Two weeks on from the Federal Budget, institutional sell-side economics research has published a fuller quantitative read on what the housing tax overhaul actually does to a property investor’s return profile. Our earlier piece covered the headline framing when the policy landed. This piece focuses on the numbers. The take-out is uncomfortable for the policy’s proponents and underwhelming for its critics. The annual cash flow hit on a representative new investor is material, the impact on total returns is modest, and the structural reasons that Australians lever into residential property over every other asset class do not change. Read together with our earlier piece on the Budget framing, the conclusion is that the political signal is louder than the economic one.

Research published 29 May 2026. All figures from Commonwealth Treasury, ATO, OECD and institutional sell-side economics research.

What Actually Changed

Two measures sit at the centre of the overhaul. From 1 July 2027 the 50% capital gains tax discount will be replaced for individuals, trusts and partnerships with inflation indexation plus a 30% minimum rate on the real (inflation-adjusted) gain. From the same date, negative gearing against salary and wages will be removed for established residential dwellings purchased after Budget night (12 May 2026). Losses on those properties will be quarantined and carried forward, available to offset future rental income on any residential property the taxpayer owns or capital gains realised when the property is sold. The CGT change applies across all asset classes, including listed equities. Newly constructed dwellings retain favourable treatment, with investors in new builds able to choose between the old 50% discount and the new indexation method, and able to continue negatively gearing against income. Existing owners are grandfathered for negative gearing but their post-2027 capital gains fall under the new indexation method.

