BlueScope Steel closed at A$32.00 on Friday, which is more than the takeover the board rejected in February was actually worth to a holder once the company’s own capital returns are netted off. The bid has gone quiet and is no longer doing any work in the share price, so the case for owning BlueScope from here has to stand on the business itself. We think it does. Institutional sell-side research has the stock rated Buy with a 12-month price target of A$37.70, implying roughly 18 per cent upside from the recent close of A$32.00. The reason is a cash flow inflection that is already in motion. Capital expenditure peaks this financial year and then falls by more than half, United States steel spreads have widened by about 30 per cent in six months, and a company that has spent three years spending is about to generate close to a billion dollars of free cash next year and more than a billion the year after, with a new capital framework that commits most of it straight back to shareholders.

Research published 13 July 2026. Price target and upside based on prices at time of publication.

About BlueScope Steel

BlueScope Steel Limited is an Australian-headquartered global steel producer with a market capitalisation of approximately A$14 billion, despatching around 8.5 million tonnes of steel a year across five reporting segments. Australian Steel Products runs the Port Kembla steelworks in New South Wales and owns the COLORBOND and TRUECORE painted and coated brands that dominate the domestic building market. North Star BlueScope is an electric arc furnace mini mill in Ohio and is the group’s biggest single earnings swing factor. Buildings and Coated Products North America, Coated Products Asia, and New Zealand and Pacific Steel make up the balance. Roughly 40 to 50 per cent of group production is higher-margin value-add painted and coated steel rather than commodity slab and coil, which is why group margins sit above the United States steel peer group. BlueScope is listed on the Australian Securities Exchange and reports in Australian dollars on a 30 June fiscal year. Results and investor presentations are on the company’s investor relations page.

