Institutional sell-side rates MongoDB a Buy with a 12-month price target of US$360.00. The stock was trading at US$334.68 on 19 May 2026, implying roughly 8 per cent upside. The thesis centres on three pillars: Atlas cloud consumption that keeps growing faster than the overall business, a product cadence that is positioning MongoDB as the default data layer for AI-native applications, and an earnings trajectory that compresses the forward P/E from 55 times to 36 times by FY29 without requiring any re-rating.

Research published 20 May 2026. Price target and upside based on prices at time of publication.

About MongoDB

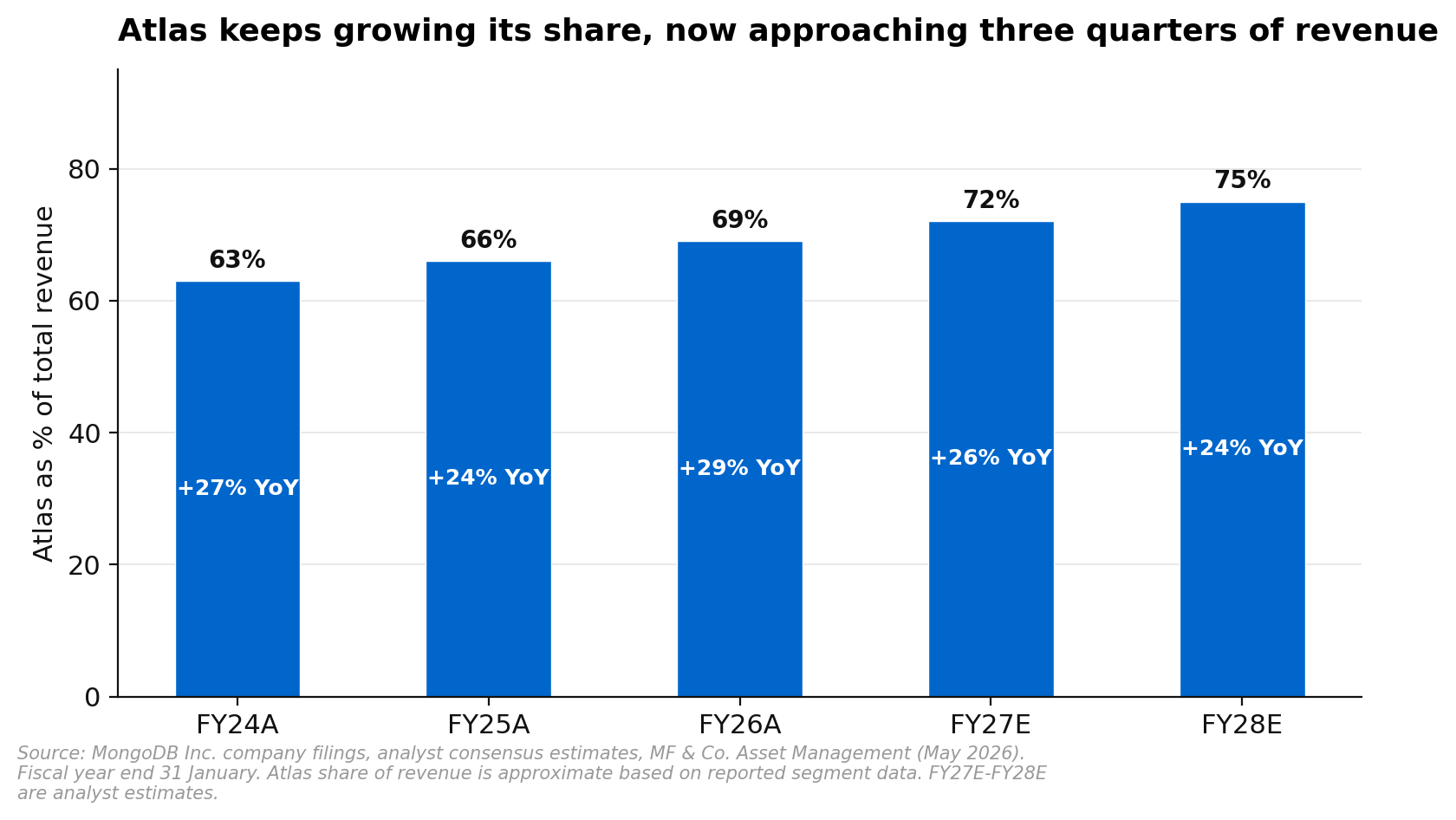

MongoDB is an independent, general-purpose data platform built on its flexible document model. The company operates two main products: MongoDB Atlas, its fully managed cloud database service that now accounts for roughly 72 per cent of total revenue, and Enterprise Advanced, an on-premises offering for customers who need to run MongoDB in their own data centres. The platform has expanded well beyond its NoSQL roots to include search, vector capabilities, event streaming and AI-native tooling. MongoDB listed on NASDAQ in 2017 and has a January fiscal year end. More on the company at mongodb.com.