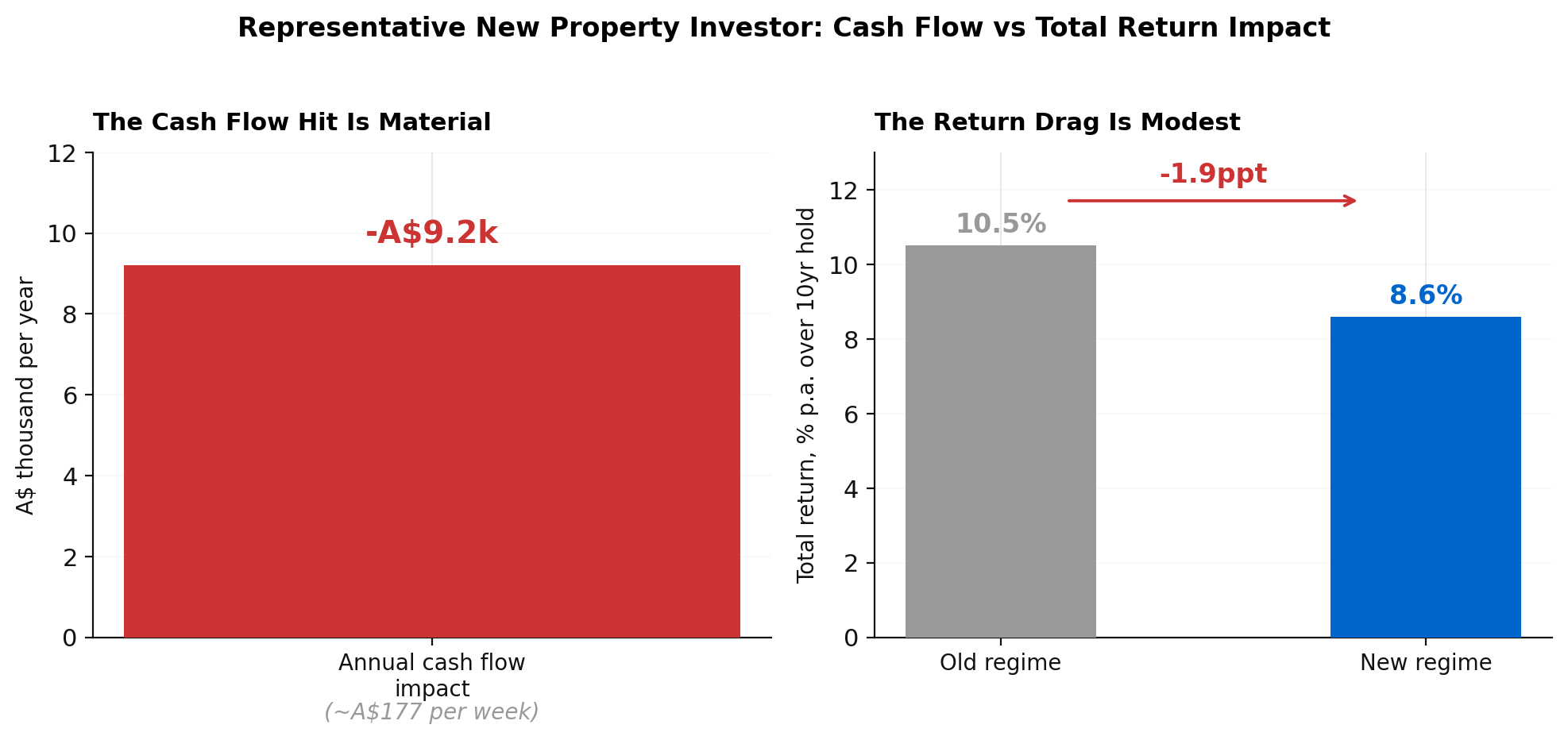

The Cash Flow Hit Is Material. The Total Return Drag Is Modest.

The representative new investor in the institutional model holds a median-priced $940k property with an 80% loan-to-valuation ratio over a 10-year horizon, with inflation tracking the central bank’s 2.5% target. Under those settings the cash flow impact in year one is approximately negative $9,200, equivalent to around $177 a week. That figure scales with leverage and inversely with rental yield. Investors with higher LVRs or lower yields will see larger numbers. The reason the cash flow hit feels meaningful while the total return picture does not is that losses are no longer extinguished against labour income. They are quarantined and reapplied later against rental income or against the eventual capital gain, but at a higher effective discount rate. The time value of money makes the deferred offset less valuable than an immediate one, but the value is not zero.

The total return decline lands at just under two percentage points per annum across the 10-year hold, lifting the effective tax rate on the eventual capital gain from approximately 23.5% to 31.7%. For an asset class where individual property returns can vary by several percentage points year to year, a 1.9ppt structural drag is real but is also well within the noise of an investor’s individual experience. The headline of the change reads as a wealth tax on landlords. The mechanics read as a tilt, not a confiscation.