Capex Has Peaked and the Cash Comes Back

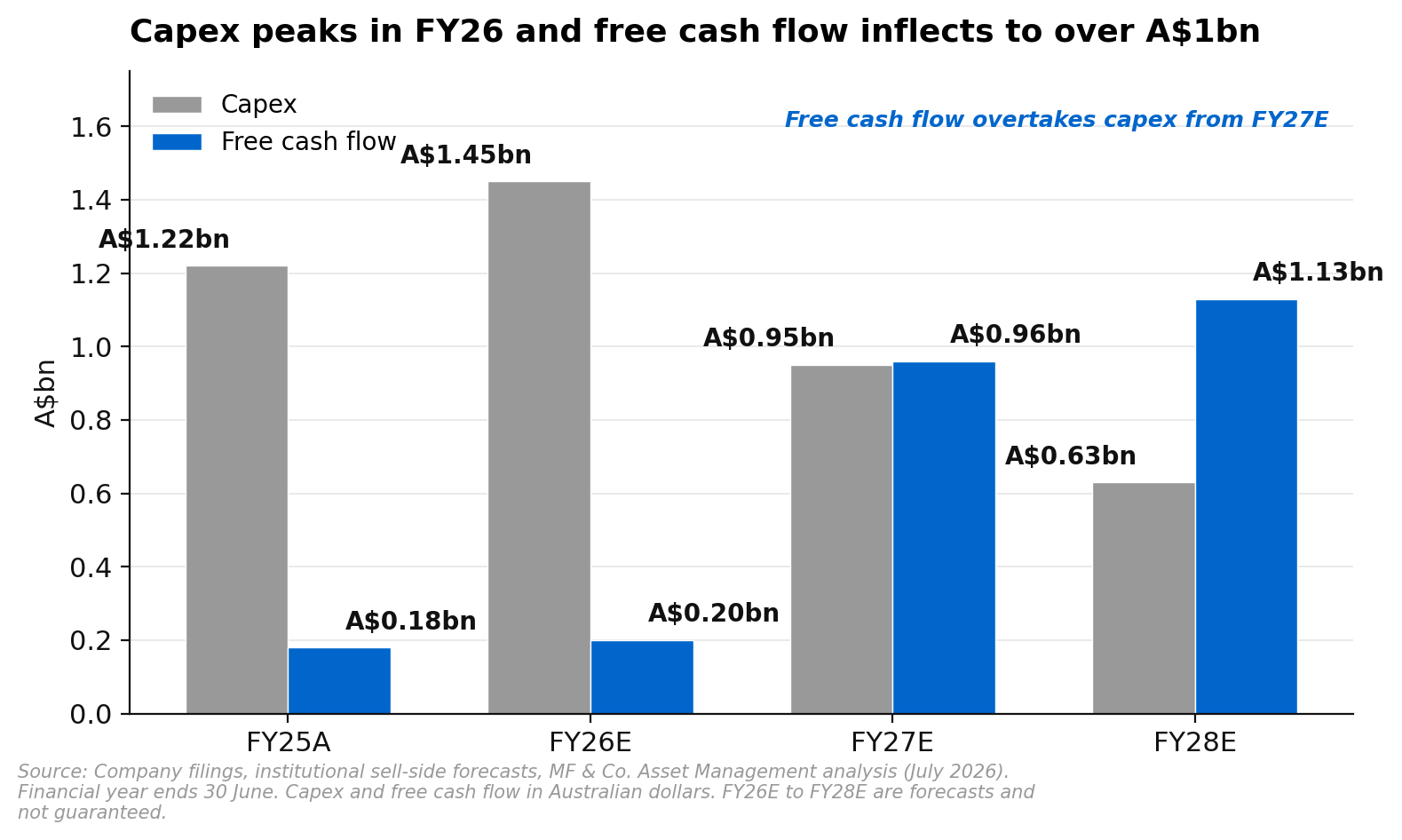

This is the whole thesis in one line. Capital expenditure peaks this financial year at around A$1.45 billion, funding the Port Kembla blast furnace reline, the North Star debottlenecking programme and the United States midstream and painted steel build-out. It then falls to roughly A$0.95 billion in FY27 and around A$0.63 billion in FY28, settling near A$0.7 billion a year after that. The projects do not stop. The spending on them does. What comes out the other side is free cash flow, which goes from about A$0.2 billion this year to roughly A$0.96 billion in FY27 and A$1.13 billion in FY28. At the current price that is a free cash flow yield of just under 7 per cent in FY27 stepping to around 8 per cent in FY28, from a business generating almost nothing today.

The capital framework turns that into shareholder cash rather than a bigger balance sheet. BlueScope has lifted its through-the-cycle net debt target to A$1.5 billion, up from the old A$400 million to A$800 million range, and committed to returning at least 75 per cent of free cash flow. On the FY27 forecast that is more than A$700 million of dividends and buybacks in a single year against a market capitalisation of about A$14 billion, and the company is targeting roughly A$3.00 a share of returns across calendar 2026, including the buyback already running. A further A$150 million cost-out programme, on top of the A$200 million delivered in FY25, and the sell-down of a 1,200 hectare surplus land portfolio sit alongside it.

One honest caveat, because the headline yield flatters. The FY26 dividend of about A$2.30 a share includes a A$1.00 special funded by the India joint venture sale, land sales and a working capital release, so the 7 per cent figure that shows up on a screen is not the run rate. The ordinary dividend has been re-based to 65 cents per half, worth about 4 per cent at the current price, and the FY27 forecast of A$1.70 puts the yield closer to 5 per cent. A 5 per cent forward yield backed by a free cash flow yield approaching 7 per cent is a genuinely good outcome. It is just not the 7 per cent dividend the screen advertises.

