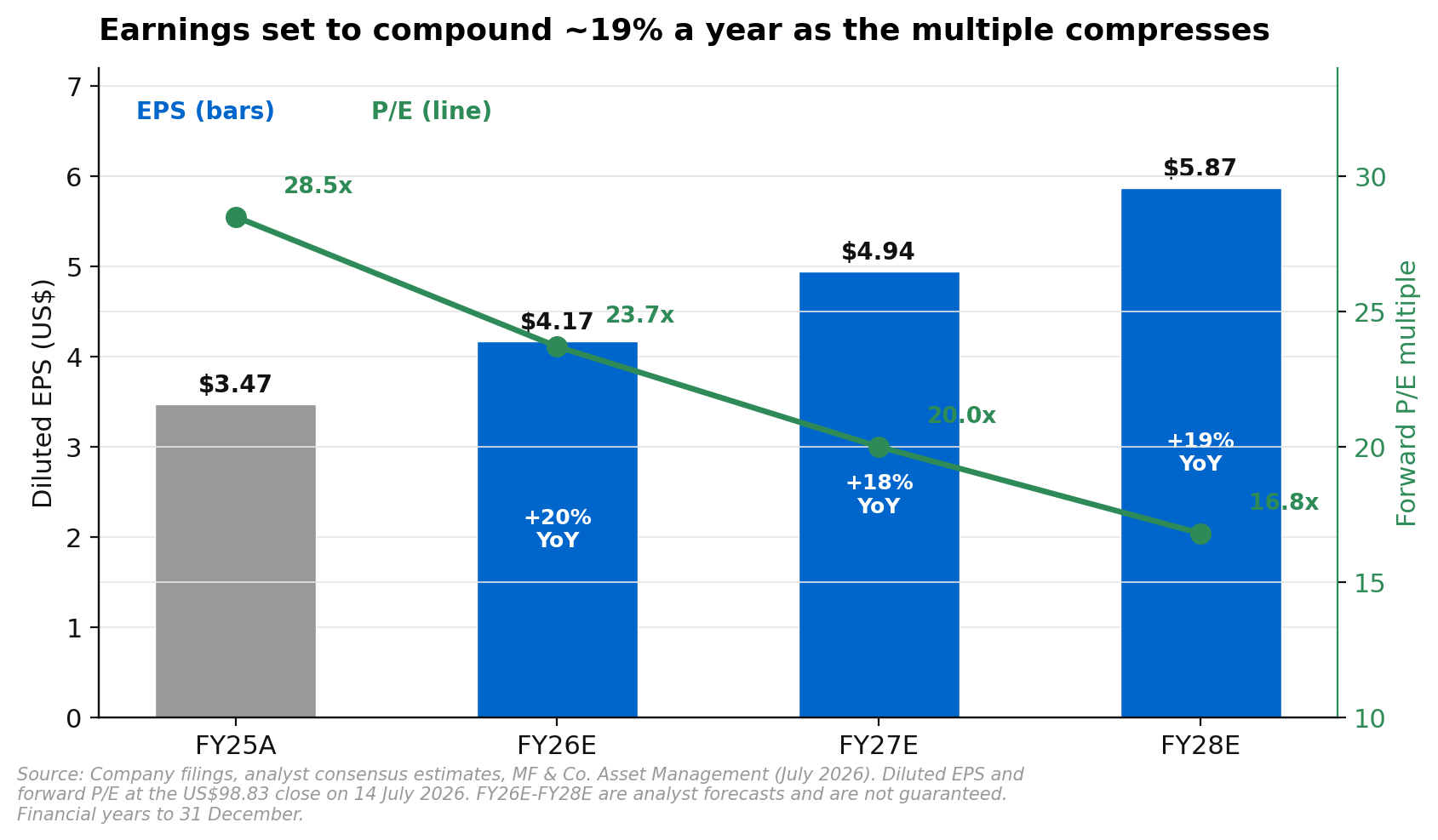

Step back and the valuation looks disconnected from the business underneath it. Revenue grew about 19 per cent in 2025 and is forecast to keep compounding in the mid-teens, re-accelerating toward 17 per cent in 2026 as both Rates and Credit contribute. Earnings are expected to grow faster still, at close to 19 per cent a year through 2028.

Yet the shares have de-rated to around 22 times forward earnings, well below the roughly 37 times they averaged over the past five years, as sentiment across listed trading venues soured and investors began fretting about longer-dated risks such as the tokenisation of real-world assets. The read-across from a weaker peer group is a poor fit for Tradeweb, whose organic growth is running at roughly twice the pace of the average listed venue. On that last worry, tokenisation, Tradeweb looks more like a beneficiary than a victim. Its global, multi-asset network is exactly the sort of infrastructure that stands to gain if settlement shortens and trading becomes more standardised across markets. The company also carries close to US$2 billion of net cash and no debt, which gives it the flexibility to fund acquisitions or return capital to shareholders while it waits for sentiment to catch up with the numbers.

Valuation

Institutional sell-side research rates Tradeweb a Buy with a 12-month price target of about US$146, roughly 47 per cent above the recent close of US$98.83. The case rests on three things: organic revenue growth in the mid-teens, faster than most listed trading-venue peers; earnings compounding at close to 19 per cent a year through 2028; and a multiple that has fallen to the low end of the company’s own multi-year range despite that growth staying intact.

As earnings scale over the next few years, the forward multiple compresses further on an unchanged price, which is another way of saying the market is paying a below-average price for an above-average grower. The dividend is modest, with a yield under one per cent, so this is a capital-growth case rather than an income one. The risk and reward look asymmetric: a business still growing at a mid-teens clip, a de-rated multiple and a net-cash balance sheet on one side, against fears that so far have not shown up in the results on the other.

Risks to the Buy Call

Most of Tradeweb’s revenue comes from variable transaction fees tied to trading volumes, so a drop in interest-rate volatility or a slowdown in secondary-market activity would feed straight through to revenue. A faster shift toward lower-fee trading protocols could keep diluting average fees and squeeze margins. Competition in both Rates and Credit is intense, and renewed share or pricing pressure would slow the growth the thesis depends on. The company also reinvests heavily in technology and staff, so if costs grow faster than revenue, margins would come under pressure. And the longer-term tokenisation debate, while we read it as an opportunity, remains a genuine uncertainty for every incumbent trading venue.

Our View

The pattern here is a familiar one. A high-quality compounder gets caught in a sentiment-driven de-rating, and for a while the price stops tracking the fundamentals. Tradeweb is still taking share in its biggest markets, still has most of its addressable trading volume sitting offline, and still turns that into mid-teens revenue growth and faster earnings growth, yet it trades near the bottom of its own valuation range. For a patient investor, that gap between a durable growth business and a discounted multiple is where the opportunity sits. It is not a cheap stock in absolute terms, and the fears are real rather than imaginary, but on balance the growth looks more durable than the multiple implies.

If you would like to discuss Tradeweb Markets or how US financial and technology names might fit within your portfolio, request a callback or call us on 1300 889 603. The above is general advice and does not consider your individual circumstances. Past performance is not a reliable indicator of future returns.