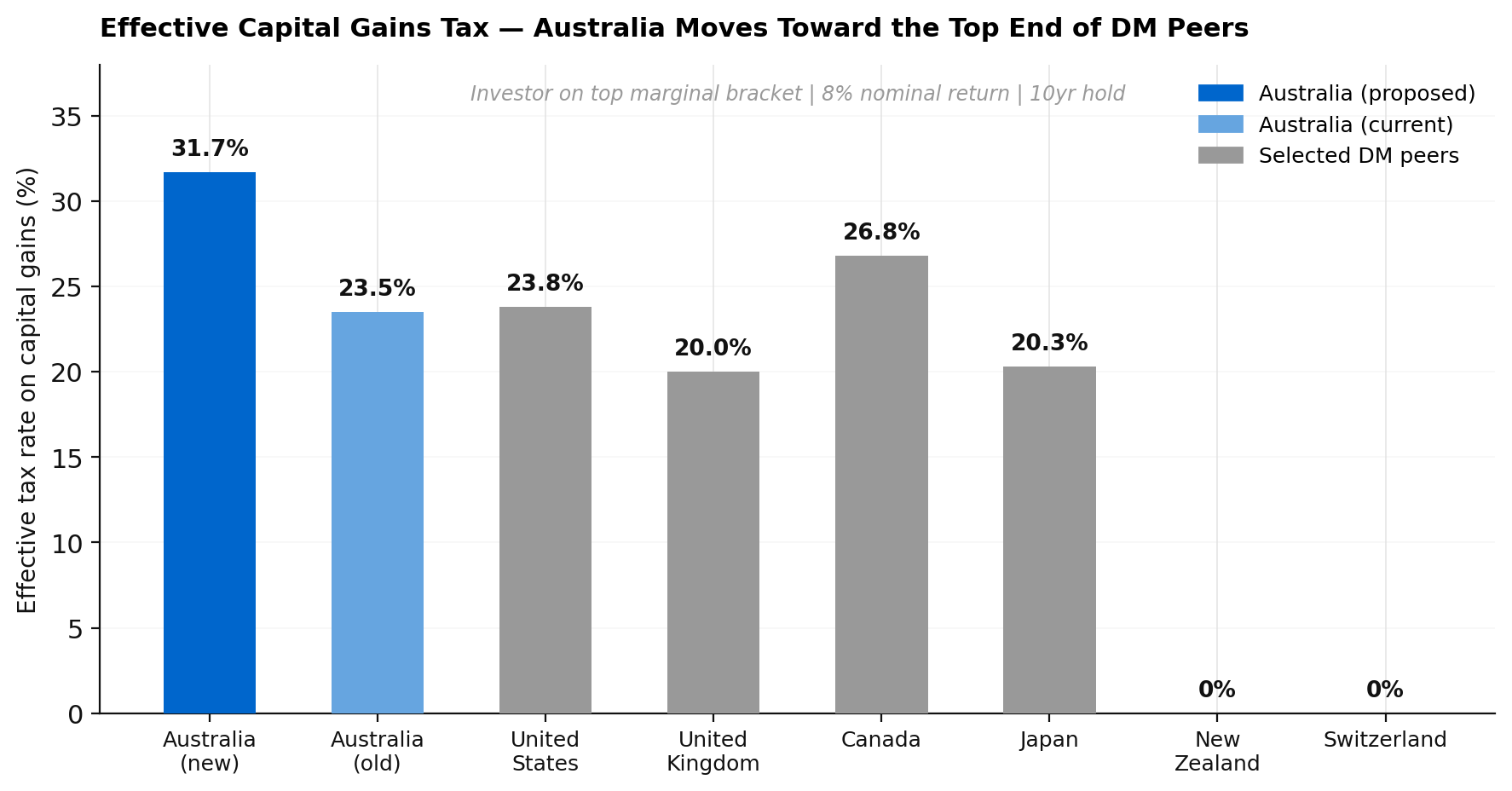

Australia Moves Toward the Top of the Developed-Market Capital Gains Ladder

The 30% minimum rate on real gains is the structural feature that drives the headline tax-rate increase. For assets with low real returns, indexation is more generous than the old 50% discount. For assets with real returns running well above inflation, which describes both residential property and listed equities over the last quarter-century, indexation is less generous. The result is that an investor on the top marginal bracket holding an 8% nominal return asset for ten years moves from an effective CGT rate near the middle of the developed-market pack to one of the highest in the OECD.

The corollary the policy debate has under-weighted is that the change applies to listed shares too. An Australian investor holding ASX-listed equities for the long term will pay the same higher effective rate on the same real gain. The CGT framework is asset-class neutral. The differential treatment is between new builds and everything else, not between property and equities. That matters for advice. Long-term equity holders who modelled their after-tax retirement income off the 50% discount need to redo the maths on every meaningful position acquired after 1 July 2027.