The United States Mini Mill Is Doing the Heavy Lifting

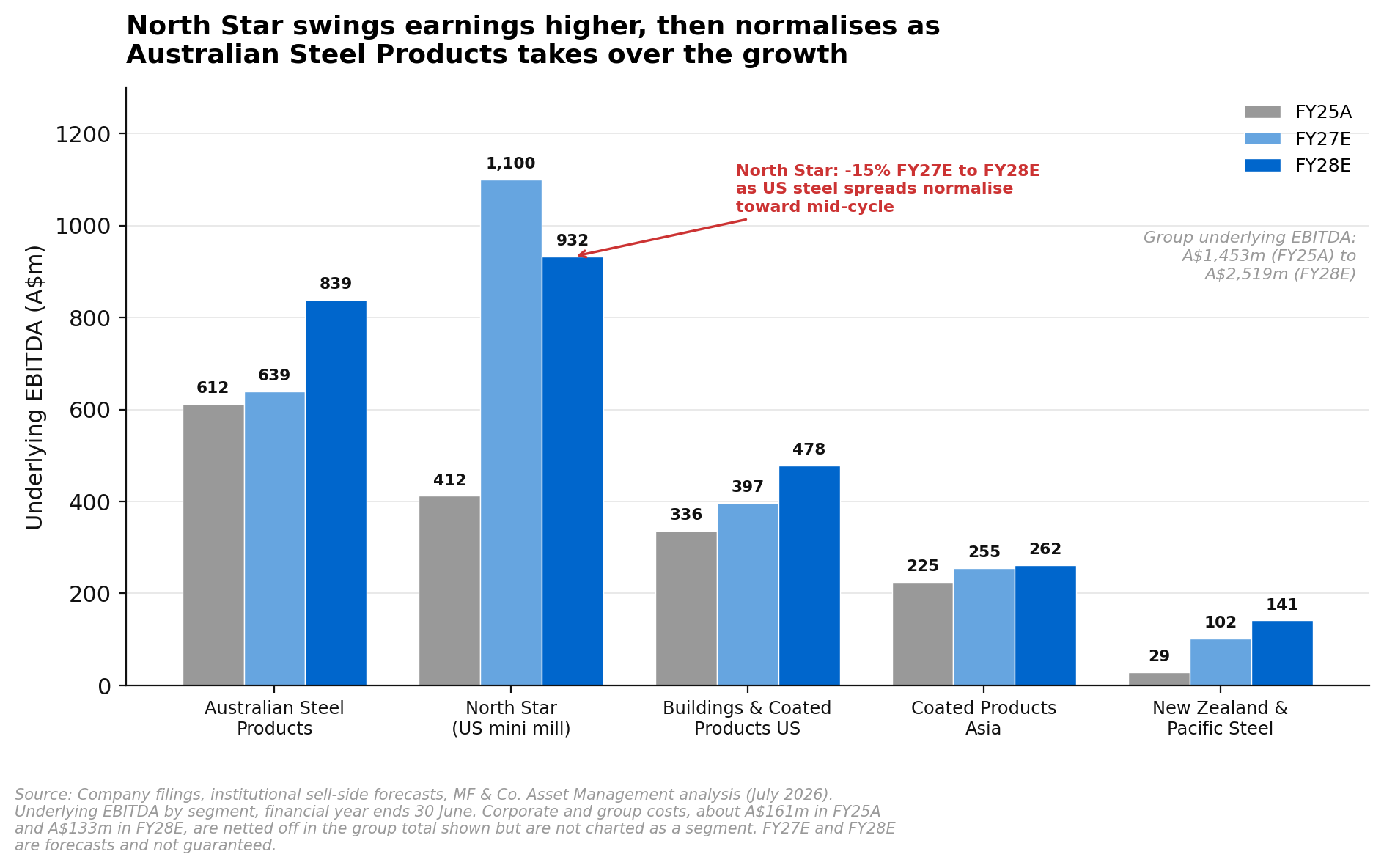

The earnings inflection is not evenly spread. United States hot rolled coil prices have risen about 30 per cent over six months on strong demand and tight supply, and BlueScope’s United States steel spreads have widened by a similar amount. North Star, the Ohio mini mill, is the direct beneficiary, with underlying EBITDA going from A$412 million in FY25 to around A$915 million this year and roughly A$1.1 billion in FY27. That single asset accounts for most of the group’s earnings growth over the next two years. The Australian business gets there later, because it prices off the East Asian benchmark on a three to six month lag, so while East Asian hot rolled coil is up about 15 per cent, Australian spreads have stayed roughly flat. The tailwind is coming. It just has not arrived yet.

Underneath the spread cycle the domestic franchise is holding up better than the macro would suggest. Australian Steel Products domestic volumes grew 1 per cent half on half in the first half of FY26, COLORBOND and TRUECORE sales are running at their highest since 2022 and ahead of the company’s calendar 2026 targets, and second half earnings before interest and tax are guided to A$620 million to A$700 million, up 10 to 25 per cent on the first half. The offsets are real and worth naming, with higher aluminium, zinc, paint and plastic input costs, higher trucking and rail freight, and higher labour and energy costs eroding some margin in every region. The spread tailwind is comfortably bigger than the cost headwind right now, and that gap is what the next two years of earnings rest on.

Look closely at FY28 on that chart, because it is the most important thing on it. North Star steps back down, from about A$1.1 billion of EBITDA to roughly A$930 million, and that is deliberate. The forecasts assume United States steel spreads normalise rather than holding at the recent spot hot rolled coil price, which was around US$1,140 a short ton at the end of June and sits well above the long-run level. Nobody is capitalising the spot spread and calling it a growth business. Australian Steel Products picks up the baton instead, growing from around A$639 million to A$839 million of EBITDA as the lagged pricing benefit flows through. If spreads stay high for longer, these numbers are conservative. If they mean-revert faster, FY28 is where it shows.