Atlas Is the Growth Engine

Atlas now represents roughly 72 per cent of total revenue and continues to grow materially faster than the overall business, with reported growth of 29 per cent in the fourth quarter of fiscal 2026. The consumption-based pricing model means revenue scales with usage, and the underlying usage trends are accelerating. Developer downloads of MongoDB’s core driver package grew 55 per cent year on year in the first quarter of calendar 2027, a re-acceleration after several quarters of steady deceleration, which coincides with the mainstream adoption of AI coding tools that scaffold new projects using MongoDB as a default data layer.

Two narrower AI-specific metrics sharpen the picture. Downloads of the LangGraph checkpoint package, installed specifically to use MongoDB as an AI agent’s memory layer, climbed from roughly 50,000 to over 615,000 in twelve months. Downloads of MongoDB’s MCP server package went from 100,000 in December to over 1 million today. These numbers are small in absolute terms but directionally significant: they tell us MongoDB’s developer funnel is broadening and skewing more AI-native with each quarter.

Becoming the Context Engine for AI

MongoDB’s product releases over the past year share a common thread: each one makes the platform a more complete and more default home for AI workloads. Four developments stand out.

First, MongoDB Agent Skills for AI coding tools. The company shipped official agent skills, packaged best practices for schema design, query optimisation and AI retrieval, bundled into Claude Code, Cursor, Gemini CLI and VS Code. The goal is to make it easy for agent-built apps to follow good MongoDB practices from the start.

Second, long-term agent memory for JavaScript. Agents run on two kinds of memory: short-term (the current task thread) and long-term (what the agent learns across sessions). Both need to be stored and queried somewhere, and MongoDB has been building itself into that layer for the leading agent frameworks, now extended to JavaScript and one of the largest developer ecosystems.

Third, automatic embedding via Voyage AI. Embeddings are the mechanism behind RAG and how agents retrieve the right context to act on. The public preview of automatic embedding brings that natively into MongoDB, reinforcing the platform as a strategic asset that grows as agents are used more.

Fourth, MongoDB 8.3, the newest release of the core database, delivers performance gains aimed squarely at AI workloads with faster retrieval and higher throughput for the same spend. Agentic applications query the database harder and less predictably than traditional software, and staying ahead of that demand is what keeps MongoDB the system of record as workloads turn agentic.