Why Reallocation Away From Property Will Be Modest

The first-order intuition is that if property’s after-tax return falls, capital should leave property for assets that have not been similarly disadvantaged. The institutional view, which we agree with, is that the reallocation will be limited for structural reasons that the tax change does not touch. The Australian financial system allows households to lever residential property at 70 to 80% LVR through long-tenor mortgages with no margin call risk and favourable regulatory capital treatment. The same household applying to fund equity exposure faces margin lending at a fraction of that leverage, mark-to-market calls and a tighter regulatory capital regime. The total stock of margin lending in Australia is around 2% of investor housing credit, with roughly 80,000 active margin lending accounts against 2.3 million property investors. The leverage advantage of property is not a tax artefact and a CGT change does not remove it.

The reallocation that does occur is more likely to be within the housing complex than out of it. Newly constructed dwellings retain both the old CGT discount option and full negative gearing, which makes them the highest after-tax return option inside the residential category. Investors who would previously have purchased an established dwelling now have an explicit tax incentive to direct capital toward new supply instead. New builds carry their own risks, including construction defects, regulatory cost overruns and elevated input price exposure following the post-COVID supply shock, so the carve-out will not be free money. But the direction of marginal investor demand is clear.

The House Price Call: Negative 5% Over the Next Year, With a Cautionary NZ Analogue

The structural impact on residential property prices is forecast at approximately negative 3% over time, broadly consistent with academic and Treasury studies of comparable historical proposals. The cyclical call is sharper. House prices are now expected to fall around 5% year-on-year over the next twelve months to a cyclical trough in the first quarter of 2027, against a prior forecast of negative 3% year-on-year. The composition of buyers will shift, with the share of owner-occupiers in new lending likely to rise as some investors withdraw and as renters at the margin become first-home buyers.