The Market Has Already Passed the Rejected Bid

BlueScope has been in play. In December 2025 the company confirmed an unsolicited, non-binding proposal from a consortium of SGH Limited and the United States steelmaker Steel Dynamics at A$30.00 cash a share, and the board unanimously rejected it in January as very significantly undervaluing the company. In February the consortium returned with a revised proposal it called best and final, headlined at A$34.00 a share, structured as A$32.35 in cash less the dividends BlueScope pays in the meantime. The board’s answer was that the price was still not sufficient for directors to recommend, though it stayed open to non-exclusive engagement if the value improved. Two earlier approaches in late 2024, at A$27.50 and A$29.00, had already been turned down.

The number that matters is not the headline. Once the roughly A$3.00 a share of calendar 2026 capital returns are netted off, the board assessed the effective consideration at about A$31.00 a share, and lower again if completion slipped into 2027. That is the figure to hold in mind, because at A$32.00 the shares now trade above what the best and final was actually worth to a holder. The market has not just caught up with the rejected bid. It has gone past it.

So the takeover is not a floor under the price, it is not the reason to buy the stock, and we would not pay a cent for it today. Steel Dynamics’ commentary on its recent earnings call and SGH’s decision to launch its own buyback both point, in our reading, to a consortium that has moved on. What the episode does tell you is still worth something. Two industry buyers who understand steel mills, and who could see the same earnings inflection coming, were prepared to pay a net A$31.00 a share on the board’s own assessment, and were told it was not enough. That is not a reason to own the stock, and it is not a floor. It is a rough read on what informed money thought the assets were worth before the cash flow arrived.