Revenue Approaching $4bn With Improving Margins

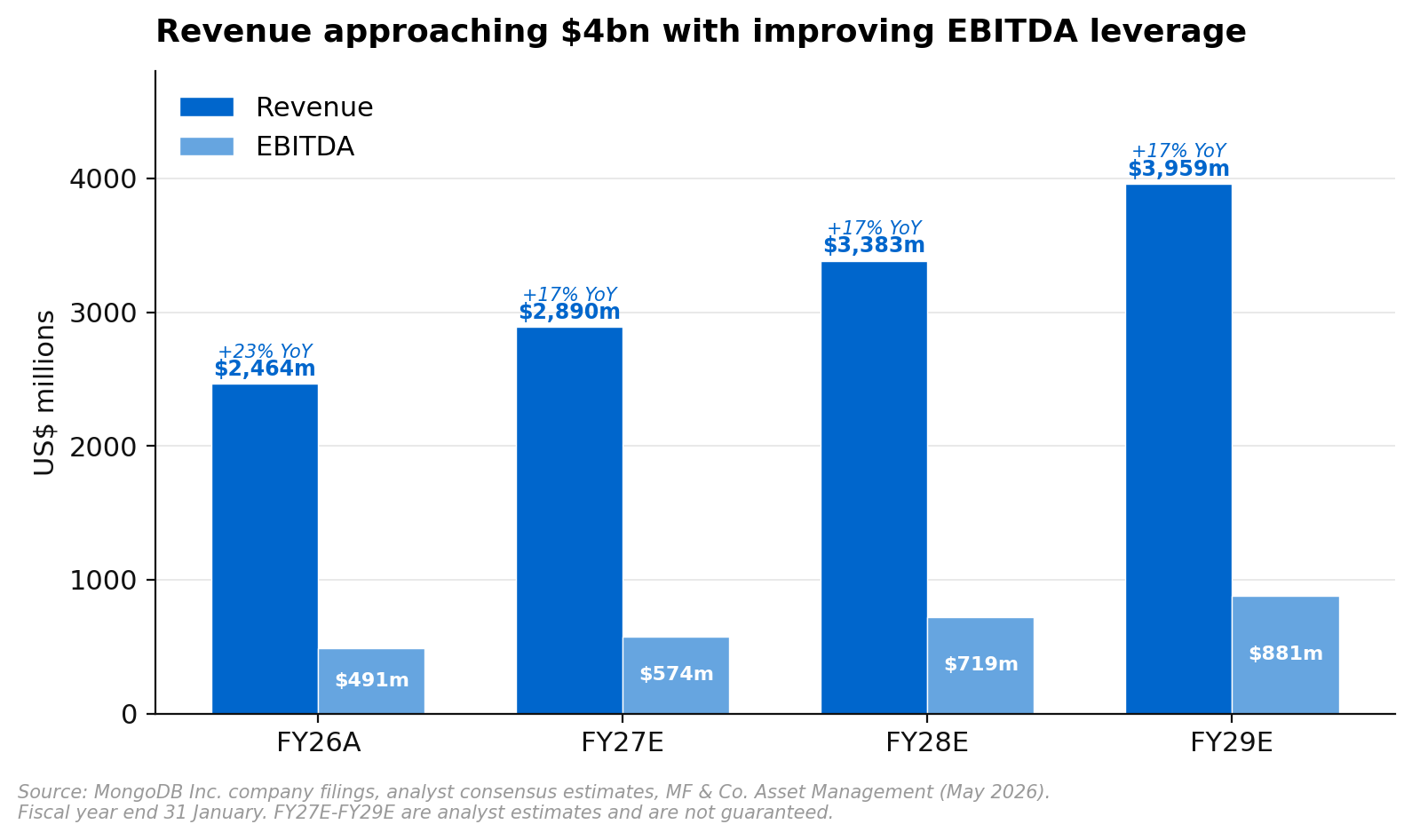

Total revenue grew 23 per cent to US$2.46 billion in fiscal 2026 and is forecast to reach US$2.89 billion in FY27, US$3.38 billion in FY28 and US$3.96 billion by FY29. Revenue growth stabilises in the high teens across the forecast period, which is notable because it comes with meaningful operating leverage: EBITDA is expected to grow from US$491 million in FY26 to US$881 million by FY29, nearly doubling in three years while EBITDA margins expand from 20 per cent to 22 per cent.

Free cash flow generation is also inflecting. The company generated US$493 million in free cash flow in FY26 and is expected to reach US$792 million by FY29, representing a free cash flow yield of roughly 3 per cent at today’s market capitalisation. For a high-growth software business with durable competitive advantages, that is an attractive trajectory.