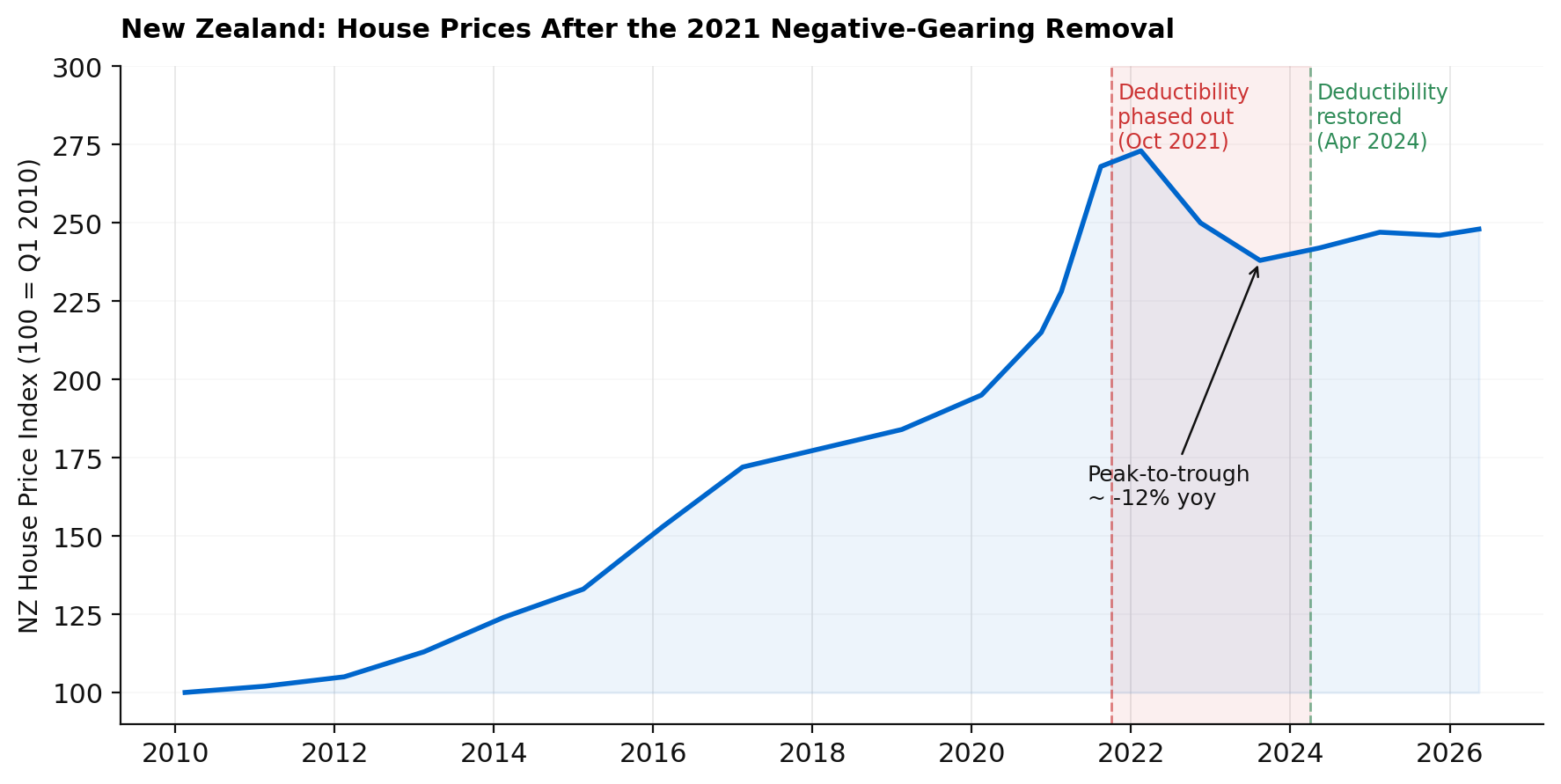

The relevant historical comparator is New Zealand, which removed interest deductibility on established investment properties in October 2021 under the Ardern government. House prices peaked the same quarter and fell sharply over the next two years, reaching a year-on-year trough of approximately negative 12% by the third quarter of 2023. The investor share of new residential mortgage lending fell from around 26% to around 17%. The Luxon government restored deductibility in April 2024 and prices have stabilised since.

The NZ episode is a cautionary tale rather than a forecast. New Zealand removed deductibility into a year that began with 30% year-on-year house price growth and was followed by 525 basis points of RBNZ tightening. The Reserve Bank itself attributed most of the decline to interest rates, not the tax change. Australia enters its policy change into a softer cyclical setup, with auction clearance rates already weak and home-buyer sentiment among the over-50 cohort, who represent roughly half of property investors, weakening in April surveys. The risk is asymmetric. The central case is a 5% decline over the next year. The downside case is that investor sentiment deteriorates by more than the underlying cash flow numbers warrant, which has happened before in housing markets responding to perceived loss of favoured status.

Will It Pass?

Labor holds 94 seats in the House of Representatives and will pass the package through the lower chamber on its own numbers. In the Senate, Labor’s 30 seats are nine short of a majority. The Coalition has indicated it will oppose the package and repeal it if returned to government. The Greens have indicated they will support the legislation, with the public position that they would prefer fewer carve-outs and no grandfathering. Labor plus the Greens clears the Senate threshold without needing crossbench support, which also means the carve-outs as currently legislated are likely to survive. Our base case is that the package passes broadly as announced over the next several months, with grandfathering of existing investors and the new-build carve-out intact.

What This Means For Investors

The investor practical takeaway sits in three buckets. First, the window to acquire established residential investment property under the old negative gearing regime closed on Budget night. Investors planning to add to their property book over the next decade need to either accept the new regime on established dwellings or pivot toward new builds, which carry construction and execution risk but retain favourable tax treatment. Second, the CGT change is not a property-only issue. Long-term equity holders need to revisit their after-tax return assumptions on positions acquired after 1 July 2027, particularly in growth assets that have historically returned well above inflation. Third, the timing question is real. If the central forecast of a 5% house price decline over the next year is correct, and the downside risk is for a larger move, the question for investors with concentrated property exposure is whether to reduce that concentration before the cyclical move or after it.

Interested in how we can help? Get in touch with our team or call us on 1300 889 603.