Valuation and What We Are Actually Underwriting

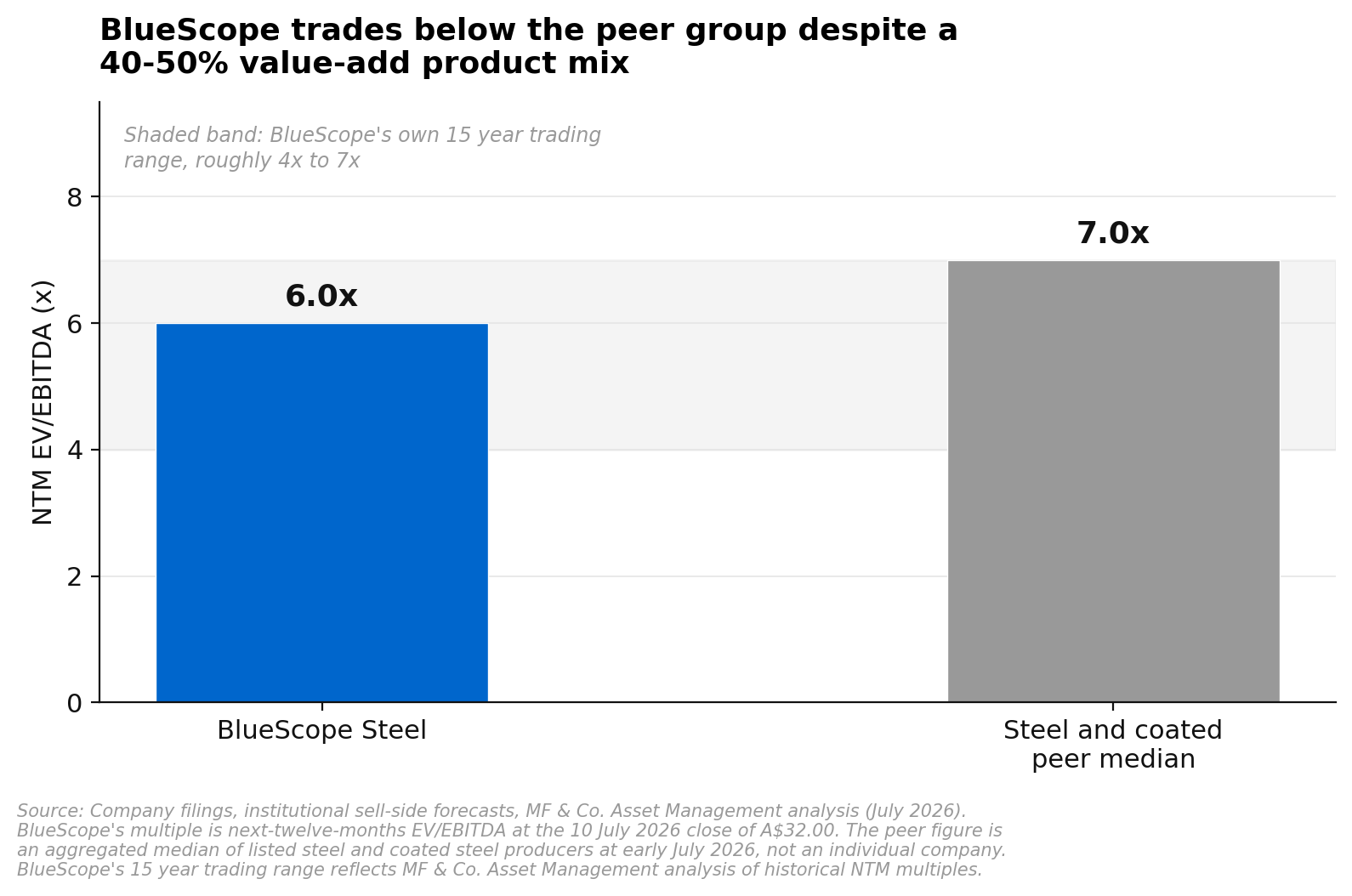

BlueScope trades on about 6 times next-twelve-months EV/EBITDA against a steel and coated peer median nearer 7 times. Its own range over the past 15 years has been roughly 4 to 7 times, so this is not a stock trading at a distressed multiple. It is a stock in the middle of its own range while sitting at a clear discount to the group it competes with. On forecast earnings it is on about 15.6 times FY26, falling to 13.1 times in FY27 as earnings step up. The discount to peers is the part that does not sit right, because between 40 and 50 per cent of production is high-margin value-add painted and coated steel, which is a building products business wearing a steel maker’s multiple, and it is the reason group margins run above the United States steel peers in the first place.

On the target itself we want to be precise about what is being underwritten, because the headline number is not all fundamental. The 12-month price target of A$37.70 implies about 18 per cent upside, and part of it reflects an allowance for corporate interest returning. Strip that out and the underlying sum-of-the-parts valuation sits at around A$36 a share, roughly 12 per cent above the current price, and that is the number we stand behind. Add the forecast dividend yield of around 5 per cent and the total return on the fundamentals alone is in the high teens over 12 months, with any renewed bid activity as free optionality rather than the reason for the trade. It is a solid return rather than a spectacular one. On a cyclical trading below its peer group with the cash flow arriving rather than being promised, we think that is enough.

Risks to the Buy Call

There are four risks worth weighing. The first is the cycle, and it is the one that matters, because this is a commodity business and the FY27 earnings peak is a spread forecast rather than a contracted order book. A global slowdown would hit steel demand and prices directly, higher Chinese steel exports would push the East Asian hot rolled coil price down and feed into Australian spreads on that same three to six month lag, and because BlueScope’s products are largely priced in United States dollars, a stronger Australian dollar lowers reported earnings whatever the steel price does. The second is cost inflation, where higher energy, metallurgical coal, iron ore and scrap prices, along with freight and labour rates, would compress the spread from the other side, and the margin expansion this thesis depends on is the gap between two moving numbers, only one of which is currently going the right way. The third is project execution, and it points straight at the cash flow inflection, because the North Star expansion, the Port Kembla reline and the United States painted steel strategy are all large capital projects running at once, and a cost overrun or a delay means capital expenditure stays elevated for longer. The capex cliff is the thesis, so anything that flattens it is the thing to watch. We would add a fourth of our own, which is that the shares have already run more than 30 per cent in a year and now sit above the effective value of a rejected takeover, so a good deal of the good news is in the price. If the earnings arrive later than forecast, there is not much of a valuation cushion underneath.

Our View

BlueScope is a cyclical business at a good point in its own capital cycle. The heavy spending is done this year, free cash flow steps up from almost nothing to more than a billion dollars, and a new framework hands most of it back through dividends and buybacks, while the United States mini mill captures a genuine spread widening now and the Australian business gets the same tailwind on a lag. We are not going to oversell it. The shares have already run more than 30 per cent in a year and now trade above what the rejected takeover was actually worth, and stripping the bid optionality out of the target leaves roughly 12 per cent of fundamental upside plus a 5 per cent yield, which is a high-teens total return rather than a doubling. The FY27 earnings peak depends on steel spreads nobody controls, and the forecasts sensibly assume those normalise rather than persist. But we are being paid a real yield out of real cash flow while the inflection lands, and we are buying a business with a superior product mix at a discount to the peers it is measured against. On that balance we think the risk and reward favours owners.

If you would like to discuss BlueScope Steel or how ASX-listed industrials and materials might fit within your portfolio, request a callback or call us on 1300 889 603. The above is general advice and does not consider your individual circumstances. Past performance is not a reliable indicator of future returns.