Where We Land on Valuation

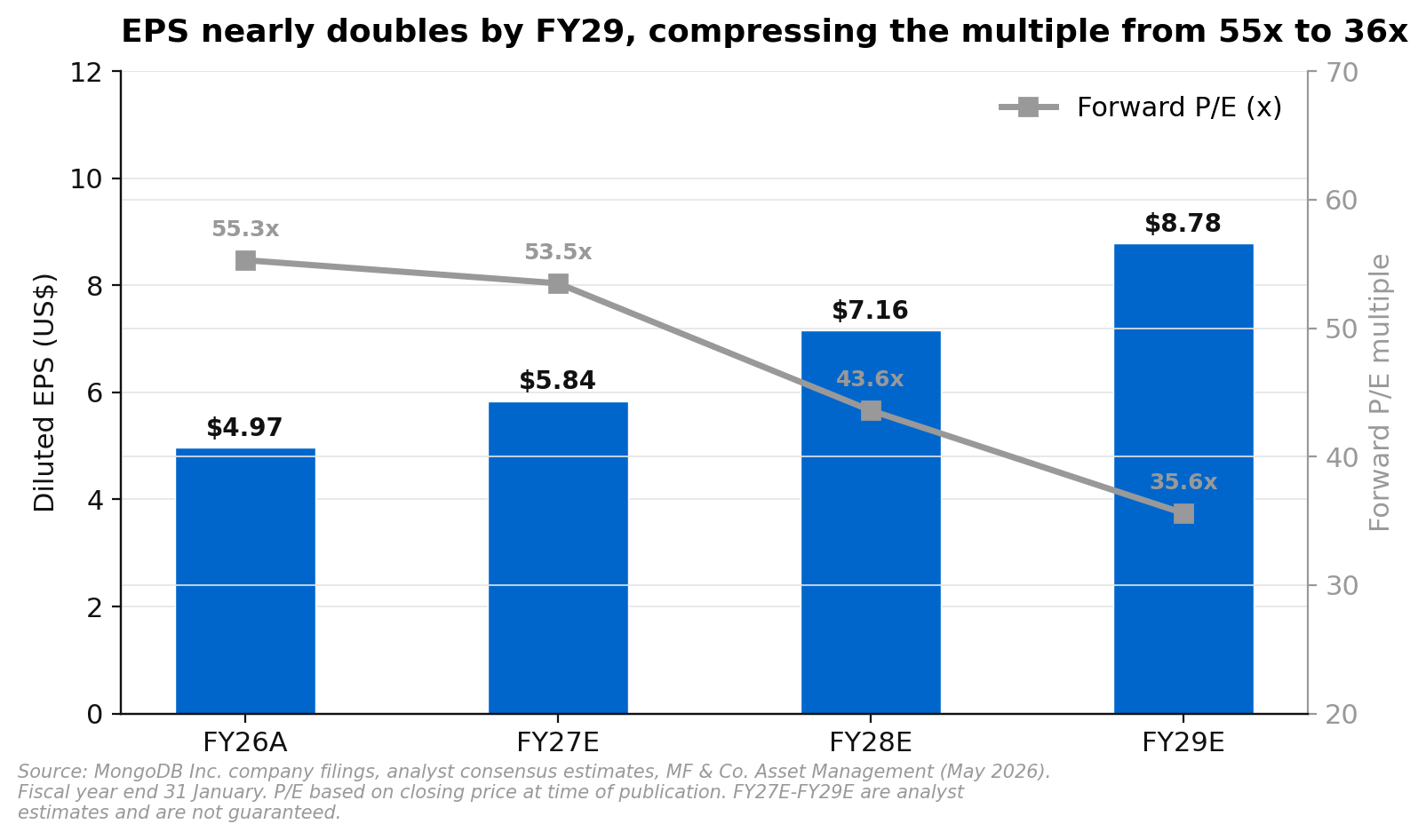

At US$334.68, MongoDB trades at roughly 53.5 times FY27 estimated earnings per share of US$5.84. That multiple compresses to 43.6 times on FY28 estimates of US$7.16 and 35.6 times on FY29 estimates of US$8.78. EPS nearly doubles from US$4.97 in FY26 to US$8.78 by FY29, driven by revenue growth, margin expansion and modest share count reduction.

The valuation framework uses a blended 50/50 approach weighting EV/Sales and EV/FCF multiples. The institutional target of US$360 implies 43 times FY28 EV/FCF and 9 times FY28 EV/Sales, which looks reasonable for a business growing revenue in the high teens with an expanding free cash flow margin and a durable competitive position in the database market.

Risks to the Buy Call

Competitive pressure from relational database incumbents is the primary risk. Hyperscalers including Oracle, AWS, Microsoft and Google Cloud are investing heavily in their own database offerings, and broader standardisation around PostgreSQL could erode MongoDB’s win rates and expansion opportunities over time.

A second risk is that the AI tailwind proves less durable than currently expected. If agentic workloads do not scale as quickly as the developer activity metrics suggest, or if alternative data stores capture more of the AI-native workload, the contribution to Atlas growth would disappoint.

Slowing pace of cloud migration and digital transformation spending, margin degradation due to required reinvestment in the enterprise and AI product lines, and adverse changes in the broader IT spending environment are additional risk factors to consider.

Our View

Institutional sell-side has the stock at a Buy with US$360 of fair value, derived from a blended EV/Sales and EV/FCF framework on FY28 estimates. At 53 times forward earnings with a clear path to 36 times by FY29, a product portfolio that is increasingly embedded in the AI development stack, and a cloud consumption engine that shows no signs of decelerating, the risk-reward looks favourable heading into the F1Q27 earnings print on 28 May.

The Atlas trajectory is the swing factor. A solid F1Q beat paired with a firmer F2Q guide would likely re-rate the stock, particularly given the FY24/FY26 precedent where conservative initial Atlas guidance set up strong full-year revisions. If Atlas consumption disappoints or the non-Atlas business deteriorates, the valuation at 53 times forward earnings offers limited margin of safety on the downside.

If you would like to discuss MongoDB or how it might fit within your portfolio, request a callback or call us on 1300 889 603. The above is general advice and does not consider your individual circumstances. Past performance is not a reliable indicator of future returns.